Introduction

Finance leaders are under pressure from every direction. Close cycles are getting shorter, compliance mandates are multiplying, and headcount budgets aren't growing to match. The tools that got finance teams here — RPA bots, rule-based automation, static dashboards — weren't built for this level of complexity.

According to Gartner, 59% of finance functions now use AI, with 57% already implementing or planning agentic AI specifically. For most finance organizations, agentic AI has already moved from roadmap to active budget line.

With adoption accelerating, the practical questions matter more than the hype. This guide covers what AI agents actually are in a finance context, which platforms are worth evaluating in 2025, where they deliver measurable ROI, and how to implement them without creating governance gaps that surface during audits.

Key Takeaways

- AI agents reason over data and execute multi-step workflows autonomously, making them fundamentally different from RPA bots

- Highest-ROI use cases: reconciliations, KYC/onboarding, fraud detection, invoice processing, credit assessment

- Implementation follows five stages: assess → govern → configure → pilot → scale (typically 8–16 weeks)

- Governance must be established before any agent touches production data — not after

- Indian enterprises and NBFCs need platforms built for GST, IRP e-invoicing, and MSME credit workflows that most global tools don't support

What Are AI Agents in Finance?

An AI agent is an autonomous software system that perceives inputs — documents, transaction data, system states — and reasons over them using large language models or similar AI. Unlike conventional automation, it executes multi-step actions across tools and systems with minimal human intervention.

RPA bots follow fixed scripts. Change the invoice format or the field name in your ERP, and the bot breaks. Standard chatbots respond to single queries but don't initiate actions, chain decisions, or operate across systems. AI agents do all three.

The Architecture Behind Finance-Grade Agents

A production-ready finance agent typically combines:

- LLMs for reasoning over unstructured inputs (PDFs, emails, policy documents)

- Retrieval-Augmented Generation (RAG) to pull from your company's own data — policies, ERP records, contracts — rather than relying on general training alone

- Tool-use for executing actions — writing journal entries, querying ERPs, triggering payment holds

- An orchestration layer that coordinates multiple agents working in parallel on complex workflows

The adoption data reflects how quickly this has moved from concept to deployment. Deloitte's 2025 survey found 80.5% of finance professionals believe agentic AI tools will become standard within five years — with trust, not capability, identified as the main adoption barrier. For finance teams evaluating deployment today, that means the priority question isn't whether agents can perform — it's whether your controls, audit trails, and approval workflows are ready to support them.

Top AI Agent Tools for Finance in 2025

There's no universal "best" platform. Tool selection depends on your ERP stack, regulatory context, and whether you have the engineering capacity to build custom workflows or need something pre-integrated.

Platforms for Oracle, SAP, and Workday-Centric Enterprises

The major ERP vendors have all embedded agents directly into their ecosystems:

- Oracle Fusion Cloud AI Agents — Purpose-built for Oracle's ERP/EPM stack, including a Payments Agent focused on cash outflow optimisation. Operates within Oracle's security boundaries and permission model

- SAP Joule Agents — Covers invoice clearance, goods receipt, purchasing, and finance workflows via the SAP AI Agent Hub. Joule Studio supports low-code and pro-code custom agent development

- Workday Illuminate — Financial Close Agent for close automation and real-time visibility, plus cost allocation, financial audit, payroll, and planning agents (some in early access as of late 2025)

The trade-off is consistent across all three: you get deep native integration and inherited security controls, but you're locked into a single-vendor ecosystem. Multi-ERP environments get complicated quickly.

Governance-First and Multi-Agent Frameworks

For firms that need more flexibility — or operate in heavily regulated environments:

- IBM watsonx Orchestrate — Pre-built connectors to 80+ enterprise applications, covering FP&A variance explanations, P2P invoice validation, O2C credit checks, and R2R close-cycle support. The watsonx.governance layer provides explainability and audit trail capabilities that regulated institutions need

- CrewAI — Open-source multi-agent orchestration framework suited for engineering teams building custom workflows. No finance-specific compliance certifications out of the box, but highly flexible for custom implementations

watsonx delivers governance infrastructure out of the box — at ERP-level cost and complexity. CrewAI gives you control over every workflow decision, but shifts the compliance and governance burden onto your internal engineering team.

AI Agents for India-Specific Finance Workflows

Most global platforms are built for US and EU finance stacks. They don't account for GST compliance monitoring, IRP-linked e-invoicing validation, MSME invoice financing workflows, or NBFC credit underwriting requirements.

Cygnet.One is built specifically for India's regulatory and financial infrastructure. The platform processes 15–19% of India's e-invoice volumes and covers the full stack of India-specific finance agent workflows:

- Cygnet BridgeCash — MSME invoice financing with AI-driven credit assessment ingesting GST returns, bank statements, ITR data, MCA data, and e-invoice data from Cygnet's own IRP platform

- Accounts Payable automation — Three-way matching across PO, GRN, and invoice with automated vendor compliance validation (PAN, GSTIN, MSME, bank account) via GSTN and MCA APIs

- GST reconciliation — ML-driven GSTR-2A/2B reconciliation with real-time IRP validation and auto-payment holds for non-compliant vendors

The platform has blocked ₹50 crore+ worth of risky payments across enterprise clients and reduced NBFC report processing time by 95%. With 250+ ERP integrations across SAP, Oracle, Microsoft Dynamics, and Tally, implementation timelines are shorter than building from scratch.

Evaluation Criteria to Apply Across Any Tool

Regardless of which category fits your environment — native ERP, open-source framework, or regional specialist — the same core criteria determine whether a tool is actually deployable. Assess each platform against:

- ERP integration depth — Native connectors vs. API-only vs. custom development required

- Compliance certifications — SOC 2 Type II, ISO 27001:2022, and region-specific accreditations

- Deployment model — Cloud-only vs. on-premises/VPC (non-negotiable for many banking and NBFC clients)

- Permission inheritance and RBAC — Agents should inherit user-level permissions, not operate with blanket system access

- Explainability and audit trails — Every agent decision needs a reviewable log, especially for credit and compliance workflows

- Total cost of ownership — Include implementation, integration, and ongoing governance overhead, not just licensing fees

Key Use Cases: Where AI Agents Transform Finance Operations

AI agents deliver the highest return when applied to high-volume, policy-bound workflows — where rules are clear but execution is manual, repetitive, and error-prone.

Reconciliations and Financial Close

This is where the ROI case is clearest. A 2025 MIT/Stanford study reported by CFO Dive found AI cut monthly financial close time by 7.5 days.

Agents handle:

- Matching subledger transactions and clearing intercompany balances

- Flagging exceptions with context rather than just surfacing discrepancies

- Generating journal entries and routing approval documentation

- Running reconciliations continuously rather than in a periodic cycle

The shift is from a 10+ day monthly close to a near-continuous close model. Finance teams stop burning the final week of every month on manual exception chasing.

KYC, Onboarding, and Compliance Monitoring

Financial institutions spent an estimated US$34.7 billion on financial crime compliance technology in 2024, according to Celent. Despite that spend, manual KYC processes still require revisits 49% of the time due to fragmentation and rework.

AI agents address this by automating:

- Identity verification and sanctions screening

- Document checks and case assembly

- Ongoing transaction monitoring against policy rules with explainable audit trails

Deloitte cites automation targets of 30–50% reduction in onboarding times for well-configured implementations.

Fraud Detection and Anomaly Identification

The ACFE's 2024 report found typical organisations lose 5% of annual revenue to fraud, with a median fraud duration of 12 months before detection. That's a full year of losses accumulating before a manual audit catches up.

AI agents operate in real time: monitoring transaction patterns in payables, receivables, and expense submissions, generating alerts with context, and flagging anomalies the moment they appear. McKinsey has identified agentic AI as applicable across KYC, AML, false-positive detection, and investigative workflows in financial crime contexts.

That pattern plays out in practice. Cygnet.One's Accounts Payable agents combine automated vendor GRC scoring, daily compliance status updates, and smart payment holds — blocking ₹50 crore+ in risky payments across enterprise clients.

Credit Assessment and Invoice Financing

For NBFCs and lenders serving MSMEs, turnaround time is a genuine competitive differentiator. SIDBI's 2024–25 Annual Report puts India's addressable MSME credit gap at approximately ₹30 lakh crore — a market that's largely inaccessible through manual underwriting processes.

AI agents compress credit decisions by ingesting multiple data sources in parallel:

- GST returns, ITR data, and bureau reports

- Bank statements with AI-driven pattern analysis

- E-invoice history from connected IRP platforms

Cygnet BridgeCash does exactly this, combining Cygnet.One's IRP platform data (covering 15–19% of India's e-invoice volumes) with consent-driven GST analytics to generate risk-optimised credit decisions for MSME borrowers.

FP&A and Reporting

Only 35% of FP&A professionals' time is spent on high-value analysis tasks, according to a 2024 FP&A Trends survey — the rest goes to data gathering, reconciliation, and spreadsheet consolidation.

AI agents handle the low-value portion: pulling data from multiple sources for rolling forecasts, running variance calculations, and generating narrative commentary on results. The practical result is fewer hours in spreadsheets and more time on decisions that actually require a finance professional's judgment.

How to Implement AI Agents in Finance: A Step-by-Step Guide

Rushing to deploy before governance is established is the most common cause of failed implementations. The process below covers five stages and typically spans 8–16 weeks for an initial production deployment.

The five stages at a glance:

- Assess readiness and define scope (Weeks 1–2)

- Establish governance before deployment (Weeks 2–4)

- Configure, integrate, and test (Weeks 4–8)

- Pilot with a defined user group (Weeks 8–14)

- Scale across workflows (Week 14+)

Step 1: Assess Readiness and Define Scope

Before selecting a tool, audit four areas:

- Data quality — Is your ERP data clean? Are GL codes consistent? Are documents indexed?

- Integration landscape — Which systems need to connect, and do APIs exist?

- Regulatory requirements — Jurisdiction-specific mandates (GST, ZATCA, GDPR) that agents must operate within

- Internal governance capacity — Who will own, review, and validate agent outputs?

The first workflow should be high-volume, rule-bound, and measurable. Expense approvals and invoice matching are good starts. Complex treasury forecasting or M&A due diligence are not.

Step 2: Establish Governance Before Deployment

No agent should touch production data until this framework exists:

- Assign a data steward, model owner, and risk officer with clear accountability

- Define RACI for every category of agent-triggered decision

- Configure RBAC so agents inherit user-level permissions — not system-level access

- Enable audit logging for all agent actions

- Set escalation rules that route low-confidence decisions to human review

Treating agents like system users — with unique credentials and least-privilege access — is becoming a consensus requirement among security teams in regulated industries.

Step 3: Configure, Integrate, and Test

Technical setup involves four core activities:

- Connect the agent to relevant data sources (ERP journals, bank feeds, document repositories)

- Validate integration with your system of record

- Run parallel processing for one full close cycle alongside the manual process

- Measure accuracy and exception rates before switching to autonomous execution

Platforms with pre-built ERP connectors compress this stage considerably — often by weeks. Cygnet.One supports 250+ ERP integrations across SAP, Oracle, Dynamics, and Tally, which means standard connectivity is rarely built from scratch.

Step 4: Pilot with a Defined User Group and Measure

Structure your pilot with clear boundaries:

- Limited user group — not the full finance team

- 60–90 day measurement window with a baseline captured before day one

- KPIs to track: cycle time reduction, exception auto-resolution rate, error rate, human override frequency

Capture the baseline before the pilot starts. Teams that skip this step often find themselves arguing over whether results improved at all — making ROI claims hard to defend and stakeholder support harder to hold.

Step 5: Scale Across Workflows

Once the pilot workflow achieves >80% autonomous execution with acceptable accuracy:

- Extend to adjacent workflows (procurement, treasury, tax)

- Expand user groups progressively

- Move from co-pilot mode (human reviews all outputs) to autonomous mode (human reviews exceptions only)

- Enable multi-agent coordination — procurement, treasury, and tax agents operating on a shared data context

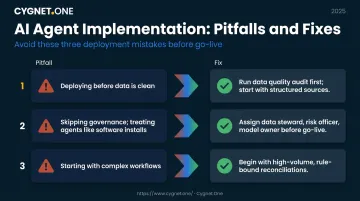

Common Implementation Pitfalls and How to Avoid Them

Deploying Agents Before Data Is Clean

Dirty ERP data, inconsistent GL coding, or missing document metadata produces high exception rates — and once users lose confidence in agent outputs, rebuilding that trust takes far longer than getting the data right upfront.

Run a data quality audit before integration. Start with the cleanest, most structured data source available (bank feeds rather than unstructured PDFs), then work outward. At ingestion, enforce:

- PII masking across all ingested records

- Consistent GL coding conventions before mapping to agent logic

- Standardized document metadata for invoices, contracts, and supporting files

Skipping Governance and Treating Agents Like Software Installs

When no one owns agent outputs or defines the escalation path, compliance gaps appear at the worst possible moment — during an audit, when regulators ask for decision rationale.

Governance roles — data steward, risk officer, model owner — must be assigned and a RACI signed off before any agent touches production data. Monthly model-drift reviews should be on the calendar before go-live, not after.

Starting With Too Complex a Workflow

Starting with high-variability, judgment-intensive workflows — like M&A due diligence or complex tax positions — before an agent is calibrated produces high override rates and, eventually, abandoned initiatives.

Start with high-volume, policy-bound workflows where rules are explicit and outcomes are measurable. Reconciliations are the right entry point. Forecasting comes after trust is established.

Each of these pitfalls shares a root cause: moving faster than the underlying readiness of data, governance, or process complexity allows. Sequence the rollout correctly and the agent compounds value; skip a step and you compound risk instead.

Frequently Asked Questions

What is the difference between an AI agent and an RPA bot in finance?

RPA bots follow fixed, rule-based scripts that break when inputs change — a new invoice format or renamed ERP field can stop a bot entirely. AI agents use LLMs to reason over unstructured data and handle variability, making them far better suited to document-heavy and judgment-adjacent finance workflows.

Which finance process should a company automate with AI agents first?

Start with reconciliations, expense approvals, or KYC/onboarding. These workflows are high-volume, rule-bound, and have a measurable before/after baseline — making it easier to demonstrate ROI and build internal confidence before expanding to more complex use cases.

How do AI agents maintain compliance with financial regulations?

Agents enforce compliance by monitoring transactions against policy rules and generating explainable audit trails for every decision. The strongest implementations inherit the organisation's existing RBAC and regulatory controls directly, avoiding a separate governance layer that compliance teams would otherwise need to reconcile.

How long does it take to implement AI agents in a finance team?

An initial single-workflow production deployment typically takes 8–16 weeks, depending on data readiness, ERP integration complexity, and governance setup — skipping governance or data quality stages is the most common reason pilots fail to scale.

Do AI agents for finance require on-premises deployment for sensitive data?

Enterprise-grade platforms offer on-premises or VPC deployment options that keep data within the organisation's security perimeter. For regulated industries like banking and NBFCs, this is often a non-negotiable requirement, not an optional add-on.

Are AI agents for finance suitable for Indian NBFCs and MSMEs?

Yes — Indian NBFCs and MSMEs handle high volumes of manual credit assessment, invoice processing, and GST compliance work, making AI automation especially impactful. Platforms built for India's regulatory stack (IRP-linked e-invoicing, NBFC underwriting workflows) deliver faster results than generic global tools. Cygnet.One's finance automation solutions, including BridgeCash for MSME invoice financing, are designed specifically for these requirements.