Introduction

Financial organizations today face a critical tension: customers expect real-time, seamless digital services comparable to what they experience with tech-native platforms, yet legacy infrastructure, regulatory pressure, and operational complexity pull in the opposite direction. Deloitte's 2024 Digital Banking Maturity study found that 'Digital Champions'—the top 10% of banks—are 2.5 times more likely to offer end-to-end remote product opening than their peers. Meanwhile, McKinsey reports the digital maturity gap between leaders and laggards has widened by 60% in just three years. The gap keeps growing.

Digital engineering—applying modern software, automation, AI, and architecture practices to build and operate financial systems—is how leading organizations are closing that gap. This means treating technology as a continuous, measurable capability, not a series of one-off IT projects.

The sections below cover what's driving urgency, the core pillars of digital engineering in finance, how compliance becomes a competitive advantage, and what real-world impact looks like.

TLDR:

- Financial services face a widening digital maturity gap—top performers are 2.5x ahead of peers

- Digital engineering treats cloud, AI, microservices, and automation as ongoing capability—not discrete projects

- Fintechs capture 5% of banking revenue and grow 2x faster than incumbents

- Engineered compliance transforms regulatory burden into operational advantage

- Measurable outcomes include 80% faster loan processing and 60% reduced invoice processing time

What Is Digital Engineering in Financial Services?

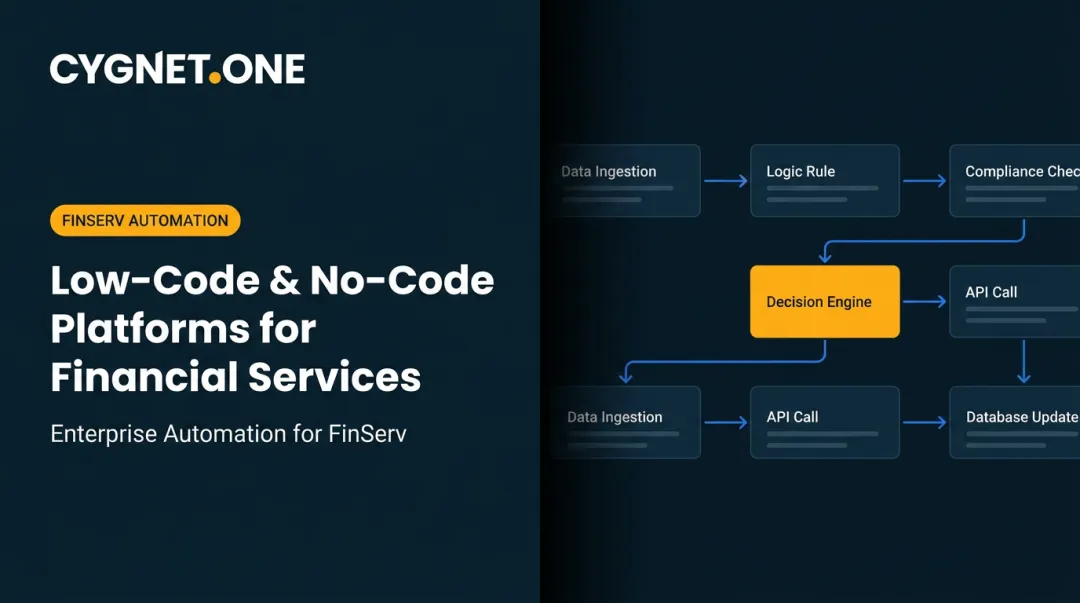

Digital engineering in financial services is the integrated practice of designing, building, modernizing, and operating financial systems using cloud infrastructure, microservices, AI/ML, workflow automation, and API-first architectures. It goes beyond one-off IT projects to treat technology as a continuous, outcomes-driven capability that evolves with business needs.

"Digital transformation" describes a destination—a changed organization that delivers value through technology. Digital engineering is the methodology that gets you there: the execution engine built on reliability, scalability, automation, and observability.

Without that engineering rigor, banks end up with expensive pilot projects that never scale.

Who Benefits Most

Digital engineering delivers the greatest impact for organizations where transaction volume, regulatory obligations, and customer experience are business-critical:

- Banks managing millions of transactions daily across multiple channels

- NBFCs competing on speed and customer experience without branch networks

- Insurance companies processing claims and underwriting decisions at scale

- Fintech platforms built on digital-native infrastructure but facing scaling challenges

- Microfinance institutions serving underbanked populations with thin margins

- Enterprise lending operations where loan processing speed impacts revenue

Across all of these, the pressure points are consistent: legacy systems that can't keep pace with demand, compliance requirements that grow more complex each year, rising customer expectations set by digital-native competitors, and the operational cost of maintaining both.

The Forces Pushing Financial Organizations Toward Digital Engineering

Competitive Pressure from Digital-Native Challengers

Fintechs and neobanks operate without legacy technical debt, deploying new products in weeks rather than quarters. BCG and McKinsey research indicates fintechs captured approximately 5% of the global banking revenue pool by 2024, with their revenue projected to grow at 15% annually—more than double the 6% rate of traditional banks.

In India, the UPI network processed 172 billion transactions in 2024, dominating retail payments. In the UK, Revolut has amassed around 10 million users. Digital-native players launch products in months while incumbents take years — a compounding gap that traditional institutions can't afford to ignore.

Regulatory Complexity Acceleration

Compliance requirements are multiplying globally — from e-invoicing mandates and GST/VAT obligations to real-time reporting frameworks. Manual or semi-automated compliance processes introduce risk, slow operations, and increase cost. Financial organizations that engineer compliance into their systems rather than bolting it on gain a structural advantage.

Key infrastructure in India illustrates the opportunity:

- TReDS and GSTN are reducing friction for SME financing and tax reporting

- SIDBI's 2023–24 report documents a ₹30 lakh crore MSME credit gap that digital compliance infrastructure is beginning to close

- Engineering compliance into systems — rather than managing it manually — cuts risk and accelerates operations

Internal Inefficiency Problem

Many financial organizations rely on fragmented legacy systems, manual workflows, and siloed data. The result: slow loan processing, error-prone reconciliation, and delayed reporting. McKinsey found banks' IT spending reached 10.6% of revenues in 2022, with 10–20% often diverted to resolving technical debt rather than building new capabilities.

That debt compounds over time. Legacy systems that once served their purpose now constrain every new initiative — raising integration costs, stretching time-to-market, and creating strategic exposure as digital-native competitors accelerate.

Key Pillars of Digital Engineering Driving Finance Transformation

Four foundational engineering capabilities, when applied together, produce lasting transformation in financial organizations. Each pillar addresses specific operational constraints while enabling broader strategic goals.

Artificial Intelligence and Process Automation

AI and ML are in active production at leading financial institutions, applied to high-value processes that were previously manual and error-prone:

- Automated credit scoring and risk assessment analyze far more data points than manual review, delivering faster, more consistent decisions

- Fraud detection through transaction pattern analysis identifies anomalies in real-time

- Intelligent document processing for loan origination extracts data from unstructured documents with high accuracy

- AI-powered reconciliation matches transactions across multiple systems, eliminating manual spreadsheet work

McKinsey and IACPM research from 2025 shows AI and automation can deliver 20-60% productivity gains for credit analysts and 30% faster decisioning speed. Leading firms achieve 80-90% straight-through processing, compared to under 50% for the average bank.

Automation doesn't replace human judgment. It augments it. AI systems surface decisions faster and with more consistency, freeing financial professionals for complex judgment calls and relationship management. The operational impact is measurable within months, not years.

Legacy Modernization and Cloud Migration

Those AI and automation gains depend on one prerequisite: infrastructure that can actually support them. Many banks and NBFCs still operate core processes on systems built for a different era. Monolithic architectures make scaling, updating, and integrating new capabilities slow and risky. Modernization to cloud-native, API-first, microservices architectures is what makes deploying AI, real-time analytics, and digital products at scale possible.

The practical approach is phased migration — wrapping or replacing legacy components without disrupting live operations. This lets organizations shift incrementally without "big bang" risk. BCG documents cases where big-bang core banking replacements took 3-6 years with cost overruns reaching 4x initial estimates.

Phased, cloud-native migrations deliver initial value in 6-12 months and reduce solution delivery times from 9-18 months to 3-4 months. The difference in risk and speed is significant.

The goal is not wholesale replacement. Strategically upgrade the components creating the most constraint, then build new capabilities on those modern foundations.

Real-Time Data and Analytics Infrastructure

In financial services, data latency is a risk. Slow or siloed data means credit decisions based on stale information, compliance reporting that lags reality, and customer experiences that feel disconnected. Digital engineering builds data pipelines and analytics infrastructure that surface real-time insights — from cash flow and ITC reconciliation to portfolio risk and customer behavior.

Modern data engineering gives finance teams dashboards and insights that were previously locked behind multi-day report cycles. This changes how financial organizations monitor risk and make decisions.

When compliance, risk, and operational data are visible in real-time, finance leaders can intervene proactively rather than reactively. That shift — from lagging indicators to live signals — is where real strategic value emerges.

Turning Compliance and Tax Complexity Into a Competitive Advantage

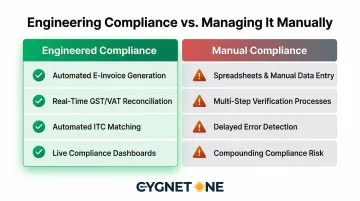

Most financial organizations treat regulatory compliance—e-invoicing, GST filing, VAT reporting, real-time payment reconciliation—as a cost center and a burden. Digital engineering inverts this. Organizations that engineer compliance deeply into their platforms gain speed, accuracy, and audit-readiness as operational by-products, not manual overhead.

What Engineered Compliance Looks Like

In practice, engineered compliance means:

- Automated e-invoice generation and validation integrated directly into ERP and accounting workflows

- Real-time GST/VAT reconciliation that eliminates end-of-period scrambles

- Automated ITC matching that preserves working capital by catching mismatches immediately

- Compliance dashboards that give finance teams instant visibility rather than requiring manual report compilation

Contrast this with the manual alternative: spreadsheets, multi-step verification, delayed error detection, and compliance risk that compounds over time. The error risk and processing cost differences are dramatic.

Production-Scale Compliance Infrastructure

Cygnet.One operationalizes this approach as a GSTN-approved IRP and GST Suvidha Provider, processing 15–19% of India's e-invoice volumes. With recognition from HMRC (UK), FTA (UAE), ZATCA (Saudi Arabia), and BOSA (Belgium), Cygnet.One has built tax and finance compliance into enterprise-grade infrastructure.

The platform has generated 412 million+ e-invoices and processes 55 million+ transactions monthly. Those numbers reflect engineering discipline, not just software.

Compliance at this volume demands automated validation, real-time error handling, audit trails, and integration with 250+ ERP systems without disrupting operations. That reliability is what allows compliance to become infrastructure rather than overhead.

The Downstream Financial Services Impact

Reliable compliance infrastructure gives financial organizations a direct path to invoice financing and working capital solutions. Verified invoice data flows into credit assessment automatically, reducing loan processing turnaround time by up to 80% while improving risk accuracy.

In India, digital infrastructure like TReDS has reduced MSME invoice-to-cash cycles from 90-120 days to under 48 hours, addressing the estimated ₹30 lakh crore MSME credit gap documented by SIDBI. The Cygnet.One and Ratnaafin partnership for MSME Invoice Financing demonstrates this model: compliance workflow data feeds directly into faster, more accurate lending decisions.

Measuring the Real Business Impact of Digital Engineering

Financial organizations considering digital engineering investments need to understand what changes in their operations. Outcomes matter more than technology features. The table below shows what digital engineering delivers across four critical process areas:

| Process Area | Outcome | How It Works |

|---|---|---|

| Loan Processing Speed | 80% reduction in TAT — days to hours | AI-powered credit decisioning and document processing |

| Invoice Reconciliation | 60% faster processing; errors near-eliminated | RPA and AI OCR integrated with ERP via three-way matching |

| Report Cycle Time | 95%+ reduction — multi-day cycles cut to minutes | Real-time data pipelines and automated reporting |

| Compliance Error Rates | 90% faster process cycles; reduced audit risk | Automated validation catches errors at the point of transaction |

Rapid, Quantifiable Results

Unlike traditional IT programs, digital engineering produces measurable results within months, not years. Targeted improvements — automated invoice processing, AI-powered credit scoring, real-time reconciliation — deliver quantifiable outcomes quickly. Each win builds the internal confidence and data infrastructure needed for broader transformation.

The Risk-vs-Reward Calculation

Digital engineering initiatives require upfront investment in platform, integration, and change management. The ROI case is clear: organizations that delay modernization accumulate technical debt, face rising compliance risk, and cede ground to more agile competitors. Every quarter of delay raises integration costs and widens the capability gap.

Organizations that invest now can deploy new financial products faster as market conditions shift — a measurable advantage in a sector where speed to market directly affects lending volumes and customer retention.

Partner Ecosystem and Integration Depth

The 250+ successful ERP integrations Cygnet.One has completed demonstrate that digital engineering for finance must connect deeply with existing enterprise systems, not operate in isolation. The value of a platform is partly measured by how quickly it can be embedded into existing workflows without disrupting operations. Integration timelines of weeks rather than months determine whether transformation delivers value or creates new bottlenecks.

Frequently Asked Questions

Which engineering is best for banking?

No single engineering discipline covers it all. Banking requires software engineering for core systems, data engineering for real-time analytics and risk modeling, and automation engineering for compliance workflows. The best results come from integrating these under a digital engineering framework tied to specific business outcomes.

What are the 7 digital banking trends?

The key digital banking trends shaping financial services today include: AI-driven credit decisioning, real-time payments infrastructure, open banking and API ecosystems, cloud-native core banking migration, hyperautomation for back-office operations, embedded finance and Banking-as-a-Service (BaaS), and advanced regulatory technology (RegTech) for compliance. Together, these trends reflect a shift from product-centric to data-driven, experience-first banking models.