The collision of these forces creates operational bottlenecks that directly impact profitability and risk exposure. The average cost to originate a mortgage has more than doubled from $5,100 in 2012 to $11,600 in 2023, representing an 8% annual increase driven largely by inefficient processes. Meanwhile, nearly 70% of IT budgets in banking are consumed by maintaining legacy systems, leaving minimal resources for innovation.

Low-code process automation offers a practical answer to these challenges. Rather than waiting months for custom development cycles, finance teams can build, test, and deploy automated workflows in days or weeks using visual designers and pre-built connectors. This article explains how low-code automation works in BFSI contexts, where it delivers the highest ROI, and what capabilities distinguish enterprise-grade platforms from consumer tools.

Key Takeaways

- Low-code platforms cut deployment time from months to weeks through visual workflow builders and pre-built integrations

- They address core BFSI pain points including loan processing delays, manual compliance checks, invoice errors, and fragmented legacy data

- High-impact use cases include credit assessment, e-invoicing compliance, regulatory reporting, customer onboarding, and MSME invoice financing

- Enterprise-grade platforms must cover multi-jurisdictional compliance, deep ERP integration, full audit trails, and 99.9%+ uptime SLAs

The Hidden Cost of Manual Processes in Financial Services

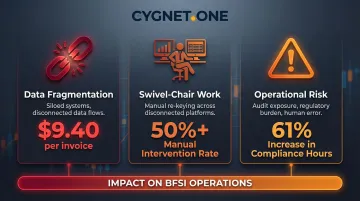

Manual workflows impose severe operational penalties across BFSI operations. Banks routinely experience Straight-Through Processing (STP) rates below 50% for core operations, meaning more than half of all transactions require manual intervention. The financial impact is measurable: organizations spend an average of $9.40 to process a single invoice manually, with exception rates averaging 14% and climbing to 22% for poor performers.

The compliance burden compounds these inefficiencies. Between 2016 and 2023, employee hours dedicated to compliance increased by 61%, with 42% of C-Suite time and 43% of board time now devoted to regulatory matters. When a compliance deadline is missed—whether for suspicious activity reporting, regulatory filing, or data retention—the consequences cascade. A single missed step in anti-money laundering (AML) processes can trigger multi-million dollar penalties, as demonstrated by HSBC's £64 million fine from the UK's FCA for AML failings and TD Bank's $3 billion US Department of Justice settlement for money laundering facilitation.

Underlying all of this is a legacy system fragmentation problem. Financial data lives in silos across core banking platforms, ERPs, CRMs, and specialized systems — and nearly half of financial organizations report this fragmented data creates what Deloitte describes as "the need for massive reconciliation."

The result is widespread "swivel-chair" work, where employees manually re-key data between disconnected systems. This directly drives:

- Higher reconciliation workload and error rates

- Elevated operational risk from manual handoffs

- Near-zero end-to-end process visibility

Without a way to connect these systems, financial teams spend more time moving data than acting on it — which is precisely where low-code automation creates the most immediate impact.

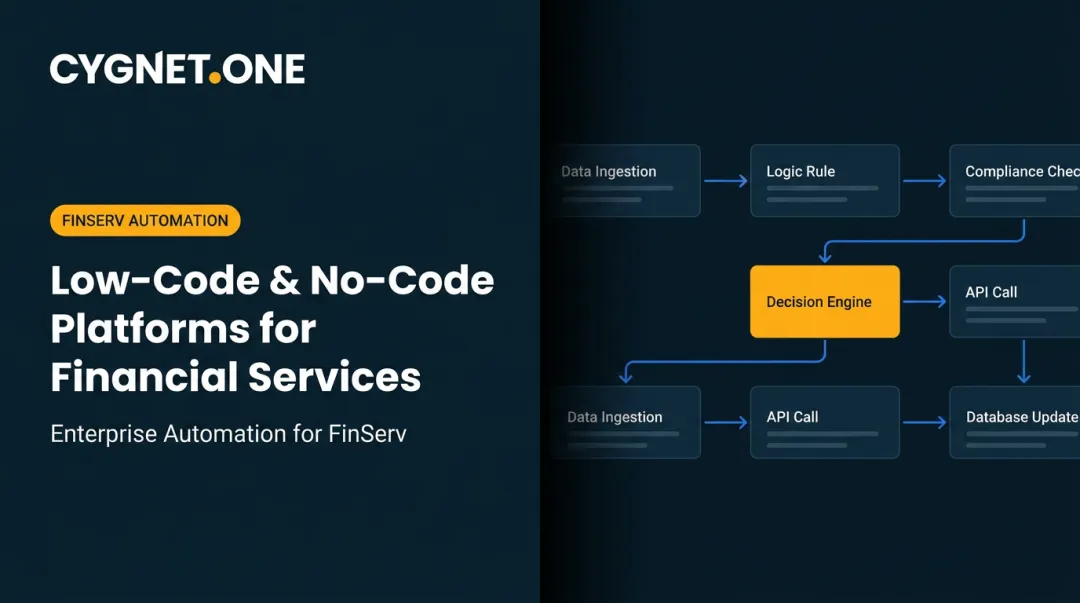

What Low-Code Process Automation Really Means for Financial Institutions

Low-code process automation is a development approach that uses visual workflow designers, drag-and-drop logic builders, and pre-built connectors to create, test, and deploy process applications. Rather than writing thousands of lines of custom code, business analysts and IT teams configure workflows through graphical interfaces that define how data moves between systems, when approvals are required, and what validations must be enforced.

The platform generates the underlying application code automatically, handling integration logic, data transformations, and user interface elements. This approach reduces the technical barrier to building sophisticated workflows while maintaining the flexibility to add custom code when business logic demands it.

Differentiating Low-Code from Traditional Automation

Low-code platforms differ fundamentally from both Robotic Process Automation (RPA) and traditional custom development. RPA mimics human actions at the user interface level—clicking buttons, copying data between screens, filling forms—making it effective for automating repetitive tasks within existing applications. However, RPA scripts are brittle; when the underlying application changes, the bot breaks.

Low-code builds the orchestration layer that coordinates systems and people across end-to-end processes. Instead of mimicking clicks, low-code platforms connect directly to system APIs, databases, and services. This architecture makes low-code solutions more maintainable, change-ready, and suitable for complex workflows where business rules evolve constantly—a critical advantage in financial services where regulations and products change frequently.

Traditional custom development offers maximum flexibility but requires months of requirements gathering, coding, testing, and deployment. A Forrester study analyzing platform-based application modernization found organizations achieved a 50% increase in application development speed and 228% ROI over three years by adopting low-code approaches instead of building everything from scratch.

What "Enterprise-Grade" Means in a Finance Context

An enterprise low-code platform is a development environment built for large-scale, mission-critical applications — one that goes well beyond what consumer or SMB tools can handle. For financial institutions, that distinction comes down to a specific set of capabilities:

- Access controls: Fine-grained role-based permissions with segregation of duties across dev, test, and production environments

- Data security: Encryption at rest and in transit, with SOC 1 and SOC 2 compliance maintained

- Audit readiness: Immutable audit trails, version-controlled workflow changes, and regulatory examination reports on demand

- Scale: High-volume transaction processing with comprehensive ERP integrations built in

These capabilities also clarify why low-code and no-code are not interchangeable in BFSI contexts. No-code platforms handle simpler use cases — form builders, basic approval workflows — well enough. Low-code, by contrast, handles sophisticated business rules, multi-system integrations, and compliance requirements that no-code tools cannot support.

Financial services processes like loan origination, credit assessment, regulatory reporting, and cross-border compliance all require conditional logic, API integrations, and exception handling. That's the domain where low-code delivers its clearest value.

Key Financial Processes That Low-Code Automation Transforms

Loan Origination and Credit Assessment

Low-code platforms orchestrate the entire loan lifecycle from application intake through funding. A single automated workflow handles:

- Document collection and identity verification through KYC providers

- Credit scoring API calls and multi-source data aggregation

- Risk-threshold routing through approval hierarchies based on lending policies

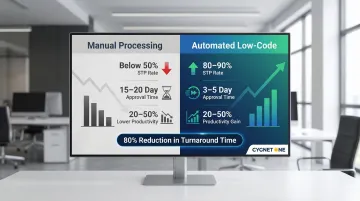

This orchestration compresses turnaround times. Top-tier banks leveraging automation achieve STP rates of 80-90% for loan operations, compared to below 50% for institutions relying on manual processes—delivering productivity gains of 20-50%. A Benelux bank reduced mortgage approval time from 15-20 days to just 3-5 days by digitizing its processes.

Cygnet.One's implementations demonstrate similar impact. One major Indian private bank achieved 80% reduction in loan processing turnaround time through automated workflows that handle document collection, credit decisioning, and disbursement. The platform's credit assessment engine builds 360-degree risk profiles within 10 minutes using GST data, bank statements, financial statements, and invoices, enabling risk-optimized decisions without manual underwriting for standard applications.

Invoice Processing and E-Invoicing Compliance

Invoice automation addresses one of the highest-volume, most error-prone processes in financial operations. Low-code platforms automatically capture invoice data through OCR or direct integration, validate line items against purchase orders and contracts, check tax calculations against jurisdiction-specific rules, and route exceptions for review.

For e-invoicing compliance, platforms with built-in government connectors eliminate manual validation entirely. The end-to-end process runs automatically:

- Generate invoices in the required schema (XML, JSON, PDF/A-3)

- Submit to the tax authority portal for validation

- Receive the cryptographic stamp or unique identifier

- Archive the compliant document for audit readiness

Best-in-class organizations reduce invoice processing costs from $9.40 to under $3.00 per invoice through automation. Cygnet.One's platform, recognized by GSTN, HMRC, FTA, ZATCA, and BOSA, processes 55 million transactions monthly and has generated over 412 million e-invoices, demonstrating production-scale capability. One implementation reduced invoice processing time by 60% through automated validation, real-time GST sync, and integration with SAP, Oracle, and other ERP systems.

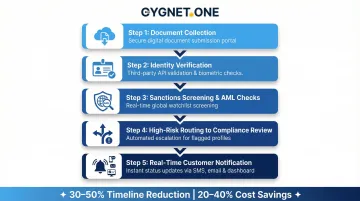

Customer Onboarding and KYC Workflows

Financial institutions use low-code to build dynamic onboarding journeys that adapt based on customer type, product selection, and risk profile. Each workflow step runs automatically:

- Collect documents via web or mobile interfaces

- Trigger background checks and identity verification through third-party services

- Perform sanctions screening and AML checks

- Route high-risk applications for compliance review

- Notify customers of status changes in real time

The average corporate client onboarding process takes 100 days, with KYC and account opening consuming over 40% of that time. Large institutions spend up to $30 million annually on KYC programs. Low-code platforms can compress these timelines by 30-50% and reduce costs by 20-40% through centralized, automated workflows that maintain full audit trails for regulatory examination.

Regulatory Reporting and Reconciliation

Low-code platforms pull data from core banking, ERP, treasury management, and trading platforms, then apply transformation rules to produce regulatory report formats. The system performs validation checks, generates submission files, and flags exceptions for manual review—with no manual extraction required.

One of India's leading NBFCs reduced report processing time by over 95% using Cygnet.One's platform to automate data collection, validation, and report generation. The solution eliminated manual data extraction and reconciliation, reducing a multi-day process to hours while improving accuracy and providing real-time compliance dashboards for CFO visibility.

MSME Invoice Financing and Supply Chain Finance

The MSME credit gap remains severe across emerging markets—in Kenya alone, MSME demand for supply chain finance is 1.2 trillion KES while supply meets only 7-10% of demand. Low-code platforms make embedded finance viable at scale by removing the manual bottlenecks that make small-ticket lending uneconomical.

Anchor companies and lenders can offer embedded finance to smaller suppliers without manual intervention. Automated workflows handle the full cycle:

- Capture invoices through e-invoicing integrations

- Assess supplier creditworthiness using invoice history, payment patterns, and GST filings

- Calculate discount rates based on risk and tenor

- Route approvals through credit committees and trigger disbursement

Cygnet.One's BridgeCash platform, launched in partnership with Ratnaafin, automates the entire invoice financing lifecycle from sourcing through disbursement, reducing the cost and complexity of serving high-volume, lower-value MSME transactions at scale.

How Low-Code Handles Compliance in Multi-Regulatory Environments

Financial institutions operating across jurisdictions face divergent e-invoicing mandates, tax reporting formats, and data residency rules. Each market runs its own technical stack — and compliance failures in any one of them carry real regulatory consequences.

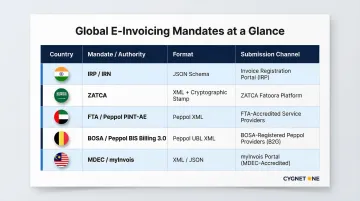

Key mandates by jurisdiction include:

- India: Real-time invoice clearance through the IRP using JSON-based schemas and IRN generation

- Saudi Arabia: XML invoices with cryptographic stamping (ZATCA) before transmission to buyers

- UAE: Peppol-based PINT-AE specifications routed through FTA-accredited service providers

- Belgium: Peppol BIS Billing 3.0 enforced for B2G transactions (BOSA-registered platforms)

- Malaysia: Submission to the myInvois portal for validation via MDEC-accredited providers

Low-code platforms with pre-built compliance connectors and government-recognized integrations eliminate the need to rebuild validation logic from scratch for each market. The platform maintains libraries of jurisdiction-specific schemas, validation rules, and submission protocols. When an invoice is generated, the system automatically applies the correct template, performs validations, and submits through the appropriate channel based on the destination country.

Built-In Audit Trail and Access Control

A BFSI-grade low-code platform must enforce role-based permissions that separate duties across workflow design, testing, approval, and execution. Every process step—who initiated it, when it occurred, what data changed, what decision was made—must be logged with immutable timestamps and stored for the retention period required by regulators.

These audit logs must be exportable in formats suitable for regulatory examination (CSV, XML, JSON) and searchable by date range, user, transaction ID, or process instance. During regulatory examinations, examiners pull complete process histories to verify that controls are operating as designed — gaps in that record create audit exposure that is difficult to remediate after the fact.

Data Security Expectations

The average data breach in financial services costs $5.56 million, the highest of any industry. Enterprise low-code platforms must encrypt data at rest using AES-256 or equivalent standards and in transit using TLS 1.2 or higher. Infrastructure must be SOC 1 and SOC 2 compliant, covering security, availability, processing integrity, confidentiality, and privacy.

The platform must also support data residency configurations that keep customer data within specific geographic boundaries — a requirement under GDPR, India's data localization rules, and regional banking regulations.

Multi-tenant architectures must provide logical data separation to prevent cross-customer data leakage.

Change Management Under Compliance

When regulations update—a new e-invoice schema version, a GST rate change, revised KYC requirements—low-code allows compliance teams to modify workflow rules and validation logic without waiting for a developer release cycle. The compliance officer updates the validation rule in the visual designer, tests the change in a sandbox environment, and promotes it to production through a governed change management process.

In custom-built systems, even minor rule changes require developer tickets, code modifications, testing cycles, and deployment windows — a process that can take weeks. Low-code compresses that to hours, reducing both compliance risk and the operational cost of staying current.

Choosing a Low-Code Platform Built for Financial Services

BFSI-Specific Workflow Templates and Connectors

Generic low-code platforms require extensive customization to support financial services use cases. Enterprise buyers should prioritize platforms that arrive ready for BFSI workflows — not ones that treat them as an afterthought.

Key capabilities to evaluate:

- Pre-built templates for loan origination, KYC onboarding, invoice financing, and regulatory reporting

- Native connectors to ERPs (SAP, Oracle, Microsoft Dynamics, Tally) and core banking systems (Finacle, Temenos)

- Out-of-the-box integration with payment gateways and government portals

- Compliance accreditations across target operating geographies

Platforms with 250+ pre-built ERP integrations and government-recognized compliance accreditations across multiple countries provide immediate value. Cygnet.One demonstrates this with accreditations from GSTN (India), ZATCA (Saudi Arabia), FTA (UAE), HMRC (UK), BOSA (Belgium), and MDEC (Malaysia), enabling compliant e-invoicing and tax reporting without custom development.

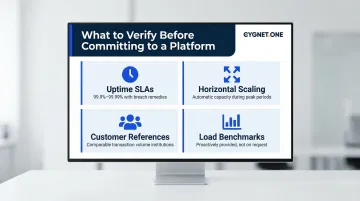

Scalability and Uptime Requirements

Financial transaction volumes are non-negotiable. The platform must handle peak processing periods — month-end close, tax filing deadlines, loan origination surges — without performance degradation. Multi-tenant architectures must demonstrate logical data separation that prevents one customer's workload from impacting others.

When evaluating vendors, check for:

- Uptime SLAs of 99.9%–99.99% for production, with defined breach remedies

- Horizontal scaling that adds capacity during peak periods without manual intervention

- Customer references from institutions with comparable transaction volumes

- Load performance benchmarks provided proactively, not just on request

Implementation and Change Velocity

The operational value of low-code depends on how quickly teams can configure new workflows and modify existing ones. Before committing, confirm that business analysts can make process changes without raising IT tickets, that sandbox environments exist for pre-production testing, and that adding a new validation rule doesn't require a developer sprint.

Platforms that require developer involvement for routine changes defeat the purpose of low-code. The best implementations empower compliance and operations teams to make rule changes, add approval steps, or modify notifications independently, while IT maintains governance over infrastructure, security, and integration architecture. In practice, that means a compliance officer can update a KYC rule on a Friday afternoon — without filing a ticket or waiting for a release cycle.

Frequently Asked Questions

What is an enterprise low-code platform?

An enterprise low-code platform is a development environment built for large-scale, mission-critical applications — supporting high-volume transactions, ERP integrations, immutable audit trails, and regulatory compliance. Unlike consumer tools, these platforms enforce role-based access, SOC 1/2 compliance, and the governance frameworks regulated industries require.

What is low-code no-code financial services?

Low-code/no-code in financial services refers to using visual development platforms to build and automate banking, lending, insurance, and compliance workflows. Low-code suits complex, regulated processes requiring sophisticated business rules and multi-system integrations, while no-code targets simpler internal tools like forms and basic approvals.

How does low-code automation help with regulatory compliance in financial services?

Low-code platforms with built-in compliance connectors automate validation against regulatory schemas (GST, VAT, e-invoicing mandates) and enforce immutable audit trails at every process step. When regulations change, compliance teams can update workflow rules directly, without waiting on full redevelopment cycles.

What financial processes are best suited for low-code automation?

The highest-ROI starting points are processes with high transaction volumes, multi-system dependencies, and frequent regulatory changes:

- Loan origination and credit assessment

- Invoice processing and e-invoicing compliance

- Customer onboarding and KYC workflows

- Regulatory reporting and reconciliation

- Supply chain finance

How long does it take to implement low-code automation for a financial institution?

Simple workflows or proofs-of-concept typically go live in 2-3 months. Medium-complexity applications with ERP integration deliver measurable results within 4-9 months. Enterprise-wide programs with deep core banking integration generally require 9-24 months for full deployment.

Can low-code platforms integrate with existing banking and ERP systems?

Yes. Enterprise low-code platforms connect to existing systems via APIs, pre-built connectors, and middleware. Platforms with 250+ pre-built ERP connectors can link core banking systems (Finacle, Temenos), ERPs (SAP, Oracle, Microsoft Dynamics), and government portals without custom development work.