Introduction

Financial institutions process millions of transactions daily — payroll runs, account reconciliations, e-invoice submissions, regulatory filings — and without structured automation, errors and compliance gaps compound at scale. Batch process automation is the automated execution of high-volume, repetitive financial tasks in grouped runs at scheduled intervals, without manual intervention.

For finance leaders, IT heads, and operations teams at banks, NBFCs, and insurance companies, this is the operational backbone that keeps back-office functions running accurately, auditably, and on schedule.

This guide covers what batch automation means in practice for financial services, the core use cases driving adoption, how to evaluate implementation approaches, and what to look for when choosing a platform.

Key Takeaways

- Batch process automation processes high-volume financial tasks on a schedule, without human intervention

- Most back-office functions—payroll, interest calculation, EOD settlement—operate on defined cycles, not on-demand

- Automation eliminates manual data entry, cuts errors, and handles volume spikes without adding headcount

- Unlike real-time processing, batch automation prioritizes efficiency and cost-effectiveness over speed

What Is Batch Process Automation in Financial Services?

Batch process automation groups financial transactions and documents — invoices, loan disbursements, tax filings, account statements — and processes them in bulk on a defined schedule. Those schedules run at set intervals: end-of-day, weekly, or month-end, with no manual trigger required for each task.

What the process achieves:

- Applies uniform rules and validation logic across every transaction in the batch

- Generates a complete audit trail for every action taken on every record

- Processes thousands to millions of transactions within a single structured run

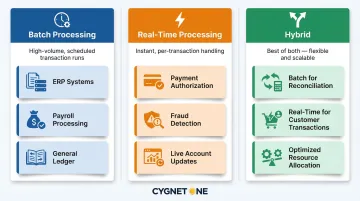

Batch vs. Real-Time Processing

Batch processing collects data over a defined window and runs it together. Real-time processing handles each transaction the instant it arrives. Most core financial systems — ERP, core banking, general ledger — are built around batch cycles, not continuous processing.

Batch processing is not simply "running a report at night." A full batch workflow spans data ingestion, validation, transformation, compliance checks, posting, and output generation — each step automated in sequence.

Key differences at a glance:

- Batch: High-volume, scheduled runs; suited for ERP, payroll, and general ledger cycles

- Real-time: Instant per-transaction handling; suited for payment authorization and fraud detection

- Hybrid: Many enterprises combine both — batch for reconciliation, real-time for customer-facing transactions

Why Financial Institutions Rely on Batch Processing

Financial institutions manage recurring, high-volume workflows that no manual team can handle at scale. India's NEFT system processed 9.27 billion transactions in 2024, while the UK's Bacs system handled 6.86 billion payments in 2025. At those volumes, manual processing isn't just inefficient — it's unworkable.

What Financial Services Uniquely Demands

Batch automation addresses:

- Regulatory compliance cycles: GST filing, VAT returns, e-invoice generation mandates

- Month-end close accuracy: Multi-system reconciliation and financial statement preparation

- Interest computation: Scheduled calculation and posting across thousands of accounts

- Multi-level approval workflows: Consistent, documented sequences every time

The Cost of Manual Processes

Without batch automation, financial institutions face:

- Data entry errors and reconciliation mismatches

- Duplicate payments and processing delays

- Late regulatory submissions carrying financial penalties

- Audit trail gaps creating compliance risk

Gartner research shows poor data quality costs organizations an average of $12.9 million annually, while a Forrester study documented an 86% reduction in trade capture errors through automation.

Regulatory and Operational Drivers

Those error and cost figures only grow when regulatory deadlines enter the picture. In jurisdictions such as India's GST framework, UAE VAT, UK HMRC mandates, and Saudi Arabia's ZATCA, financial reporting and invoicing must follow structured, documented processes by law. Batch automation builds that audit trail into every run — meeting compliance requirements without separate manual effort.

Real-world scale: Cygnet.One, which processes 15–19% of India's e-invoice volumes through its platform, has documented a 95%+ reduction in report processing time and 60% faster invoice processing cycles for organizations with ERP-integrated batch workflows.

How Batch Process Automation Works: End-to-End

Batch automation pulls financial data from ERP systems, banking platforms, vendor portals, and regulatory gateways into a processing queue. At the scheduled trigger, the system runs the entire batch through validation, transformation, compliance checks, and system posting — with no manual intervention required.

Scheduling rules, exception handling logic, and integration connectors govern the process. Outputs include updated accounting records, filed reports, payment instructions, and compliance submissions.

Step 1: Data Ingestion and Batch Formation

Data arrives from multiple channels:

- ERP modules and core banking systems

- Vendor invoice portals

- Tax gateways and regulatory platforms

- Payment networks and clearing houses

The batch formation step defines which records belong to the current cycle based on date range, document type, or transaction category. This prevents incomplete or duplicate data from entering the pipeline.

Step 2: Automated Validation, Processing, and Compliance Checks

Once assembled, the automation engine validates each record against predefined rules:

- Matching invoices to purchase orders

- Checking tax computation accuracy

- Flagging duplicate transactions

- Verifying vendor or counterparty data

The engine then applies compliance checks — including e-invoice schema validation against regulatory gateways and VAT calculation verification. Exceptions route automatically for human review; clean records continue through the pipeline without interruption.

Step 3: System Posting, Output Generation, and Audit Logging

The final stage handles three distinct outputs simultaneously:

- ERP posting: Validated records update directly in the accounting or ERP system

- Regulatory submissions: Reports transmit automatically to authorities such as GSTN, HMRC, or ZATCA

- Audit logging: Every action on every record is written to a tamper-proof log in real time

This audit trail supports financial audits and regulatory inspections without any additional manual documentation.

Where Batch Processing Is Applied in Financial Services

Batch automation is the standard operating model for:

Core Banking Operations:

- End-of-day transaction settlement and reconciliation

- Interest calculation and posting

- Account statement generation

Payment Processing:

- Payroll disbursement

- Bulk payment file generation

- NEFT, RTGS, and clearing network transaction processing

Tax and Regulatory Compliance:

- E-invoice generation and submission to tax authorities

- GST/VAT return preparation and filing

- Regulatory report generation and transmission

Lending Operations:

- Loan disbursement processing

- EMI and interest computation in NBFCs

- Credit assessment and approval workflows

Insurance:

- Claims batch adjudication

- Premium calculation and billing

- Regulatory filing preparation

Each of these domains shares a common scheduling logic: batch jobs run when transactional systems are quiet.

When Batch Jobs Run

Batch processes typically execute at off-peak hours — overnight, weekend, or month-end — to avoid competing with real-time transactional systems.

They're triggered on:

- Fixed schedules: Daily EOD, weekly payroll, monthly close

- Volume thresholds: Once an invoice queue crosses a defined threshold (e.g., 500+ records)

- Regulatory deadlines: Mandatory tax filing dates

The process is recurring and often regulatory-deadline-driven. For institutions operating under e-invoicing mandates or periodic tax filing requirements (monthly GST, quarterly VAT), batch automation is the mechanism that ensures compliance at scale.

India's GSTN processes over 11 million e-invoices on peak days — a scale that manual workflows simply cannot absorb without automation.

Common Challenges, Misconceptions, and When to Reconsider

Operational Challenges

Batch Window Overruns:

Legacy ERP systems with rigid batch windows create delays when urgent transactions arrive after a cycle closes. The Bank for International Settlements notes this puts immense pressure on traditional EOD processes as institutions try to support 24/7 services.

Mid-Batch Failures:

Poorly configured validation logic allows data errors to propagate through entire batches before being caught. When batch jobs fail midway, incomplete postings create reconciliation problems requiring significant manual effort to unwind.

Data Quality Issues:

"Poisoned data" (erroneous, incomplete, or poorly formatted records) entering the system can corrupt downstream processes and reports. The adoption of richer data formats like ISO 20022 increases this risk if validation controls aren't robust.

Key Misconceptions

Misconception 1: Batch automation requires replacing existing ERP systems

In practice, automation layers can integrate with legacy infrastructure through APIs or middleware without full platform replacement. This means institutions can modernize incrementally rather than committing to a costly rip-and-replace project.

Misconception 2: Automation eliminates the need for exceptions management

Well-designed batch systems reduce exceptions but don't eliminate them. Exception handling remains a critical component. Systems must:

- Route flagged transactions to the appropriate review queue

- Enable operator corrections without disrupting the broader batch

- Maintain audit trails of all manual interventions

When Batch Processing Isn't the Right Fit

Batch cycles introduce unacceptable latency for transactions requiring immediate action:

- Real-time fraud alerts

- Instant payment schemes

- Emergency fund transfers

- Customer-facing payment confirmations

Organizations should map which workflows operate on cycles (payroll, reporting, tax filing) versus which require real-time responses. Where there's a mismatch, applying batch architecture simply because it's the legacy default creates risk — not efficiency.

Conclusion

Batch process automation delivers a structured, auditable, scalable method for handling high-volume recurring financial workflows—from e-invoice generation to regulatory reporting—with reduced errors, lower manual effort, and traceable compliance records.

The value lies not in replacing judgment but in eliminating the repetitive, error-prone manual steps that delay decisions and expose organizations to compliance risk. Organizations that design automation around actual cycle requirements—rather than defaulting to batch or real-time without evaluation—see faster reconciliation cycles, cleaner audit trails, and fewer last-minute reporting failures.

Key outcomes batch automation delivers in financial services:

- Predictable processing windows that align with regulatory deadlines

- Audit-ready records with full transaction traceability

- Reduced manual intervention in high-volume, recurring workflows

- Consistent output quality regardless of transaction scale

As regulatory mandates expand and transaction volumes grow, batch automation gives financial institutions the operational backbone to scale without sacrificing accuracy or compliance readiness—two things no audit or regulator will overlook.

Frequently Asked Questions

What is batch processing in finance?

Batch processing is the automated grouping and execution of financial tasks—such as payroll, invoice processing, and reconciliation—in scheduled runs rather than one transaction at a time. This enables high-volume throughput with minimal manual intervention.

Why do banks do batch processing?

Banks rely on batch processing because core banking functions—EOD settlement, interest calculation, statement generation—operate on defined cycles, not continuously. Batch automation handles the volume, enforces data consistency, and meets the processing SLAs required by regulators.

Is batch processing still used today?

Yes. Batch processing remains widely used in financial services because back-office functions like regulatory reporting, GST and TDS filing, and GL posting operate on scheduled cycles, not in real-time. It's the most cost-effective and reliable approach for recurring, high-volume workflows.

What is the difference between batch processing and real-time processing in financial services?

Batch processing groups transactions and executes them at scheduled intervals—optimized for cost and throughput. Real-time processing handles each transaction instantly. Most financial institutions use both, depending on whether the workflow is back-office or customer-facing.

What are common examples of batch processing in banking?

Common examples include end-of-day account reconciliation, payroll disbursement, EMI and interest calculation, e-invoice generation and tax authority submission, regulatory report generation (GST returns, VAT filings), and bulk statement generation for account holders.

How does batch process automation reduce errors in financial operations?

Automation applies consistent validation rules across every transaction in the batch, checking for duplicates, mismatches, and compliance errors before posting. This removes the manual data entry step where most errors originate. Every run also generates a full audit log, making discrepancies straightforward to trace and correct.