Low-code development offers banks and NBFCs a practical way to break through this barrier — faster, with less risk, and without ripping out systems that still work. This guide explains how low-code platforms are helping financial institutions modernize incrementally, the highest-value use cases delivering measurable ROI, and a practical framework for starting your transformation journey.

TLDR: Key Takeaways

- Low-code platforms accelerate application delivery by 50–70%, enabling banks to deploy new capabilities in weeks instead of months

- Highest-ROI use cases: digital onboarding, loan origination automation, compliance reporting, and fraud monitoring dashboards

- Low-code connects to legacy cores via APIs — no core system disruption required

- Start with one high-impact use case, prove ROI in 60–90 days, then scale with governance built in from the start

Why Traditional Banking IT Is Struggling to Keep Up

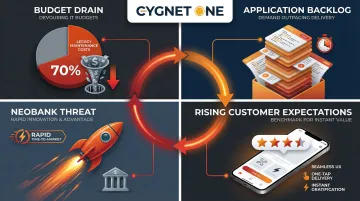

Most banks operate on core systems that are 20+ years old, held together by custom middleware and undocumented integrations. Any change risks cascading failures and requires scarce specialists who understand mainframe languages like COBOL. This creates a legacy architecture trap where modernization feels impossible.

70% of IT spending goes to maintaining existing systems, leaving just 30% for building new capabilities. Business demand for applications far outpaces IT delivery capacity. McKinsey research shows that roughly 30% of CIOs believe over 20% of their budget for new products is diverted to resolving tech debt — directly constraining throughput and growing application backlogs.

This delivery gap widens as competitive pressure mounts. Over 700 digital challengers — neobanks and fintech specialists — have launched in the past decade globally, many built entirely on modern cloud infrastructure. The threat isn't just new entrants. Bain & Company research found that consumers now benchmark banks against Amazon's seamless digital experience, not other financial institutions. Banks failing to deliver instant, mobile-first services are already losing loyalty and market share.

The pattern is consistent across markets:

- Legacy systems absorb most of the IT budget, leaving little room for innovation

- Application backlogs grow faster than traditional development can clear them

- Neobanks and fintechs outpace incumbents on speed-to-market for new features

- Customer expectations, shaped by consumer tech, keep rising regardless of bank size

What Makes Low-Code Different for Banking

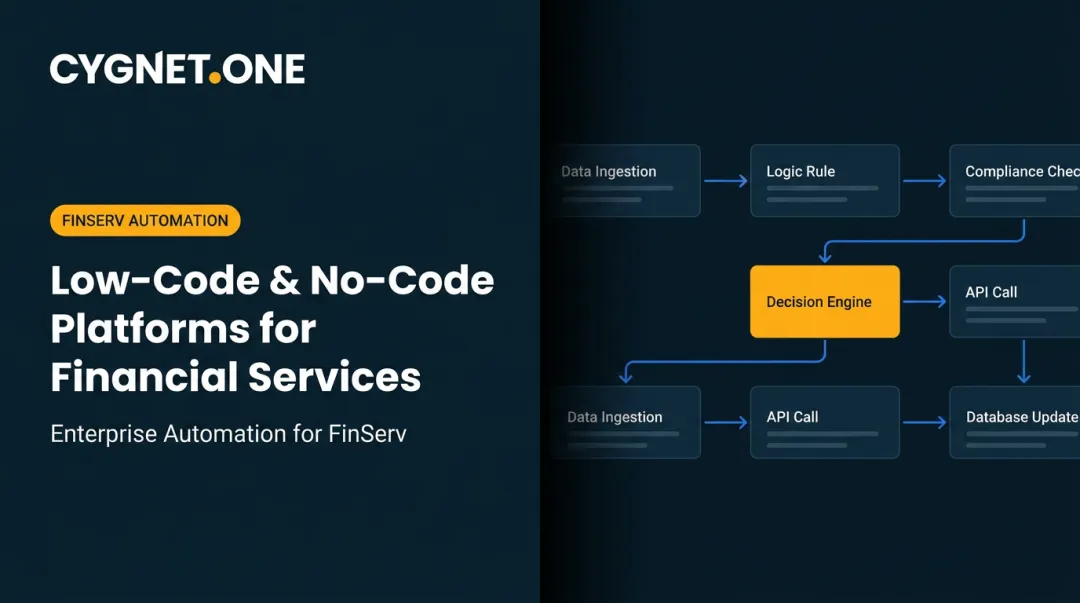

Low-code platforms combine visual drag-and-drop builders, pre-built components, and configurable workflows so both developers and domain experts can build, test, and deploy applications far faster than traditional coding. Gartner defines Enterprise Low-Code Application Platforms (LCAPs) as tools that accelerate delivery through model-driven design, generative AI, and component catalogs — a definition that maps directly onto banking's need for speed without sacrificing control.

The Bridge Model, Not Replacement

Low-code does not require ripping out core banking systems. Instead, it creates a modern application layer on top of legacy infrastructure through:

- Pre-built connectors and API gateways that expose core banking functions

- Microservices architecture that isolates new capabilities from legacy systems

- Integration platforms that orchestrate workflows across multiple backends

Banks preserve decades of regulatory logic and embedded business rules while modernizing the customer-facing experience.

Compliance-by-Design Advantage

Leading low-code platforms embed security controls natively:

- Role-based access controls and approval workflows

- Complete audit trails for every transaction and change

- Configurable compliance rules that update as regulations evolve

- Data encryption and residency controls for regulated markets

Meeting KYC, AML, and data privacy requirements becomes a configuration task rather than a custom development project.

Citizen Developer Enablement

Low-code allows banking operations experts, compliance analysts, and business analysts to configure and maintain applications themselves. Research shows that 87% of enterprise developers use low-code for at least some of their work — adoption driven by real delivery pressure, not hype.

Application demand in banking is outpacing developer supply, and global workforce forecasts project a tech talent shortage of 85.2 million workers by 2030. Low-code reduces that bottleneck by shifting IT focus toward governance, standards, and complex integrations — rather than routine build requests.

Reusability and Scalability

Components built once — forms, workflows, document verification modules — can be reused across multiple banking products and channels. Each reused component cuts build time on the next project, so the productivity advantage grows with every deployment cycle.

Key Use Cases: Where Low-Code Delivers the Most Value in Banking

Banks and NBFCs see the fastest ROI from low-code adoption in five core areas — each targeting a process where legacy systems create the most friction, cost, or compliance risk.

Digital Customer Onboarding and KYC

Low-code enables end-to-end digital account opening:

- Mobile-friendly forms with real-time validation

- Automated document verification and identity checks

- Instant account creation and activation

- Integrated KYC workflows with audit trails

Traditional onboarding takes days or weeks and requires branch visits. Digital onboarding compresses this to minutes or hours — research shows 63% of customers abandon applications that take too long.

Fully digitized onboarding workflows have demonstrated turnaround time reductions of up to 80%, a figure Cygnet.One has achieved with NBFC clients through end-to-end automation of KYC and account activation steps.

Loan Origination and Credit Assessment

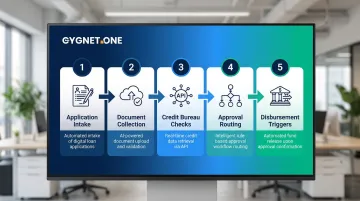

Low-code workflows automate the entire loan journey:

- Application intake - Digital forms with pre-filled data from existing systems

- Document collection - Automated upload, verification, and classification

- Credit bureau checks - Real-time API calls to CIBIL, Experian, or CRIF

- Approval routing - Configurable decisioning rules and escalation workflows

- Disbursement triggers - Automated account setup and fund transfer

Traditional loan processing takes weeks or months. Digitized workflows reduce this to hours or days, with reported turnaround time reductions ranging from 30% to 75%.

Compliance Reporting and Regulatory Workflow Automation

Low-code transforms compliance from a reactive, IT-dependent process to a configurable, business-managed workflow:

- Automated data pulls from multiple systems

- Standardized reporting formats for RBI, ECB, or other regulators

- Scheduled submissions with deadline tracking

- Instant audit trail generation for every report

The compliance burden is significant: financial institutions spend approximately $200 billion annually on financial crime compliance alone. Low-code platforms enable banks to update workflows in days when regulations change, rather than waiting months for IT to code modifications.

Fraud Detection and Real-Time Monitoring Dashboards

Low-code platforms enable banks to build real-time transaction monitoring dashboards that:

- Surface anomalies across multiple data sources

- Trigger alerts based on configurable risk rules

- Route cases for human review with full context

- Update detection logic dynamically as fraud patterns evolve

The practical shift here is speed: when a new fraud pattern emerges, compliance teams can update detection logic in hours — without waiting for a development sprint.

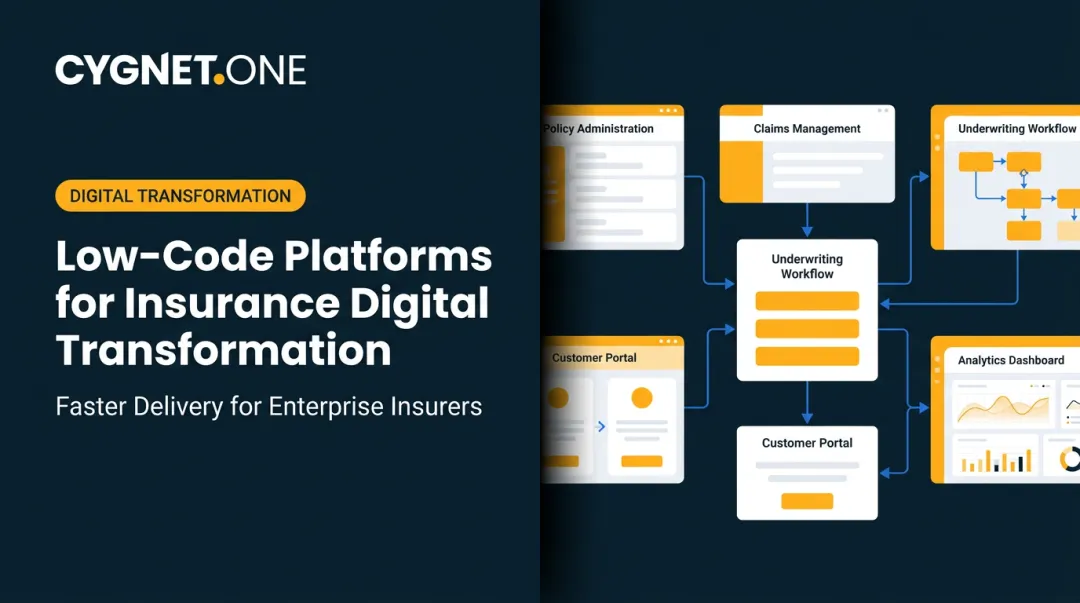

Branch and Back-Office Operations Unification

Low-code creates unified staff interfaces that pull data from multiple backend systems — core banking, CRM, cards, loans — into a single consistent view. Key operational gains include:

- Fewer screens for tellers and loan officers to navigate

- Reduced data entry errors across handoff points

- Faster service resolution at branch and contact center levels

- Consistent customer data regardless of which system was last updated

Business Benefits of Low-Code Banking Transformation

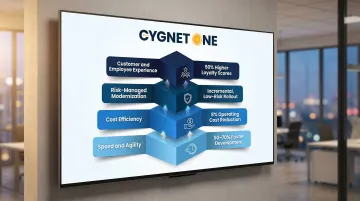

Speed and Agility

Low-code dramatically compresses development timelines. Forrester's Total Economic Impact research quantifies a 50% reduction in app development time for professional developers, while Gartner estimates 50–70% faster development for certain use cases. Applications that would take 6–12 months with traditional development teams deploy in weeks.

Cost Efficiency

Reduced dependency on large specialized development teams, reusable components, and lower maintenance overhead translate into measurable savings. Accenture modeling suggests that scaled low-code adoption could reduce operating costs by 8% for financial institutions. Faster time-to-market and stronger customer retention add to that return.

Risk-Managed Modernization

Incremental low-code adoption allows banks to prove value use-case by use-case, keeping core systems stable while building new capabilities. This contrasts sharply with high-risk "big bang" replacement approaches. Industry research indicates that 70–80% of digital transformation efforts fail, often due to attempting too much change at once. Low-code enables measured progress with controlled risk.

Improved Customer and Employee Experience

Faster digital services directly improve satisfaction metrics. Bain & Company research found that mobile-first customers give loyalty scores nearly 50% higher than customers with low digital engagement — translating into stronger deposit retention and cross-sell rates.

The gains extend internally too. Low-code tools produce simplified staff interfaces that cut training time, reduce processing errors, and lift employee productivity across branch and back-office teams.

These four benefits compound: faster delivery reduces cost, lower risk enables broader rollout, and broader rollout reaches more customers and staff.

Key outcomes banks report after low-code adoption:

- Shorter onboarding cycles for new digital products

- Reduced reliance on scarce specialist developers

- Parallel workstreams across IT and business teams

- Faster regulatory response when compliance requirements change

Challenges to Anticipate and How to Address Them

Low-code adoption in banking typically surfaces three recurring challenges: governance gaps, legacy integration complexity, and vendor risk. Addressing each one early prevents costly course corrections later.

Governance and Shadow IT Risk

Without clear ownership and guardrails, low-code can generate a wave of unmanaged applications across business units. Banks should establish a Center of Excellence (CoE) model where:

- IT sets platform standards and security policies

- Citizen developers complete mandatory training and certification

- All applications undergo security review before production deployment

- Reusable component libraries are curated and maintained centrally

Done right, the CoE becomes an enabler rather than a bottleneck — giving business teams freedom to build while IT retains visibility and control.

Integration Complexity with Legacy Cores

Low-code platforms handle most integrations through pre-built connectors, but core banking systems — Finacle, Flexcube, TCS BaNCS — often expose proprietary protocols that require deliberate planning. Banks should:

- Audit integration requirements early in the planning phase

- Prioritize platforms with strong financial services connector libraries

- Invest in API gateway infrastructure to expose core banking functions securely

- Consider specialized mainframe adapters for protocols not supported natively

Security and Vendor Lock-in Considerations

Regulatory scrutiny in BFSI makes vendor evaluation more consequential than in other sectors. Banks must assess low-code platforms against their data residency requirements, third-party risk frameworks, and exit strategies. Prioritize vendors with:

- SOC 2 Type II compliance and banking-grade security certifications

- Encryption standards for data at rest and in transit

- Open API architectures that prevent vendor lock-in

- Clear data portability and export capabilities

- Support for on-premises or private cloud deployment where required

How to Start Your Low-Code Banking Transformation

Start with One High-Value, Bounded Use Case

Don't try to transform everything at once. Select a single process with clear success metrics:

- Digital onboarding for a specific product line

- Loan origination for a particular loan type

- Compliance reporting for one regulatory requirement

Ship it quickly, prove ROI with real numbers, then expand to the next process. Institutions that follow this sequence — including NBFCs and banks that Cygnet.One has helped modernize — consistently find that early wins unlock executive support for broader adoption.

Build Your Governance Framework First

Before going wide, establish:

- Approved platform standards covering permitted tools and deployment models

- Citizen developer certification programs to build consistent skill levels

- Mandatory security reviews at design, development, and deployment stages

- A centrally managed component library of pre-approved, reusable building blocks

This ensures that scale doesn't create new technical debt.

Define Metrics and Iterate

With governance in place, the next step is measurement. Set baselines for your first use case before launch:

- Processing time (application to decision)

- Error rate (manual corrections required)

- Cost per transaction

- Customer satisfaction scores

Review outcomes at the 60-90 day mark. Those results — not assumptions — should drive which process you modernize next. A loan origination pilot that cuts turnaround time by 50%, for instance, makes a far more persuasive case to leadership than any roadmap slide.

Frequently Asked Questions

What is low-code in the context of digital banking transformation?

Low-code refers to development platforms that use visual tools, pre-built components, and configurable workflows to let banks build and deploy applications faster — without requiring large teams of specialized developers or replacing core banking infrastructure.

How does low-code help banks modernize legacy systems?

Low-code does not replace legacy systems but wraps around them, creating modern application layers connected via APIs and pre-built connectors. This allows banks to deliver new digital experiences while legacy cores continue running unchanged.

What are the most common low-code use cases in banking?

The top applications are digital customer onboarding and KYC automation, loan origination and credit assessment workflows, compliance reporting and regulatory submissions, real-time fraud monitoring dashboards, and unified branch operations interfaces.

How does low-code help banks meet regulatory compliance requirements?

Low-code platforms embed audit trails, role-based access controls, and configurable approval workflows natively. This makes it faster to implement and update compliance processes as regulations change — with full traceability built in.

Can smaller banks and NBFCs benefit from low-code, or is it only for large institutions?

Low-code is particularly well-suited for smaller banks and NBFCs because it reduces dependency on large IT teams, lowers development costs, and allows rapid deployment of targeted solutions like digital loan processing or KYC automation.

What are the main risks of adopting low-code in banking, and how can they be mitigated?

The primary risks include shadow IT from weak governance, integration friction with legacy cores, and vendor security gaps. A Center of Excellence model addresses governance, while early integration audits and banking-grade vendor evaluation keep the other two in check.