Introduction

Finance leaders are under real pressure right now. Boards want faster closes. Regulators want cleaner filings. And CFOs are expected to deliver strategic insight, not just accurate month-end numbers. The problem: too many finance teams are still buried in manual work.

According to a 2024 PwC Baltic CFO Survey, 63% of financial planning and budgeting activities remain fully or mostly manual — with 12% fully manual and 51% mostly manual. That's the majority of core finance work still running on human effort, spreadsheets, and email chains.

Manual processes create compounding problems: errors that cascade through reporting, compliance filings that miss deadlines, and finance talent wasted on data entry instead of analysis.

This guide covers what finance process automation (FPA) actually is, which processes to prioritise first, how the major tool categories compare, and what to look for when evaluating vendors. By the end, you'll have a clear framework for building a business case or shortlisting the right solution.

Key Takeaways

- Finance process automation uses technology — RPA, AI, and cloud platforms — to handle repetitive financial tasks with minimal human input, reducing errors and freeing teams for strategic work.

- Highest-ROI automation targets: accounts payable, accounts receivable, payroll, reconciliation, and compliance reporting.

- Main tool categories include RPA platforms, AI/ML-powered automation, ERP systems, and specialized compliance and e-invoicing platforms.

- Vendor evaluation must include compliance credentials, ERP integration depth, security certifications, and scalability.

- Implementation success depends on process readiness and change management as much as it does on picking the right software.

What Is Finance Process Automation?

Finance process automation (FPA) is the use of technology — software bots, AI, machine learning, and cloud platforms — to execute repetitive financial tasks with minimal human intervention. That covers everything from scanning an invoice and routing it for approval, to generating a consolidated P&L report across 12 entities.

Automating a specific task (like invoice capture) is not the same as end-to-end finance transformation. Most organizations start with task-level automation and expand from there — the table below shows why that first step already delivers measurable gains.

Manual vs. Automated Finance Workflows

The gap between manual and automated workflows is measurable and significant.

| Dimension | Manual Workflow | Automated Workflow |

|---|---|---|

| Speed | Slow, dependent on headcount | Real-time or near-real-time |

| Error rate | High — data re-entry introduces mistakes | Consistent, validated at source |

| Scalability | Requires more staff as volume grows | Scales without adding headcount |

| Audit trail | Fragmented, hard to reconstruct | Complete, timestamped, exportable |

| Compliance | Reactive — errors found after the fact | Proactive — validated before submission |

What's Driving Adoption Now

Finance automation has moved from optional upgrade to operational priority. Several converging pressures explain why:

- Regulatory mandates — e-invoicing is now mandatory in India, Saudi Arabia, UAE, and increasingly across the EU, with penalties for non-compliance

- CFO pressure for faster closes — boards expect real-time financial visibility, not month-end surprises

- The shift to strategic finance — 95% of senior finance executives cite process efficiency as a key automation objective, with 76% specifically wanting to free staff for more engaging, analytical work

Key Finance Processes to Automate

No finance team can automate everything at once. The right starting point is where volume is highest, errors are most costly, and ROI is clearest.

Accounts Payable and Receivable

AP and AR consistently deliver the strongest early ROI from automation.

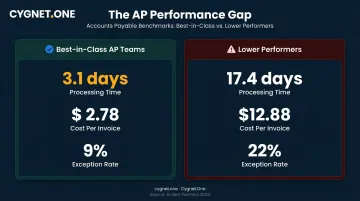

For accounts payable, automation handles invoice capture via OCR, three-way purchase order matching, approval routing, and payment processing. The performance gap is significant. According to Ardent Partners' 2024 State of ePayables report, best-in-class AP teams process invoices in 3.1 days at $2.78 per invoice. Lower performers take 17.4 days at $12.88 per invoice, with exception rates of 22% vs. 9% for top teams.

For accounts receivable, automation covers invoice generation, payment matching, dunning workflows, and cash application — reducing the time between delivery and cash receipt.

Payroll and Expense Management

Payroll is typically an organisation's largest single expenditure, which makes errors expensive. Automation covers salary calculations, deductions, tax withholding, and payslip generation — eliminating manual errors that can trigger compliance issues or employee disputes.

Expense management automation addresses a different set of pain points:

- Receipt scanning and OCR extraction

- Automated policy validation (flagging out-of-policy claims before reimbursement)

- Approval routing without email chains

- Direct integration with payroll for reimbursement

The combined impact is faster reimbursements, cleaner audit trails, and fewer policy violations that finance teams have to chase manually.

Financial Close and Reconciliation

Month-end close is one of the most time-pressured and error-prone activities in finance. The APQC benchmark puts the median monthly close at 6 days, with top performers completing it in 4.8 days or less. Finance shared services centres tend to run slower, at a median of 8 days.

Automation compresses this timeline by handling:

- Bank reconciliation and intercompany matching

- Journal entry creation from transactional data

- Variance flagging and exception reporting

- Financial statement generation directly from ERP data

The result is less time spent assembling data and more time spent reviewing it.

Compliance, Tax Reporting, and E-Invoicing

This is the most consequential automation category for enterprises operating across multiple geographies — and the most underestimated.

E-invoicing is now a legal requirement in several major markets:

- India: GST e-invoicing mandatory for businesses above turnover thresholds, with IRN generation required at the time of invoicing

- Saudi Arabia: ZATCA Phase 2 integration enforcement is ongoing, with fines starting at SAR 5,000 for non-generation of e-invoices

- UAE: Ministry of Finance e-invoicing programme is active, with FTA regulatory oversight

- Europe: EU ViDA directive entered into force in April 2025, enabling member states to mandate e-invoicing

For multi-geography enterprises, automating tax calculations, e-invoice generation, and regulatory submissions isn't just an efficiency play — it's a legal risk management decision. A missed filing or a non-compliant invoice format can trigger penalties, audit scrutiny, and reputational damage.

Reporting, Forecasting, and FP&A

Gartner reported that 58% of finance functions were using AI in 2024, up 21 percentage points from 2023 — largely driven by demand for faster, more automated financial narratives.

Automated reporting tools consolidate real-time data from ERPs and business systems to produce:

- CFO-ready dashboards with live financial metrics

- Variance analyses flagging actuals vs. forecast

- Rolling cash flow forecasts updated automatically

When reporting runs on automation, finance teams stop building spreadsheets and start driving decisions. That shift — from data assembly to strategic analysis — is where FP&A automation pays for itself.

Finance Automation Tools: Categories and Technologies

No single platform automates every finance process. Selection depends on workflow type, data structure, volume, and the degree of human judgment required.

Robotic Process Automation (RPA)

RPA uses software bots to mimic human actions on structured, rule-based tasks: logging into systems, copying data between fields, generating and distributing reports. It's best suited to high-volume, repetitive workflows where the logic doesn't change.

RPA's limitation is its rigidity. Bots follow fixed rules — they can't handle unstructured data, ambiguous inputs, or processes that vary significantly from case to case. When an invoice arrives as a scanned PDF with a non-standard layout, basic RPA struggles.

Leading platforms recognized by Gartner and Forrester in this category include UiPath, Automation Anywhere, and SS&C Blue Prism — all flagged as Leaders in the 2024 Gartner Magic Quadrant for Robotic Process Automation.

AI and Machine Learning-Powered Automation

AI and ML extend automation beyond rule-based tasks. These platforms can:

- Extract data from unstructured documents (scanned invoices, contracts, remittance advices) using intelligent document processing

- Detect anomalies in transaction data that may indicate fraud or error

- Learn from historical approval patterns to predict likely outcomes

- Generate variance explanations and narrative commentary in natural language

Unlike pure RPA, AI-powered tools improve as they process more data — and they handle format variation and edge cases that would break a rule-based bot. In a 2023 BlackLine survey, 78% of finance and C-suite professionals viewed generative AI as critical for streamlining financial operations.

ERP Systems and Finance Platforms

ERPs — SAP, Oracle, Microsoft Dynamics, and others — serve as the backbone of finance automation by integrating AP, AR, payroll, inventory, and reporting into a unified data model. Without a well-configured ERP, most automation efforts produce fragmented results.

The critical consideration when adding automation tools on top of an ERP is integration depth. API-native, real-time connectors outperform file-based batch integrations — both in data freshness and in failure handling. Panorama Consulting's 2024 ERP Report found that only 49% of ERP projects completed within the expected timeframe, making pre-built connectors a safer bet than custom integrations built from scratch.

Specialized Compliance and E-Invoicing Platforms

For enterprises in regulated markets, ERP functionality alone isn't sufficient. Compliance with e-invoicing mandates requires platforms that are government-recognized, maintain real-time connections to regulatory portals, and can handle jurisdiction-specific validation rules.

Cygnet.One is an example of this category. The platform holds accreditations across multiple jurisdictions:

- India: GSTN-approved IRP and GSP

- Saudi Arabia: ZATCA recognized

- UAE: FTA recognized

- UK: HMRC recognized

- Malaysia, Belgium, Singapore: MDEC, BOSA, and IMDA accredited

With 250+ ERP integrations and over 1.7 billion e-invoices generated — roughly 19% of India's total e-invoice volume — the platform handles compliance at a scale most custom-built connectors can't match. For multi-geography enterprises, deploying pre-built, government-recognized infrastructure cuts implementation risk and time compared to building jurisdiction-specific connectors from scratch.

How to Evaluate and Choose the Right Finance Automation Vendor

With hundreds of vendors in the market, a structured evaluation framework prevents both overspending and under-selecting.

Start with a process audit: identify your highest-volume, most error-prone workflows, and rank them by ROI potential before you shortlist a single vendor. Buying automation for a process you haven't cleaned up first is one of the most common (and expensive) mistakes finance teams make.

Compliance Credentials and Regulatory Recognition

In regulated markets, vendor compliance credentials are non-negotiable. Treat them as a baseline requirement, not a differentiator.

Questions to ask every vendor:

- Are you government-recognised in each geography where we operate?

- Can you provide proof of GSTN, ZATCA, FTA, or HMRC recognition?

- How quickly do you update your platform when regulations change?

Working with an unrecognised vendor in markets like India or Saudi Arabia creates genuine legal exposure. Cygnet.One's multi-jurisdiction accreditation portfolio, built over 25 years of compliance work, is the type of credentialing that should be verified and matched against your operating geographies during vendor evaluation.

ERP Integration Depth and Implementation Speed

Don't just confirm that a vendor integrates with your ERP — ask exactly how they do it.

Key questions:

- Is the integration API-native or file-based?

- Does it sync in real time or in batch?

- What happens when the integration fails — is there automatic retry and alerting?

- How long does implementation actually take?

Cygnet.One's e-invoicing implementations typically go live within 8 to 10 weeks, with pilot deployments starting in weeks using file-drop templates before API rollout. That's a meaningful benchmark, given that ERP projects routinely extend to 15+ months.

Security Standards and Data Governance

Financial data demands verified security controls, not vendor assurances. Key certifications to require:

- SOC 2 Type II — validates security controls over an observation period

- ISO 27001:2022 — information security management system certification

- GDPR compliance — essential for any vendor processing EU-resident data

Also ask about:

- Audit trail depth — retention periods and retrieval controls

- Data residency guarantees — where data is stored and whether it stays there

- Role-based access controls — who can view, edit, or export sensitive records

Cygnet.One holds SOC 2 Type II certification and ISO 27001:2022, and maintains 7-year audit logs with full metadata and retrieval control.

Scalability, Uptime, and Support

Growing enterprises need infrastructure that scales without manual intervention. Evaluate:

- Uptime SLA — 99%+ is standard; anything below 99.5% deserves scrutiny for compliance-critical workflows

- Peak load handling — can the platform process your month-end volume without degradation?

- 24/7 support — especially important when your operations span multiple time zones

- Multi-entity and multi-currency support — essential for group finance operations

Common Implementation Challenges and How to Overcome Them

Automating Broken Processes

Automation amplifies whatever exists beneath it. Automate a broken approval workflow and you get the same broken process — just running faster and harder to unwind. Before implementation, map your current workflows in detail, identify redundancies, and define the future-state process you actually want. Automate that, not the current mess.

Change Management and Employee Resistance

Finance staff often resist automation out of concern for their roles. The organisations that navigate this best position automation as augmentation — tools that remove tedious work so teams can do more valuable analysis.

Practical steps that work:

- Nominate internal change champions from within the finance team

- Set clear KPIs for the implementation so success is visible

- Provide structured training before go-live, not after

- Communicate openly about what changes and what doesn't

Data Quality and Integration Failures

Poor master data is the leading cause of automation project failure. Inconsistent vendor names, duplicate records, and chart-of-accounts errors all surface immediately when automation starts processing at volume.

Before deployment, address these directly:

- Run a data governance audit across your vendor master, customer master, and chart of accounts

- Validate all records against your ERP data model before go-live

- Confirm your chosen platform has proven, pre-built ERP connectors — not brittle custom integrations that break when a field name changes

Frequently Asked Questions

What is process automation in finance?

Finance process automation uses technology — including RPA, AI, and cloud platforms — to handle repetitive financial tasks like invoicing, payroll, reconciliation, and reporting with minimal human intervention. The goal is improved speed, accuracy, and compliance across the finance function.

What are the top 3 RPA tools?

UiPath, Automation Anywhere, and SS&C Blue Prism each earned Leader status in the 2024 Gartner Magic Quadrant for RPA. The best fit depends on your specific workflows and the degree of data irregularity involved.

What is the difference between RPA and AI in finance automation?

RPA uses rule-based bots for structured, repetitive tasks. AI-powered automation handles unstructured data, learns from historical patterns, detects anomalies, and makes adaptive decisions. The two approaches are complementary, and most mature implementations combine both.

Which finance processes should be automated first?

Start with accounts payable, invoice processing, and bank reconciliation — high-volume, structured workflows with clear ROI. Once stable, expand into FP&A automation and multi-jurisdiction compliance reporting.

How long does finance process automation implementation take?

Specialized SaaS platforms with pre-built ERP connectors can go live in weeks; full ERP-wide or custom builds typically take several months. Implementation readiness — data quality, process clarity, stakeholder alignment — is usually the deciding factor.

How do I measure ROI from finance process automation?

Track time saved per workflow, error rate reduction, exception rates, and headcount efficiency. Layer in strategic outcomes like forecast accuracy and audit readiness. ROI should be monitored continuously — not just calculated at go-live.