Introduction

Most banks are running digital-age expectations on decade-old infrastructure. Rising customer demands for real-time services, aggressive fintech competition, and tightening regulatory requirements are all arriving simultaneously — while the core systems meant to handle them were never built for this moment.

These legacy platforms — often a patchwork of mainframe applications, COBOL codebases, and bolt-on acquisitions — cannot deliver the speed and experience modern banking requires.

The cost of standing still now outweighs the cost of change. Lost market share to digital-native challengers, slow manual processes, and growing cybersecurity exposure compound every quarter.

Platform modernization in BFSI is no longer a strategic option. It is a survival imperative. Institutions that delay face shrinking margins, customer attrition, and regulatory penalties — while those that modernize open the door to new revenue streams, leaner operations, and lasting competitive advantage.

Key Takeaways

- Legacy platforms accumulate technical debt that makes every new feature slower and costlier to ship

- Three forces are pushing modernization onto bank boardroom agendas: regulatory pressure, digital-native competition, and M&A complexity

- Phased, API-led, and cloud-based strategies make modernization possible without a full system replacement

- AI, cloud infrastructure, and open APIs are the technology pillars that enable safe, incremental transformation

- Measure success across four categories: customer experience, operational efficiency, financial performance, and risk compliance

Why Legacy Banking Platforms Are Failing

The Compounding Weight of Technical Debt

Technical debt in banking operates like compound interest on deferred decisions. Every workaround, patch, and shortcut taken to keep legacy systems running accumulates deficiencies that make future changes far more expensive. What once cost weeks to implement now takes months. What required one developer now demands entire teams. This isn't merely inefficiency—it's a structural impediment to growth.

The numbers tell a stark story:

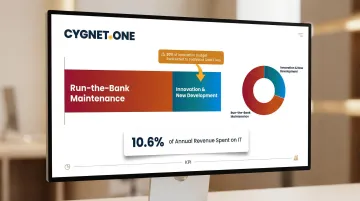

- Banks allocate 60–80% of IT budgets to "run-the-bank" maintenance, leaving just 20–40% for innovation

- Around 30% of that innovation budget gets redirected to fixing problems caused by existing technical debt

- Financial institutions spend 10.6% of revenue and 20% of total expenses on IT — yet still struggle to launch new products or respond to market shifts

The Cobbled Systems Problem

Many banks have grown through acquisition, inheriting multiple disconnected core systems that were integrated through data aggregation rather than true unification. This creates a "Frankenstein" infrastructure where customer data, product definitions, and transaction histories exist in incompatible formats across disparate platforms. A complete view of each customer's accounts, history, and preferences becomes nearly impossible without significant manual effort — directly undermining cross-sell opportunities and personalized service delivery.

Beyond service gaps, these architectures carry serious operational risk. A single severe core outage can put $5–15 million in revenue at risk for a large bank. High-profile failures at TSB Bank (resulting in £48.65 million in fines) and RBS demonstrate how fragile these architectures have become.

The Vanishing Talent Pool

The industry still relies on billions of lines of COBOL code — IBM estimates 250 billion lines remain in production globally. Yet the engineers who built these systems are retiring, and modern developers lack familiarity with legacy languages. A 2025 survey found 39% of mainframe users experiencing pressure from the skills gap.

This creates key-person risk, increased change-failure rates, and lengthened mean time to repair (MTTR) during outages. Routine maintenance becomes increasingly risky, and institutions face growing reliance on costly third-party outsourcers.

What's Driving Platform Modernization in BFSI

Digital-Native Customer Expectations

Millennials and Gen Z expect banking to be as seamless as any other digital experience. Nearly 70% have authorized data sharing with third-party providers—a clear signal of appetite for open banking and embedded finance.

What makes this particularly urgent: these generations show the highest propensity to switch banks, even when satisfied. Digital experience quality has become a primary retention lever, not a differentiator.

Legacy monolithic platforms—built for batch processing and branch-based delivery—cannot keep pace with these demands. Real-time account updates, instant credit decisions, and personalized financial insights require event-driven architectures that most legacy cores were never designed to support.

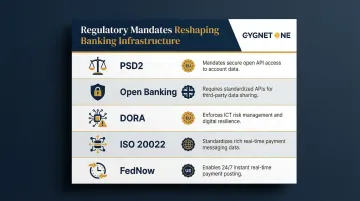

Regulatory Mandates Forcing Architectural Change

A wave of regulations since 2016 has forced banks to modernize infrastructure that was never designed for dynamic compliance environments:

- PSD2 (EU) mandates secure APIs for third-party access to customer accounts

- Open Banking (UK) requires standardized API implementations across major banks

- DORA (EU) establishes comprehensive ICT risk management and resilience testing requirements

- ISO 20022 migration demands support for richer, structured payment data and real-time settlement

- FedNow (US) requires 24/7 real-time posting and immediate funds availability

These mandates require fundamental changes to core ledgers, API gateways, consent management, and audit capabilities—none of which legacy infrastructure can absorb without structural overhaul.

M&A Activity and the Consolidation Imperative

Banking M&A rebounded sharply in 2024-2025, with US banking deals reaching $16.3 billion in 2024 and Q3 2025 alone recording $16.63 billion in transactions. Each merger forces a critical decision: continue bolting on acquired platforms (worsening technical debt) or consolidate onto a modern core.

The cost of delay is steep:

- Core conversion overruns: Integration projects routinely exceed initial estimates by 50–100%

- UBS/Credit Suisse (2023): Flagged up to $28.3 billion in potential negative impact with a 3–4 year IT integration timeline

- Root cause: Harmonizing customer data, product definitions, and transaction histories across dissimilar legacy cores compounds cost at every stage

Banks that enter mergers with modern, API-first platforms cut integration timelines significantly—and avoid the compounding technical debt that makes the next merger even harder to absorb.

Core Modernization Strategies

Strategy 1: Phased / Sequential Migration

Phased migration modernizes one legacy core at a time, mapping each product line or business unit to the new platform progressively. Commonwealth Bank of Australia executed an 18-month phased migration of its SAP-based core to the cloud, achieving sub-two-minute failover capability with minimal disruption to 16 million customers.

This approach suits banks that have grown through acquisitions — risk is contained to individual product lines, and early phases generate lessons that sharpen later rollouts. The trade-off: parallel systems run for years, which increases both complexity and cost.

Strategy 2: Big-Bang Full Replacement

Big-bang replacement cuts over all legacy systems to a new core on a single date — the fastest path to unified operations and immediate cost reduction. Midbank in Egypt completed a big-bang go-live in 2025 with Temenos solutions, delivering reduced transaction times and improved efficiency.

When planned with exhaustive testing, staff training, and rollback procedures, big-bang delivers a clean end-state quickly. Execution risk, however, is severe. TSB Bank's 2018 failure locked millions of customers out of accounts, resulting in £48.65 million in fines and lasting reputational damage — a reminder that this strategy demands high risk tolerance and rigorous preparation.

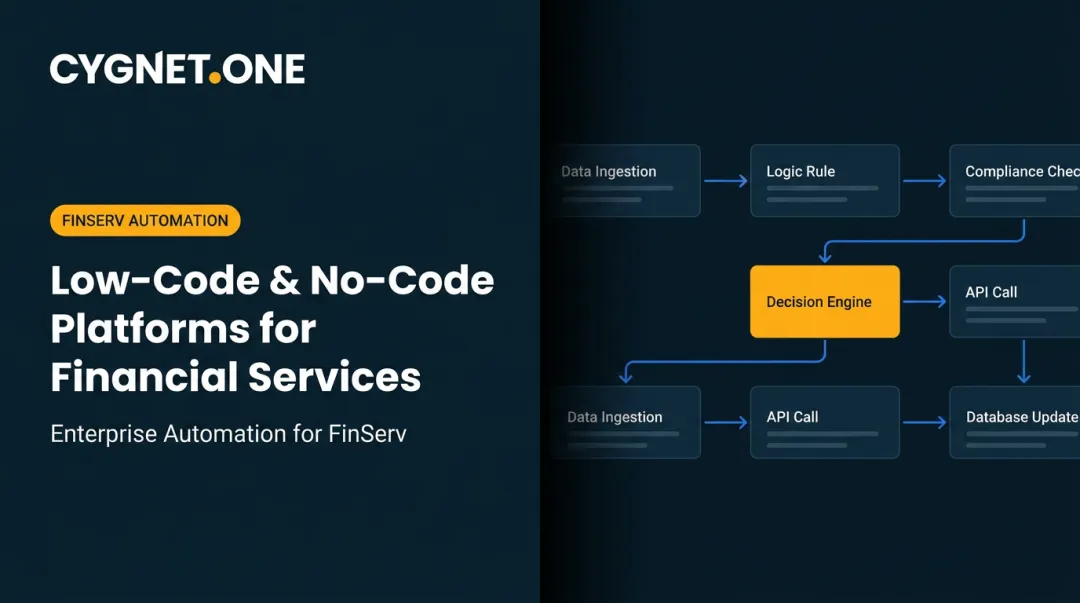

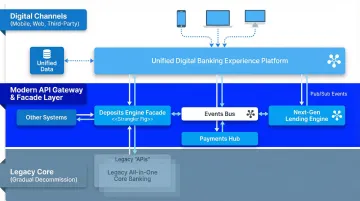

Strategy 3: API-Led Modernization (Strangler Fig)

API-led modernization wraps legacy cores with modern APIs, letting new features and channels run on modern infrastructure while the back end is gradually decommissioned. BBVA's API Market brought in 11.1 million new digital customers in 2023 — 65% via digital channels — and cut onboarding to minutes. DBS Bank took a similar path, decomposing monolithic systems into microservices to unlock faster product delivery and real-time capabilities.

Institutions can deliver new digital experiences immediately while de-risking the back-end migration — the core stays live throughout. The downside is that technical debt and legacy maintenance costs persist until decommissioning is complete.

Strategy 4: Cloud-Native Greenfield Stack

Greenfield approaches launch a separate modern banking entity on a fully cloud-native stack while the legacy business continues uninterrupted. Mox Bank (by Standard Chartered) launched in Hong Kong with Thought Machine's Vault core on AWS, achieving 50% customer base growth in four months. Starling Bank and Monzo built entirely on cloud platforms, enabling faster product launches and lower customer acquisition costs.

Greenfield eliminates legacy constraints entirely — institutions can test modernization at speed without touching the core business. The cost of running parallel operations is real, though, and eventual consolidation with the legacy estate adds future complexity.

Selecting the Right Strategy

No single approach fits all institutions. The right strategy depends on:

- Institution size and complexity — larger, more complex banks favor phased approaches

- Degree of technical debt — heavily customized cores may require greenfield or big-bang

- Risk appetite — risk-averse institutions prefer phased or API-led strategies

- Regulatory environment — DORA and resilience mandates influence architecture choices

- Available budget and talent — phased approaches spread costs but require sustained investment

Leading analysts recommend a portfolio approach, selecting strategies per product line or domain rather than applying one model enterprise-wide.

Technology Enablers: AI, Cloud, and APIs Powering Modern Banking

AI and Machine Learning for Modernization and Operations

Generative AI is accelerating legacy code modernization by analyzing, translating, and refactoring COBOL code, reducing dependence on scarce specialists. McKinsey documented a 40% boost in developer productivity using GenAI tools for legacy code analysis. In operations, 72% of organizations have adopted AI in some form, with 65% using GenAI regularly.

AI is most mature in fraud detection, where ML models enable anomaly detection and real-time risk decisions. HSBC reported a 60% reduction in case volumes for AML and fraud detection using AI-powered platforms. Credit decisioning also benefits, with AI ingesting documentation, drafting credit memos, and enhancing risk scoring models.

Cloud Infrastructure as the Backbone

The shift from on-premise data centers to hybrid and multi-cloud environments is now foundational for modern banking operations. Gartner forecasts that 90% of organizations will adopt hybrid cloud by 2027. Cloud infrastructure delivers elastic scalability, geographic redundancy, and faster deployment cycles that fixed on-premise capacity simply cannot match.

Commonwealth Bank's cloud migration engineered sub-two-minute failover capability, a measurable leap in operational resilience. Cloud-native platforms enable banks to shift from CAPEX to OPEX cost models, though actual savings depend heavily on migration strategy and require institution-specific TCO modeling.

Open APIs and Composable Banking

Modern platforms use open API frameworks to integrate with fintechs, third-party data providers, and regulatory systems. The UK's Open Banking ecosystem demonstrates maturity: 99.59% API availability, 328ms average response times, and 2.23 billion successful calls in February 2026 across 145 third-party providers.

Platforms achieving 250+ ERP integrations—like those deployed by firms including Cygnet.One—illustrate the scale of interoperability now expected across the financial ecosystem. APIs enable composable banking, where institutions assemble best-of-breed services rather than relying on monolithic suites. That same interconnectivity is what makes real-time data infrastructure viable at scale.

Real-Time Data Infrastructure

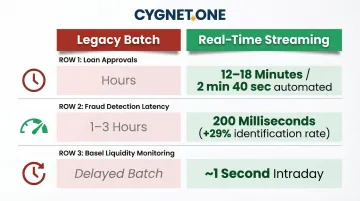

Replacing batch-processing pipelines with real-time streaming and event-driven architectures unlocks capabilities that batch systems structurally cannot deliver. Key performance gains reported across implementations include:

- Loan approvals: Dropped from hours to 12–18 minutes; one institution processes 70% of applications fully automatically in 2 minutes 40 seconds

- Fraud detection latency: Reduced from 1–3 hours in batch environments to 200 milliseconds in streaming architectures, with identification rates up 29%

- Basel liquidity monitoring: Intraday metrics computed within approximately one second, enabling live compliance reporting

These gains compound: faster decisions reduce operational cost while real-time compliance reporting reduces regulatory exposure simultaneously.

Cybersecurity and Compliance by Design

Modern platforms must embed security and compliance—SOC certifications, regulatory API connections, audit trails—at the architecture level rather than as bolt-ons. Institutions that treat compliance as a native capability gain structural advantages in regulated markets.

DORA raises the bar further, mandating comprehensive ICT risk management, incident reporting, and resilience testing. Platforms must maintain inventories of information assets with auditable data lineage and tested Recovery Time Objectives (RTO) and Recovery Point Objectives (RPO) for each business function.

Measuring Success: KPIs for Banking Platform Modernization

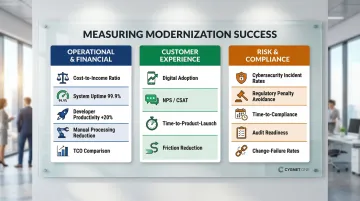

Modernization without measurement is just change for its own sake. Tracking the right KPIs across three dimensions — customer experience, operational efficiency, and risk — gives institutions a clear picture of whether their investment is delivering.

Customer Experience KPIs

Track metrics that directly reflect customer impact:

- Digital adoption rates — percentage of transactions completed via digital channels

- Customer satisfaction scores — NPS and CSAT measurements post-modernization

- Time-to-product-launch — weeks or months from concept to market

- Friction reduction — account opening time, loan approval speed, payment processing latency

Institutions achieving 12-18 minute loan funding times or 2-minute credit decisions represent concrete benchmarks for customer experience improvement.

Operational and Financial Performance KPIs

Monitor efficiency gains and cost impacts:

- Cost-to-income ratios — target 15-20% reduction in cost base

- System uptime — 99.9% SLA benchmarks are industry standard

- Developer productivity — 20% uplift in feature delivery velocity

- Manual processing reduction — percentage of automated workflows

- Total cost of ownership — compare against legacy baseline

A Forrester Total Economic Impact study for ClearBank — a UK-based cloud-native bank — documented 90% ROI with a 10-month payback period and £4.8 million net present value.

Risk and Compliance KPIs

Track regulatory and security metrics:

- Cybersecurity incident rates — frequency and severity of security events

- Regulatory penalty avoidance — fines prevented through improved compliance

- Time-to-compliance — speed of implementing new regulatory requirements

- Audit readiness — percentage of audit requirements met on-demand

- Change-failure rates — stability of production deployments

In practice, regulators and boards are asking for this data — institutions that track it proactively spend less time firefighting audits and more time executing their roadmap.

Frequently Asked Questions

What is platform modernization in banking?

Platform modernization is the process of replacing or upgrading legacy core banking systems, data infrastructure, and operational processes with modern, cloud-native, API-driven, and AI-enabled technology. It aims to improve efficiency, agility, and customer experience while reducing technical debt and operational risk.

What is technical debt in banking, and why does it matter?

Technical debt is the accumulated cost of shortcuts and deferred updates in legacy code. It compounds over time like interest, making new feature development slower, riskier, and more expensive. Left unchecked, it consumes innovation budgets and raises change-failure rates—eroding a bank's ability to compete.

What is the difference between core banking modernization and digital transformation?

Core banking modernization focuses on replacing or upgrading foundational transaction-processing systems: the ledgers, payment engines, and product processors. Digital transformation is broader—covering customer channels, processes, culture, and technology strategy—and typically requires modernization as a foundation before it can succeed.

How long does a banking platform modernization project typically take?

Timelines vary based on institution size, strategy, and degree of technical debt. Phased approaches may span 3-5 years, while API-led modernizations deliver results incrementally within months; big-bang replacements typically need 12-24 months of preparation before cutover.

How does AI accelerate banking platform modernization?

AI automates legacy code analysis and migration, enabling developers to understand and refactor COBOL systems 40% faster. It also powers intelligent credit decisions, real-time fraud detection, and data quality validation—while GenAI accelerates documentation review and technical specification drafting.

Should banks modernize their core all at once or in phases?

There is no universal answer. Big-bang replacements deliver speed and a clean end-state but carry high execution risk, while phased or API-led approaches reduce risk at the cost of longer timelines. The right choice depends on the institution's risk appetite, available resources, and strategic urgency.