Introduction

Most banks and NBFCs are still running core systems built for a world that no longer exists — on-premise infrastructure that can't scale fast enough, can't integrate cleanly with modern fintech, and increasingly struggles to meet RBI, SEBI, and IRDAI compliance mandates as they evolve. Cloud migration is how financial institutions close that gap.

Cloud migration in financial services means moving financial data, applications, and infrastructure from legacy or on-premise systems to cloud-based environments. For CIOs, CTOs, and digital transformation leaders at banks, NBFCs, insurance firms, and fintech companies, this is uniquely complex territory. Stringent regulatory obligations, extreme data sensitivity, and always-on operational requirements make it a high-stakes, multi-year undertaking — not a standard IT lift-and-shift.

This guide covers:

- What cloud migration means specifically for financial services

- Why adoption is accelerating despite regulatory complexity

- How the migration process works, step by step

- The core challenges and how to navigate them

- How to choose the right migration model for your organization

Whether you're evaluating a full public cloud strategy or a hybrid approach, this guide gives you the framework to make that call with confidence.

Key Takeaways

- Cloud migration moves banking, lending, insurance, and compliance workloads from legacy systems to scalable cloud environments

- Firms migrate primarily for agility, cost optimisation, real-time data processing, and meeting evolving regulatory demands

- Migration follows six stages: assess, plan, pilot, migrate, validate, and optimise, with compliance checkpoints built into each phase

- Key challenges include data sovereignty, multi-jurisdiction compliance, legacy system complexity, and talent shortages

- Hybrid cloud approaches often deliver better outcomes than full migration for institutions with mission-critical legacy workloads

What Is Cloud Migration in Financial Services?

Cloud migration in financial services is the structured process of transferring financial systems—including core banking platforms, lending engines, compliance infrastructure, and payment systems—to cloud environments, whether public, private, or hybrid. The goal is moving from capital-intensive, inflexible on-premise infrastructure to scalable, pay-as-you-go cloud architecture.

Done well, migration enables real-time transaction processing, faster product launches, and more efficient regulatory reporting. Rather than maintaining expensive data centres with fixed capacity, financial institutions gain elastic infrastructure that scales with demand—critical during peak periods like quarter-end reporting or loan disbursement surges.

Cloud migration differs from related concepts:

- Cloud-native development builds applications from scratch on cloud platforms, while migration moves existing systems

- Digital transformation represents a broader strategic shift across business models, whereas migration focuses specifically on infrastructure relocation

- Data centre consolidation consolidates physical hardware footprints—cloud migration goes further by modernizing how workloads are delivered entirely

Why Financial Services Firms Are Moving to the Cloud

Financial services firms are shifting from viewing cloud primarily as a cost-reduction tool to recognizing it as an engine for revenue growth and innovation. Global IT spending in banking is projected to reach $793.5 billion in 2025, growing 8.4%, reflecting sustained investment in cloud capabilities.

Operational Demands Unique to Financial Services

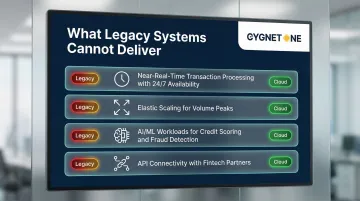

Legacy infrastructure cannot keep pace with what modern financial institutions actually need:

- Near-real-time transaction processing with 24/7 availability

- Elastic scaling to handle cyclical volume peaks (tax seasons, quarter-end surges)

- AI/ML workloads for credit scoring, fraud detection, and risk analytics

- API connectivity with fintech partners and third-party data providers

Cloud infrastructure supports all of these. Legacy systems do not.

The Cost of Standing Still

Financial institutions typically spend 60-80% of IT budgets on legacy system maintenance, leaving almost nothing for innovation. Core banking platforms average 20-30 years old, and 43% of US banks still run COBOL-based systems.

The operational cost shows up quickly: slower product releases, inability to integrate with fintech APIs, fragmented customer data, and manual compliance reporting that consumes staff hours better spent elsewhere.

Regulatory and Competitive Pressure

Regulators including RBI, FCA, SAMA, and CBUAE are issuing cloud-specific guidelines — pushing institutions to formalize cloud governance rather than avoid it. This is no longer optional in many jurisdictions.

At the same time, fintech revenues are projected to grow nearly three times faster (~15% annually) than traditional banking (~6% annually) between 2022 and 2028. That gap is largely a cloud agility gap. For institutions in India, the Middle East, and Europe, the question is no longer whether to migrate — it's how fast.

How Cloud Migration Works: A Step-by-Step Process for Financial Institutions

Cloud migration for financial institutions is a phased, risk-managed program that typically spans months to years. Each phase builds on the last, covering:

- Workload assessment and cloud readiness

- Strategy design and target architecture

- Compliance and security mapping

- Migration execution and data validation

- Post-migration optimization and governance

Phase 1: Portfolio Assessment and Cloud Readiness

The first step involves auditing all existing applications, systems, and data assets to determine cloud suitability. Institutions categorize workloads into three groups:

- Cloud-ready: Reporting tools, compliance dashboards, e-invoicing systems requiring minimal modification

- Cloud-adaptable: Applications requiring refactoring, such as customer-facing mobile banking or fraud detection platforms

- Cloud-unsuitable: Legacy core systems that must remain on-premise or be replaced entirely

Tax and compliance platforms are natural early candidates. Cygnet.One's cloud-native infrastructure, for instance, processes 55 million transactions per month and has generated over 412 million e-invoices — the kind of compliance-ready workload profile that sets a realistic benchmark for financial institutions planning their first migrations.

Phase 2: Strategy Design and Target Architecture

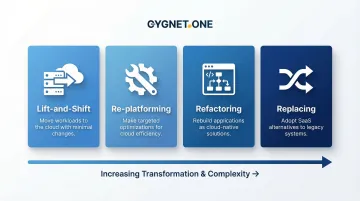

Financial institutions select their migration strategy based on workload type, regulatory constraints, and business objectives:

- Lift-and-shift: Moving applications with minimal changes

- Re-platforming: Making targeted optimizations during migration

- Refactoring: Rebuilding applications to be cloud-native

- Replacing: Adopting SaaS alternatives

Target architecture — public, private, hybrid, or multi-cloud — is defined based on data sovereignty requirements and operational risk tolerance. Over 85% of enterprise organizations have adopted hybrid or multi-cloud strategies to balance agility with security and compliance.

Phase 3: Compliance and Security Mapping

Before any data moves, financial institutions must map every workload to applicable regulatory requirements — data residency rules, encryption standards, audit trail requirements, and third-party risk management obligations.

For multi-geography institutions operating across India, UAE, UK, and Saudi Arabia, this step must account for multiple regulatory frameworks simultaneously:

- India: RBI data localization mandates for payment systems

- UAE: CBUAE requirements for master system records within national borders

- Saudi Arabia: SAMA approval-based regime for foreign cloud services

- UK: FCA/PRA guidance on outsourcing and data residency policies

Cloud-based finance platforms must meet multi-jurisdictional compliance baselines including GSTN approval, FTA recognition, ZATCA recognition, and HMRC recognition to operate across these markets.

Phase 4: Migration Execution and Data Integrity Validation

Data migration proceeds in stages, typically starting with non-critical workloads. Institutions use specialized transfer tools and platform-specific best practices to prevent data loss.

Post-migration validation is critical:

- Reconciling migrated data against source systems

- Running parallel operations to confirm accuracy

- Verifying that regulated processes — transaction reporting, audit logs, compliance workflows — are fully preserved

- Testing business continuity and disaster recovery procedures

Financial institutions cannot tolerate data discrepancies or process failures, making this the most operationally demanding phase of the entire program.

Phase 5: Optimization and Ongoing Governance

Go-live marks the start of cloud operations, not the finish line. Post-migration activities include:

- Cost optimization: Rightsizing compute resources and eliminating waste

- Performance tuning: Optimizing application response times and throughput

- Cloud governance: Establishing FinOps frameworks and security posture management

- Continuous compliance monitoring: Ensuring ongoing adherence to regulatory requirements

Most institutions establish a dedicated cloud center of excellence at this stage — a cross-functional team responsible for FinOps discipline, regulatory adherence, and continuous improvement across the cloud estate.

Key Challenges and Compliance Considerations in Financial Services Cloud Migration

Data Privacy and Sovereignty

Financial data is subject to strict residency rules in most jurisdictions. In India, the RBI mandates that all payment system data must be stored exclusively within the country. Similarly, the UAE's CBUAE requires that the master system of record containing all customer data be held within UAE borders. These requirements make public cloud adoption complex without region-specific data centres or private cloud configurations.

Regulatory Compliance Complexity

Financial institutions migrating to cloud must simultaneously satisfy prudential banking regulators, data protection authorities, tax authorities, and payment network rules. The core compliance frameworks include:

- ISO 27001 — information security management baseline

- SOC 1/SOC 2 — controls over financial reporting and data security

- PCI-DSS — payment card data protection standards

- Local prudential rules — RBI, CBUAE, FCA, and equivalent national regulators

Vendors that already hold these certifications — and carry regulatory recognition across multiple jurisdictions — reduce the compliance burden considerably, letting institutions focus on migration execution rather than baseline accreditation.

Legacy System Interdependency

Most large financial institutions operate core banking systems that are decades old, deeply customized, and tightly coupled with dependent systems. Core banking modernization projects typically take 3-5 years and cost large UK banks £250-330 million, with some exceeding £800 million — a scale that reflects the complexity facing large institutions globally.

Migration timelines extend because critical workloads — real-time payment processing, core ledger systems — cannot tolerate downtime. Lift-and-shift approaches are often impossible without extensive re-engineering.

Talent and Skills Gap

Cloud migration in financial services requires a rare combination of cloud engineering expertise, financial services domain knowledge, and regulatory understanding. 94% of core banking modernization projects exceed their timelines, with skills gaps being a primary factor.

That 94% figure reflects a consistent pattern: the capability gap is underestimated at project outset. Bridging it typically requires both targeted upskilling of internal teams and structured engagement with specialized implementation partners.

Risk Management Dimension

Cloud introduces new operational risk vectors that financial regulators increasingly scrutinize:

- Vendor concentration risk

- Third-party dependency

- Shared responsibility model misunderstandings

- Cyber exposure

Regulators in India, the UAE, and the UK now expect institutions to document these risks formally — mapping cloud dependencies, exit strategies, and incident response protocols before migration begins, not after.

Common Misconceptions and When to Choose Hybrid Over Full Cloud

Addressing Key Misconceptions

Misconception 1: Cloud migration is primarily about cost reduction Cloud has moved well beyond cost savings. The real competitive edge lies in faster time-to-market, enhanced customer experiences, and the agility to launch new products before competitors.

Misconception 2: The cloud provider is solely responsible for security Security is a shared responsibility. The provider secures the underlying infrastructure; your institution remains accountable for data protection, access controls, and application security. That line matters in every regulatory audit.

Misconception 3: Cloud migration is a one-time project It is a continuous capability-building process. Ongoing optimization, governance, and skills development do not stop at go-live — they define how much value you extract over time.

When Full Public Cloud Is Inappropriate

Full public cloud migration may be unnecessary or inappropriate when:

- Operating mission-critical, ultra-low-latency core banking systems

- Subject to strict data residency laws that no public cloud provider can fully satisfy

- The cost of re-engineering tightly coupled legacy workloads outweighs cloud benefits

- Recent significant on-premise investments have long depreciation cycles remaining

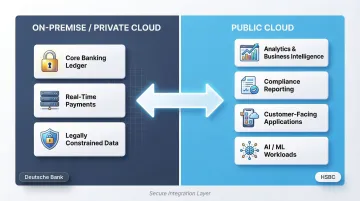

The Hybrid Cloud Alternative

Many financial institutions achieve optimal outcomes through hybrid models. Regulated, latency-sensitive, or legally constrained workloads stay on private cloud or on-premise, while analytics, reporting, compliance, customer-facing applications, and AI/ML workloads move to public cloud.

For complex financial institutions, hybrid is frequently the most pragmatic path — not a compromise, but a deliberate architecture choice. Deutsche Bank, Morgan Stanley, and HSBC have all publicly adopted hybrid models to balance agility with security and regulatory compliance.

Conclusion

Cloud migration in financial services is not simply an infrastructure upgrade — it's a compliance-driven, risk-managed process that sits at the intersection of technology strategy and regulatory obligation. Done right, it delivers real competitive advantage. Done carelessly, it creates exposure that no institution can afford.

The institutions that execute this well share a common approach: they treat cloud strategy as a business outcome decision, not an IT project. That means compliance mapping begins before architecture design, risk frameworks govern workload sequencing, and vendor selection accounts for regulatory familiarity — not just technical capability.

Whether you're moving to a full public cloud or building a hybrid model, the model matters less than the fit. The right migration strategy is the one aligned to your institution's actual regulatory obligations, legacy constraints, and growth priorities — not the one that sounds most progressive in a vendor pitch.

Frequently Asked Questions

Are banks moving away from cloud?

No—the opposite is true. Most banks are deepening cloud investments, not retreating. While some have repatriated specific workloads due to cost or latency reasons, the overall direction of the financial services industry is toward greater cloud adoption, particularly for analytics, compliance, and customer experience workloads.

Who are the big 4 cloud providers used in financial services?

AWS, Microsoft Azure, Google Cloud, and IBM Cloud are the dominant providers used by financial institutions. Each has built dedicated financial services cloud programs and compliance certifications to meet the industry's strict regulatory requirements.

What are the biggest challenges of cloud migration in financial services?

Three challenges consistently top the list: regulatory compliance and data sovereignty across multiple jurisdictions, legacy system complexity and interdependencies, and the shortage of professionals with both cloud and financial services expertise.

How long does cloud migration typically take for a financial institution?

Timelines vary significantly. A targeted migration of a single application or reporting system may take 3-6 months. Enterprise-wide transformation of core banking and compliance infrastructure typically spans 2-5 years, executed in multiple phased waves.

Is cloud migration safe for sensitive financial data?

Yes, when implemented correctly. Cloud environments can be highly secure — using encryption, role-based access controls, and compliance-certified infrastructure — and many meet or exceed the security controls of aging on-premise systems.

What is the difference between hybrid cloud and full cloud migration for financial institutions?

Full cloud migration moves all workloads to public cloud infrastructure. Hybrid cloud retains sensitive, latency-critical, or regulated workloads on private or on-premise infrastructure while using public cloud for analytics, compliance, and customer-facing applications. For large financial institutions, hybrid is the more common approach.