Introduction

Banks are running out of runway on manual operations. Compliance costs for US and Canadian financial institutions hit USD 61 billion annually in 2024, with 99% of institutions reporting year-on-year increases. At the same time, global banking revenue margins are projected to fall from 3.1% to 2.7% by 2030, according to McKinsey's Global Banking Annual Review—while banks already spend roughly USD 600 billion per year on technology globally.

Something has to give. For most banks, that something is the operational layer — and RPA is where the efficiency gains are most immediate.

Robotic Process Automation (RPA) deploys software bots that mimic human actions across digital interfaces, navigating core banking systems, CRMs, and ERPs to handle rule-based, repetitive tasks without touching underlying infrastructure. No system overhauls required, no migrations — bots work on top of what's already there.

This guide covers what banks need to know before committing: the highest-impact use cases, a phased implementation roadmap, and a vendor selection framework built specifically for regulated financial environments.

TL;DR: Key Takeaways

- RPA automates rule-based banking tasks, freeing staff for judgment-intensive work and cutting processing errors

- Top use cases: KYC/onboarding, loan processing, AML reporting, fraud monitoring, and back-office reconciliation

- Start with process assessment and a low-risk PoC — jumping straight to full deployment is the most common failure mode

- Evaluate vendors on BFSI domain expertise, security certifications, and integration depth before comparing licensing costs

- Establish pre-deployment baselines so ROI is measurable — it compounds as bots scale across additional processes

Why Banks Are Prioritising RPA Right Now

The global RPA market in BFSI was valued at USD 685.7 million in 2022 and is projected to reach USD 8.79 billion by 2030—driven by three pressures reshaping how banks operate:

Regulatory burden is accelerating. AML obligations, KYC requirements, and Basel compliance frameworks have pushed screening alert volumes up for over 83% of mid-to-large institutions. The cost of staying compliant manually is no longer sustainable.

Customer expectations have shifted. Fintechs have set the benchmark for instant onboarding and same-day decisions. Traditional banks competing on legacy processing timelines are losing the product comparison before the conversation even starts.

Margin compression leaves little room for inefficiency. McKinsey's analysis shows banks need to reduce cost per asset by 5% annually to maintain returns—against a historical reduction rate of just 1%. RPA is one of the few tools that can close that gap at scale.

Modern RPA vs. Older Automation Methods

Traditional macros and hardcoded scripts operate within a single system and break the moment the interface changes. Modern RPA bots navigate multiple systems simultaneously—core banking platforms, ERP, CRM—handle exceptions through defined escalation rules, and integrate with AI/ML layers for intelligent document processing and pattern recognition.

Early movers have a structural head start. Banks that have already built RPA infrastructure are accumulating process templates, governance frameworks, and institutional knowledge that late adopters will take years to replicate.

High-Impact RPA Use Cases in Banking

Not every banking process is a good automation candidate. Prioritize workflows that are high-volume, strictly rule-based, time-sensitive, and currently generating errors or backlogs.

Customer Onboarding and KYC

RPA bots extract data from submitted identity documents, validate against regulatory databases, cross-check watchlists, and populate customer records—all without human intervention for standard cases. State Street Bank's Blue Prism implementation achieved 49% faster movement from account opening to trading, returning over 187,500 workdays over four years.

Indonesia's Bank Mega saw customer verification drop from 3–4 hours to under 5 minutes after automating KYC checks—a 98% increase in processing speed.

Loan and Credit Processing

Bots handle document collection, credit score retrieval, eligibility checks, and borrower status notifications. A top-25 US commercial bank using Automation Anywhere reported 100% error elimination and a 2.6-day reduction in mortgage cycle time, with appraisals completed 6.3 days faster.

For NBFC clients, Cygnet.One's automation work has delivered up to 80% reduction in loan processing turnaround time. A leading Indian NBFC spanning microfinance, agri-finance, and MSME lending also saw a 95% reduction in report processing time.

Regulatory Compliance and AML Reporting

RPA handles transaction monitoring against defined rule sets, flags anomalies for AML review queues, and auto-generates regulatory submissions on schedule. DNB Bank automated 500,000 customer accounts to meet a government compliance deadline and eliminated AML errors entirely—part of a broader programme that saved €70 million and returned 1.5 million hours across 230 automated processes.

Scheduled compliance workflows eliminate the risk of missed deadlines and inaccurate submissions—and the same pattern-monitoring logic that catches regulatory anomalies applies directly to fraud prevention.

Fraud Detection and Transaction Monitoring

Bots continuously scan transaction patterns against predefined rule sets and trigger instant alerts for investigation teams. Speed matters, but consistency matters more. Human reviewers fatigue; bots don't miss the 3 AM transaction.

Cygnet.One's hyperautomation practice includes AI-powered transaction monitoring that flags unusual activity for fraud prevention, embedded directly into banking client environments.

Back-Office Reconciliation and Ledger Management

Bank Mega reduced reconciliation processing from up to 6 hours to near-instantaneous after automation. Riyad Capital saved over 20,000 working hours annually with a 66% reduction in processing time per reconciliation item.

For banks still running daily cash positioning and general ledger updates through manual spreadsheet workflows, this is often the fastest ROI available: low complexity, high frequency, and straightforward to measure.

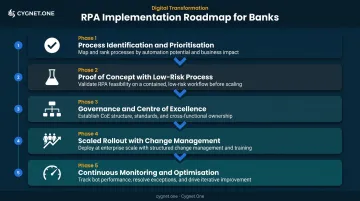

Step-by-Step RPA Implementation Roadmap for Banks

Banks that skip structured rollout phases typically find their bots breaking within six months — when a system upgrade or regulatory change hits a workflow nobody was monitoring. A phased approach with defined checkpoints prevents that outcome.

Phase 1 – Process Identification and Prioritisation

Build a process inventory first. Map every manual workflow, then score each against four criteria:

- Volume – How many transactions or instances per day/month?

- Frequency – Is this daily, weekly, or event-triggered?

- Rule-based consistency – Are decisions always deterministic, or do they require judgment?

- Current error rate – Is this process generating rework, backlogs, or compliance issues?

Processes scoring high across all four are your first candidates. Processes requiring interpretation, exception-heavy judgment, or unstructured inputs should stay off the initial list.

Phase 2 – Proof of Concept with a Low-Risk Process

Start with an internal, non-customer-facing process. Regulatory report generation, daily reconciliation, or ledger update workflows are ideal PoC candidates — they're high-frequency, measurable, and contained.

The goal isn't just to prove the technology works. It's to validate ROI assumptions with real data and build internal credibility before automating anything customer-facing. Forrester's Total Economic Impact research on RPA in financial services shows a typical progression from 4 initial workflows to 15 processes in year one, reaching 120 automated processes by year three. That trajectory depends entirely on whether the PoC produced credible, measurable results first.

Phase 3 – Governance and Centre of Excellence (CoE)

Once the PoC delivers validated results, governance becomes the critical next step — and the most commonly under-resourced one. An RPA CoE fails when IT owns it alone. Banking RPA governance requires joint business and IT ownership, with the business unit accountable for process outcomes and IT accountable for bot stability and system integration.

The CoE should monitor:

- Bot performance and exception rates

- Upstream/downstream system changes that could break workflows

- Regulatory updates that affect automated compliance processes

- Expansion pipeline for new process candidates

Without this structure, bots become orphaned after the initial deployment. They run unmonitored until a silent failure surfaces as a compliance gap or a reconciliation error that nobody catches in time.

Phase 4 – Scaled Rollout with Change Management

With governance in place, scaled rollout can begin — but the human dimension is where most programmes stall. Staff need to understand that RPA targets task relief, not headcount elimination. Practically, this means:

- Train non-technical staff to manage bot exceptions and flag workflow breaks

- Communicate early and repeatedly — ambiguity creates resistance

- Assign internal RPA champions who can sustain adoption after the vendor engagement ends

- Connect reskilling to concrete new responsibilities, not abstract promises about "higher-value work" with no defined path

Phase 5 – Continuous Monitoring and Optimisation

A deployed bot is a maintained asset, not a completed project. Regulatory changes, system upgrades, and process redesigns all create breaking conditions. Establish a regular review cadence — quarterly at minimum — and define exception escalation protocols before they're needed.

How to Select the Right RPA Vendor for Your Bank

RPA tools that perform well in manufacturing or retail are not automatically suited to banking. The security, compliance, and integration requirements of regulated financial environments narrow the field considerably. Approach vendor selection with the same rigor you would apply to any core infrastructure decision.

BFSI Domain Expertise and References

A vendor with genuine banking experience brings pre-built process templates, awareness of regulatory constraints, and case studies from comparable institutions. Generic enterprise RPA experience is not equivalent.

Request references from banks of comparable size, geography, and regulatory environment. Ask specifically how the vendor handled compliance workflow changes mid-deployment—that is where domain gaps become apparent.

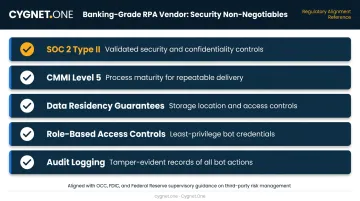

Security Certifications and Data Compliance

Non-negotiables for banking-grade RPA:

- SOC 2 Type II – Validated controls over security, availability, and confidentiality

- CMMI Level 5 – Process maturity for consistent, repeatable delivery

- Data residency guarantees – Where is your data stored, and who can access it?

- Role-based access controls – Can you restrict bot credentials to minimum necessary permissions?

- Audit logging – Complete, tamper-evident records of every bot action

Per OCC, FDIC, and Federal Reserve guidance, banks remain fully responsible for third-party vendor actions—using an RPA vendor does not transfer regulatory accountability. Regulators explicitly list SOC reports and independent assessments in their third-party due diligence requirements.

Cygnet.One holds both CMMI Level 5 and SOC 2 Type II certification, providing the compliance assurance baseline that banking clients require for sensitive financial data environments.

Integration Capability with Core Banking Systems

The vendor must demonstrate integration with your existing stack without requiring expensive backend overhauls. Cygnet.One's automation practice supports integration across SAP, Oracle, Microsoft Dynamics, Salesforce, and GSTN/MCA APIs—operating at both API level and UI level depending on what the target system supports.

Ask vendors to demonstrate:

- Native connectivity to your core banking platform

- Handling of legacy systems where API access isn't available (UI-level bot navigation)

- Attended vs. unattended bot support depending on your workflow requirements

Scalability, Uptime SLAs, and Support Model

Bots running month-end reconciliation or regulatory filing workflows cannot go down at deadline. Evaluate:

- Infrastructure capacity to scale during peak periods

- Guaranteed uptime SLAs (not aspirational targets)

- 24/7 support with severity-graded escalation paths—not just a ticketing queue

Cygnet.One's managed services infrastructure maintains 99% uptime in banking modernization deployments, with automated escalation workflows graded by severity and routed through real-time alerting systems.

Total Cost of Ownership vs. Sticker Price

Licensing cost is rarely the largest line item in an RPA program. Factor in:

| Cost Component | What to Evaluate |

|---|---|

| Implementation effort | Days to configure, test, and deploy per process |

| Bot licensing | Per-process or per-bot pricing at scale |

| Maintenance overhead | Who handles bot breaks when upstream systems change? |

| Internal training | How long to make business teams self-sufficient? |

| Vendor support model | Is ongoing optimization included or billable separately? |

The cheapest vendor at contract signing frequently carries the highest total cost by year two.

Measuring RPA ROI in Banking

Establish baselines before deployment—not after. Without pre-automation benchmarks, ROI claims are unverifiable and executive buy-in erodes when questioned.

Track these metrics:

- Processing time per transaction (before and after)

- Error rate and rework volume

- FTE hours reallocated to non-automatable tasks

- Compliance incidents and deadline adherence

Frame ROI for executive stakeholders by connecting automation metrics to business outcomes: faster loan disbursement improves net promoter scores and revenue velocity; fewer AML errors reduce penalty exposure. The efficiency number matters less to leadership than the business risk or revenue impact it represents.

Forrester's 2024 TEI study for a composite financial services organization modelled 330% ROI with a payback period under six months and $53.4 million in net present value. The study also noted 7.5% improvement in staff retention—a measurable business outcome that traditional ROI models routinely overlook, and a real differentiator in a tight hiring market.

Those numbers also grow over time. A reconciliation bot built for one business unit can be adapted for three more at minimal incremental cost—compounding returns well beyond the initial deployment.

Common RPA Implementation Pitfalls in Banking

Most RPA programs in banking don't fail because the technology doesn't work — they fail because of avoidable execution mistakes. Three pitfalls account for the majority of underperforming implementations.

Automating a Broken Process

RPA makes bad processes faster, not better. If the underlying workflow carries redundant approval steps, unclear data ownership, or inconsistent inputs, bots will faithfully replicate every flaw at scale. Redesign the process before you automate it — not after.

Treating RPA as an IT-Only Project

When IT selects bot candidates without business participation, the team optimizes for technical ease rather than business impact. The result is low-ROI implementations that solve problems nobody prioritized. Forrester explicitly identifies the siloed IT-driven approach as a documented pitfall in financial services RPA programs.

Underestimating Change Management

Employee resistance — often rooted in job security concerns — is the leading cause of RPA program failure, according to SSON research. Proactive communication, visible leadership sponsorship, and concrete reskilling pathways are non-negotiable. Forrester's composite financial services model budgeted $4.3 million for change management and training alone, with retraining timelines ranging from 2 to 20 days depending on role complexity.

Frequently Asked Questions

What is RPA in banking and how is it different from traditional automation?

RPA uses software bots to mimic human actions across existing system interfaces—no backend coding or API development required for most workflows. Traditional automation requires system-level integration built specifically for each workflow, making it expensive and inflexible when processes or systems change.

Which banking processes are the best candidates for RPA?

High-volume, rule-based processes with clear inputs and outputs: KYC verification, loan document collection and status updates, AML transaction monitoring, daily reconciliation, and regulatory report generation. Processes requiring human judgment or unstructured data interpretation are poor candidates for standard RPA.

How long does RPA implementation typically take in a bank?

A PoC for a single contained process typically takes 6–12 weeks. Enterprise-wide scaled deployment spans 6–18 months, depending on process complexity, governance readiness, change management maturity, and vendor support quality.

What security certifications should I require from an RPA vendor for banking?

At minimum: SOC 2 Type II, CMMI Level 5, data residency controls, role-based access with least-privilege enforcement, and complete audit logging of all bot activity. These align with OCC/Fed/FDIC third-party due diligence requirements for technology risk governance.

How do I build the business case for RPA to present to bank leadership?

Quantify the cost of current manual processes—FTE hours multiplied by volume and error rate—then project automation savings with a phased cost-benefit analysis. Present RPA as a long-term strategic investment with compounding returns, and tie efficiency gains directly to revenue or risk outcomes leadership already tracks.

Can RPA work alongside legacy core banking systems without full integration?

Yes. RPA bots operate at the UI layer, interacting with legacy systems exactly as a human user would. No backend API or deep integration is required for most use cases, which is why RPA works in environments where system-level integration would be cost-prohibitive.