Introduction

Financial institutions process millions of transactions daily — UPI alone handled over 22.6 billion transactions worth ₹29,52,542 crore in March 2026, across 705 live banks. Traditional automation cannot keep pace with this volume. Rules-based RPA breaks when inputs change, periodic compliance reviews miss real-time violations, and manual credit assessments create bottlenecks that cost lenders deals.

AI agents close that gap. Unlike static automation, they perceive financial data from multiple sources, reason through variables, and act without waiting for human triggers: flagging fraud, scoring a loan, generating a compliance report — in real time.

What follows is a practical breakdown for banking, lending, and compliance leaders — covering how these agents work, where they deliver the most measurable impact in BFSI, and what to look for when evaluating vendors.

Key Takeaways

- AI agents go beyond RPA — they reason through context, act autonomously, and learn from outcomes across financial workflows

- Key use cases: credit risk scoring, fraud detection, compliance monitoring, cash flow forecasting, and customer support

- Vendor choice depends on your data environment, compliance needs, and use case scope, ranging from ERP-embedded platforms to specialized BFSI solutions

- Indian NBFCs and digital lenders have a particularly strong case for AI agents in credit underwriting and invoice financing

- Start small, fix your data foundation first, and build human oversight into every high-stakes decision

What Are AI Agents in Financial Services?

An AI agent is autonomous, goal-directed software that perceives data from multiple sources — ERPs, transaction systems, regulatory feeds, scanned documents — reasons through it, and takes action without requiring a human to trigger each step.

IBM defines AI agents as systems that autonomously perform tasks by designing workflows with available tools. The BIS goes further, describing them as LLM-based systems with planning capabilities, long-term memory, and access to external tools — including the ability to execute code or interact with market systems.

How They Differ from Traditional Automation

RPA bots follow rigid scripts. When a field changes format, an invoice arrives in an unexpected layout, or a regulation updates — the bot breaks. A chatbot stops at answering the question. An AI agent pulls live data, initiates the next step, and escalates when something needs human judgment.

The distinction matters in finance because:

- RPA requires exact, predictable inputs and produces scripted outputs

- AI agents interpret context, handle exceptions, and adapt when conditions shift

- Chatbots respond to queries but stop there — they hold no state, take no follow-on action, and can't initiate requests

Why the Market Is Moving Now

The AI agents in financial services market is projected to grow from USD 691.3 million in 2025 to USD 6.708 billion by 2033. A Gartner survey of 301 CFOs found that 77% planned to increase technology budgets in 2025, framing AI as a finance operating-model investment with measurable returns — not a speculative IT initiative.

How Do AI Agents Work in Finance?

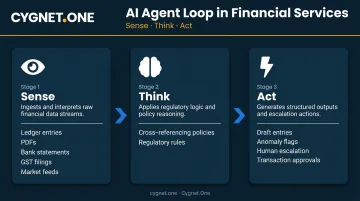

AI agents in regulated financial environments operate on a three-part loop:

Sense → Think → Act

1. Sense — the agent ingests structured and unstructured data: ledger entries, PDFs, bank statements, GST filings, market feeds, emails

2. Think — it reasons over that data, cross-references internal policies or regulatory rules, and determines the appropriate action

3. Act — it executes within pre-defined secure boundaries: creating a draft entry, flagging an anomaly, routing a case for human review, or approving a low-risk transaction

The Technology Stack Underneath

Three core technologies work together underneath:

- Machine learning for pattern recognition in transaction data, repayment behavior, and fraud signals

- Natural language processing for reading unstructured documents — loan applications, audit reports, customer emails

- Fine-tuned large language models for contextual reasoning across financial regulations, internal policies, and domain-specific data

Why the Audit Layer Is Non-Negotiable

In regulated environments, every agent action must meet three requirements:

- Timestamped — a complete chronological record of what the agent did and when

- Documented — structured logs that survive regulatory examination

- Explainable — human-readable reasoning, not opaque model outputs

This matters most in credit decisions. The CFPB is clear: model complexity doesn't excuse vague outcomes. Creditors must provide specific adverse-action reasons regardless of how the underlying algorithm works.

For high-stakes decisions, governed AI agents use an escalation trigger — a confidence threshold below which the agent routes the case to a human reviewer rather than acting on its own. That threshold is what separates governed automation from unchecked automation.

Key Use Cases of AI Agents in Financial Services

The strongest BFSI use cases share three traits: repetitive workflows, multi-variable decision-making, and serious financial consequences when errors occur. These conditions make finance one of the highest-impact sectors for agentic AI.

Credit Risk Assessment and Loan Underwriting

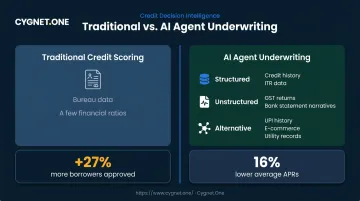

Legacy credit scoring models rely on bureau data and a handful of financial ratios. AI agents evaluate creditworthiness across a far broader data landscape simultaneously:

- Structured inputs: credit history, financial statements, repayment records, ITR data

- Unstructured inputs: GST return patterns, e-invoice flows, bank statement narratives, e-way bill volumes

- Alternative data: UPI transaction history, e-commerce performance, utility records, MSME registration data

The CFPB documented an AI underwriting model that approved 27% more borrowers than a traditional model, with 16% lower average APRs for approved loans. BIS research found that combining ML techniques with non-traditional data improved default prediction by 5.3 percentage points in AUROC over traditional models.

For NBFCs and digital lenders, this matters immediately. Cygnet.One's credit assessment platform ingests GST filings, bank statements (in any format including scanned documents via AI-OCR), ITR data, MCA records, and UPI transaction history to generate risk-optimized credit decisions. One of India's leading NBFCs reduced report processing time by over 95% after deploying the platform — ageing analysis reports that previously took 4–5 days were generated in seconds.

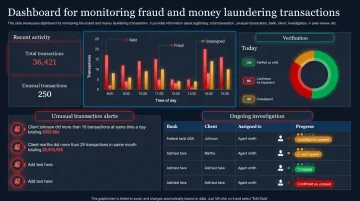

Fraud Detection and Transaction Monitoring

Static rule thresholds catch known fraud patterns. They miss the novel ones. RBI reported 36,075 fraud cases involving ₹36,014 crore in 2024–25 — a figure that underscores how inadequate rules-based monitoring has become at scale.

AI agents monitor transactions continuously, detecting anomalies based on:

- Behavioural patterns unique to each account

- Network relationships between parties

- Contextual signals — transaction size, time, location relative to historical norms

BIS Project Aurora found that ML models detected more than twice as many money launderers as siloed rule-based systems in a proof-of-concept, with an 80% reduction in false positives in collaborative scenarios.

Once flagged, the agent logs the evidence trail, escalates to compliance teams, and documents the decision rationale. Investigations that previously took hours of manual review are resolved within the same automated cycle.

Regulatory Compliance and Audit Trail Generation

Financial crime compliance costs reached USD 274 billion globally in 2022, up 28% from USD 214 billion in 2020. Much of that cost comes from manual review cycles and point-in-time audit preparation.

AI agents shift this from periodic to continuous:

- Cross-verify every transaction or invoice entry against RBI guidelines, GST rules, or applicable regulatory standards in real time

- Flag inconsistencies before they become violations

- Generate timestamped, human-readable audit logs for every action taken

For Indian BFSI institutions, SEBI requires market intermediaries to report AI and ML applications in use — meaning the agent's own decision log becomes part of the compliance posture, not just an operational record.

Cash Flow Forecasting and Treasury Management

Static monthly forecasting built on spreadsheet models cannot reflect a business reality that changes daily. AI agents process live data from ERP systems, payment platforms, and bank feeds to model cash flow scenarios continuously.

In practice, treasury teams gain real-time liquidity visibility — with agents that can flag shortfalls, model funding scenarios, and update forecasts as transactions clear. Gartner found that 66% of finance leaders believe GenAI will have the most immediate impact on explaining forecast and budget variances. Deloitte's 2024 global treasury survey identified cash flow forecasting, cash positioning, and market-risk management as the most popular treasury AI use cases.

Specific areas where agents add measurable value:

- Automated daily cash positioning across accounts and currencies

- Scenario modeling for payment timing and working capital optimization

- Early-warning alerts when liquidity falls below defined thresholds

- Variance explanations tied directly to transaction-level data

Customer Service and 24/7 Financial Support

AI support agents in financial services connect directly to live systems and take action — not just retrieve information. A capable agent can:

- Pull live account data to answer balance or transaction questions

- Guide customers through onboarding steps with context awareness

- Initiate service requests or escalations based on what they find

- Hand off to human representatives when complexity exceeds defined thresholds

The functional difference from a chatbot is system access: chatbots surface static responses, while AI support agents query live financial data and trigger downstream workflows. For financial institutions managing high inbound volumes — especially NBFCs handling MSME borrower queries — this reduces service costs while maintaining response quality.

Key Benefits of AI Agents for BFSI and Lending Institutions

Speed and Scale Without Proportional Headcount

AI agents process transactions, applications, and compliance checks at volumes no manual team can match. Accenture estimates that 73% of time spent by US bank employees has high potential to be impacted by GenAI — 39% through automation and 34% through augmentation. McKinsey puts the annual value pool for GenAI in banking at USD 200–340 billion.

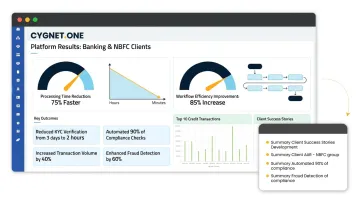

For Indian lenders specifically, Cygnet.One's implementations have delivered:

- 95% reduction in report processing time for a leading NBFC

- 80% faster decision-making for a private bank's GST reconciliation workflows

- 350 man-hours saved for indirect tax return filing automation at a banking client

Accuracy and Audit Readiness

AI agents apply identical logic to every transaction, every time — no fatigue, no end-of-quarter shortcuts. Every action is logged with rationale, which makes regulatory reviews faster and less disruptive for compliance teams.

Strategic Capacity for Finance Teams

When agents handle GL coding, credit document verification, compliance flagging, and invoice reconciliation, finance teams shift from reactive data processors to strategic decision partners. That capacity shift plays out across every role:

- Relationship managers focus on client strategy instead of data assembly

- Credit officers engage on complex cases rather than routine document checks

- Risk teams govern the model rather than run the reports

Vendor Guide: Choosing the Right AI Agent Platform for Financial Services

The vendor market divides into three broad categories:

| Category | Examples | Best For |

|---|---|---|

| ERP-embedded platforms | SAP Joule, Oracle, Workday | Enterprises already on these ERP stacks |

| Specialist finance automation | HighRadius, BlackLine, Tipalti | AP, AR, and financial close automation |

| Domain-specific BFSI platforms | Cygnet.One, Hebbia, Salesforce Financial Services Cloud | Regulated lending, compliance, and credit workflows |

The right fit depends on your workflow scope, data environment, and compliance mandates — criteria covered in detail below.

Key Evaluation Criteria

Accuracy and auditability Prioritize platforms with source-linked outputs and immutable audit logs. Can the agent explain its decision in plain language? For credit decisions and fraud investigations, explainability is a regulatory requirement, not an optional feature.

Integration depth Siloed agents that can't access cross-system data deliver partial value. Assess pre-built connectors for your ERP, core banking system, CRM, and regulatory feeds. Cygnet.One supports integration with SAP, Oracle, Microsoft Dynamics, Tally, Finacle, and BANCS, with 100+ ERP integrations documented globally.

Compliance and security posture In regulated environments, verify:

- SOC 2 Type II or equivalent certification

- ISO 27001 for information security management

- Role-based access controls and data residency options

- For India deployments: alignment with RBI IT Governance Master Direction, GSTN rules, and SEBI AI/ML reporting requirements

- For Middle East deployments: ZATCA, FTA, and applicable local mandates

Customization vs. deployment speed Pre-built agents deploy faster but may not accommodate your firm's proprietary underwriting models or risk thresholds. Evaluate whether the platform supports configuration through rule engines or low-code tools — or requires a full professional services engagement for every change.

For Indian and Middle East BFSI institutions specifically, Cygnet.One offers a purpose-built option. With SOC 2 Type II compliance, ISO 27001:2022 certification, and deep ERP integration experience, it is built for the compliance-heavy requirements of Indian lending and invoice financing. The platform already processes 15–19% of India's e-invoices.

Its BridgeCash platform draws on real-time GST and e-invoice data — sourced directly from its IRP and GSP position — to power automated credit assessment for NBFCs and lenders serving MSME clients.

Implementing AI Agents in Your Financial Institution

Start with One Bounded Use Case

Don't build an enterprise-wide agent strategy before validating a single deployment. Identify a workflow that is:

- Repetitive and data-rich

- Currently creating measurable delays or errors

- One where the consequences of mistakes are financially clear

Invoice processing, credit document verification, and compliance flagging are strong starting points. Pilot one agent in a controlled environment and measure against pre-defined success metrics before scaling.

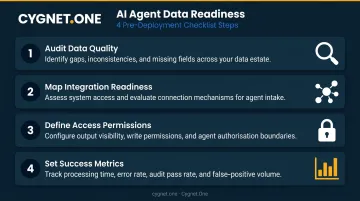

Fix the Data Foundation First

AI agents perform at the level of the data they ingest. Before deployment:

- Audit data quality across your core systems — gaps, inconsistencies, and missing fields will propagate into agent outputs

- Map integration readiness — which systems can the agent access, and through what mechanisms?

- Define access permissions — who can see agent outputs, and which systems can an agent write to?

- Set success metrics upfront — processing time, error rate, audit pass rate, false-positive volume

Govern from Day One

For high-stakes decisions — credit approvals, regulatory filings, fraud escalations — human oversight is non-negotiable. Build the governance framework before go-live, not after:

- Define confidence thresholds below which agents escalate to human reviewers

- Establish escalation protocols and review ownership

- Schedule periodic audits of agent outputs against expected behavior

- Maintain a model inventory with version tracking and performance monitoring

This governance structure directly affects your regulatory standing. The FSB has flagged AI-related vulnerabilities — including third-party dependencies, model correlation risks, and governance gaps — as active concerns for financial regulators. Institutions that document their controls, version their models, and assign clear oversight ownership tend to resolve regulatory inquiries faster and recover more predictably when a model produces unexpected outputs.

Frequently Asked Questions

What are AI agents in finance?

AI agents in finance are autonomous software systems that perceive financial data from multiple sources, reason through it using machine learning and NLP, and take goal-directed actions — processing invoices, flagging fraud, or scoring credit risk — with minimal human input and full audit traceability.

Which AI agent is best for finance?

The right platform depends on institution type and use case. Large enterprises may prefer embedded ERP options like SAP Joule or Workday, while BFSI institutions and NBFCs with lending and compliance requirements are better served by specialized platforms built for regulated environments, such as Cygnet.One for Indian and Middle East markets.

What is an AI support agent?

An AI support agent is a customer-facing or internal assistant that answers financial queries, guides users through processes, and takes action — flagging issues or initiating service requests — by integrating with live financial systems. Unlike a chatbot, it executes decisions rather than just delivering responses.

How do AI agents differ from RPA in financial services?

RPA bots follow fixed rules and break when inputs change. AI agents interpret context, handle exceptions, and improve over time — making them suitable for complex financial workflows that require judgment rather than simple rule execution.

What compliance and security standards should AI agents in banking meet?

AI agents in banking should meet SOC 2 Type II or equivalent standards, maintain ISO 27001 certification, support role-based access controls, and keep full audit logs of every decision. Indian deployments must also align with RBI IT Governance Master Direction, GSTN rules, and SEBI AI/ML reporting requirements.

How long does it take to implement AI agents in a financial institution?

Focused pilots for a single use case — invoice processing or credit flagging — can go live in weeks. Enterprise-wide deployments with ERP integrations typically take 3–6 months. Measurable ROI is often visible within the first deployment cycle when success metrics are defined upfront.