Introduction

Banks, NBFCs, and insurers struggle with the same operational bottleneck: enormous document volumes — loan applications, KYC packets, bank statements, compliance filings, invoices — most of which still depend on manual handling. India's CKYCR registry held over 82 crore individual KYC records as of December 2023. The government sanctioned 6.67 crore loans under PMMY in FY 2023-24 alone. Each record, each application, reviewed by hand.

The result is predictable: slower turnaround, compliance gaps, and skilled staff spending hours on data entry instead of credit or risk decisions.

This guide answers three questions for finance and operations leaders evaluating IDP:

- What IDP actually does — and what it doesn't

- Where it delivers the strongest ROI in financial workflows

- What separates a capable vendor from one that will struggle with your real document mix

Key Takeaways

- IDP uses AI, ML, and NLP to classify, extract, validate, and route financial documents — far exceeding basic OCR capabilities

- Highest-ROI use cases: loan origination, KYC/AML compliance, invoice processing, and client onboarding

- Prioritize vendors with strong accuracy on unstructured documents, SOC 2 Type II certification, and deep ERP/core banking integration

- Red flags: template-only extraction, no audit trails, and vendors who can't show live financial services deployments

- Well-implemented IDP cuts document processing times by 60–80%, with measurable cost savings at scale

What Is IDP — and Why Financial Services Can't Ignore It

IDP Defined

Intelligent Document Processing is an AI-powered pipeline that ingests documents in any format (structured forms, semi-structured invoices, unstructured contracts), classifies them, extracts relevant data, validates it against business rules, and routes it into downstream workflows.

That's meaningfully different from the two technologies it's often confused with:

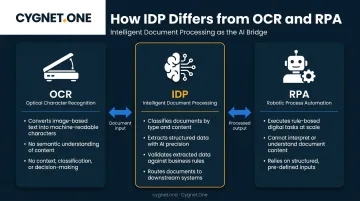

- OCR converts image-based text into machine-readable characters but has no understanding of context or document type

- RPA automates repetitive task execution but cannot interpret document content on its own

IDP is the layer between them : the intelligence that reads and understands a document before handing structured data to RPA bots or core banking systems for action.

A Market That's Growing Fast

The global IDP market sits at USD 3.22 billion in 2025 and is forecast to reach USD 43.92 billion by 2034 at a 33.68% CAGR. BFSI accounted for 40% of market share in 2024 — the largest vertical by a significant margin.

That dominance makes sense: financial services firms deal with regulatory filings, audit trails, KYC documentation, loan paperwork, and invoices at a scale and complexity that most other industries don't approach.

The GenAI Inflection Point

That market growth is being accelerated by a fundamental shift in how IDP works. Traditional systems required extensive template configuration for each document layout — a new vendor invoice format meant manual reconfiguration. Modern LLM-enhanced IDP eliminates this constraint, supporting zero-shot extraction (no training examples needed, just a schema definition) or few-shot learning with as few as 5–10 sample documents.

For mid-sized NBFCs and insurers, this matters. It means onboarding new document types in days rather than months, and deploying IDP across varied document mixes without building custom templates for every supplier, regulator, or branch format.

Some platforms now use Vision Language Model (VLM)-based extraction, which interprets layout, tables, and handwritten annotations together — rather than treating each as a separate parsing problem.

High-Impact IDP Use Cases in Financial Services

Loan Origination

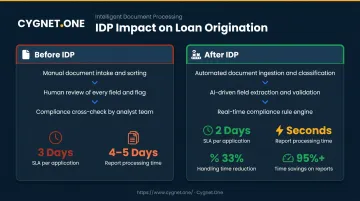

Loan processing involves a dense document mix: income proofs, ITR filings, bank statements, identity documents, and collateral paperwork. IDP automatically ingests these, classifies each document type, extracts relevant fields, and cross-validates them — then flags discrepancies before the file ever reaches a credit officer.

The results are measurable. An IndusInd Bank IDP deployment reported a 33% reduction in average document handling time, with SLAs compressed from 3 days to 2 days. Cygnet.One's NBFC clients have seen report processing times cut by over 95% — from 4–5 days to seconds — through automation of loan tracking and portfolio management workflows.

For India-scale lenders processing millions of applications annually, that kind of compression has direct revenue implications: faster decisions mean faster disbursements.

KYC and AML Compliance

KYC document verification — passports, utility bills, Aadhaar, PAN, address proofs — is repetitive, high-volume, and regulatory-critical. It's also expensive. A 2016 Thomson Reuters survey found banks spent an average of USD 60 million annually on KYC compliance.

The efficiency case for IDP is concrete. McKinsey research shows that straight-through processing for 50–65% of files cuts low-risk KYC review time from 100 minutes to 30 minutes. Across the board, automation trims KYC workloads by 20–30% and improves quality by 15–40%.

Cost data from India tells the same story:

- Traditional KYC runs approximately ₹1,000 per check (CERSAI data)

- Entities using CKYCRR APIs have brought that cost down to roughly ₹1.25

- IDP is the processing layer that makes API-driven automation viable at scale

Invoice Processing and Accounts Payable

IDP extracts vendor data, invoice amounts, GST fields, and tax line items, then matches invoices to purchase orders automatically. This eliminates the manual verification loops that slow AP teams and create reconciliation errors.

Cygnet.One's platform delivered a 60–70% reduction in MIRO (Goods Receipt + Invoice Verification) processing time for a global enterprise client, measured against fully manual baseline processing through SAP. The automation replaced manual PO–GRN–invoice validation with RPA bots integrated with an OCR/AI engine.

For Indian businesses, this connects directly to e-invoicing compliance. India's GST e-invoice mandate covers businesses with turnover above ₹5 crore, requiring IRP-assigned IRNs for every B2B invoice. Cygnet.One operates as a GSTN-approved IRP and GSP, having processed over 412 million e-invoices — making compliance automation and invoice processing effectively the same workflow.

In Saudi Arabia, ZATCA's Phase 2 e-invoicing requirements (clearance, XML/PDF-A3 format, cryptographic stamps) similarly make IDP a compliance necessity for businesses operating in the Kingdom.

Client Onboarding

Multi-page onboarding packets in wealth management and insurance involve varied document types: identity proofs, financial disclosures, risk questionnaires, and policy documents. Manual processing creates delays that cost firms clients before relationships even begin.

Deloitte research indicates that automating KYC-related steps can reduce processing times by up to 60%, with firms targeting 30–50% reductions in overall onboarding timelines. Cygnet.One's BridgeFlow platform delivers automated digital onboarding with real-time validations — one implementation achieved a 50% improvement in onboarding process time.

Regulatory and Compliance Reporting

RBI, SEBI, and IRDAI in India, alongside ZATCA and FTA mandates across the Middle East, each demand accurate, timestamped, auditable documentation. IDP automates extraction for filings, suspicious activity reports, and audit trails — directly reducing the human error risk that regulatory reviews target.

India's Account Aggregator framework has already enabled 221 crore+ successful financial data-sharing transactions, pointing to the infrastructure scale at which compliance automation now needs to operate.

Core Capabilities to Look for in an IDP Solution

When evaluating vendors, five capabilities separate serious platforms from those that will struggle with your actual document environment.

1. Extraction across all document types

Your vendor must handle structured forms, semi-structured invoices and bank statements, and unstructured contracts and correspondence. Your vendor must handle structured forms, semi-structured invoices and bank statements, and unstructured contracts and correspondence. Clean digital PDFs are the easy case — most platforms handle those. Ask specifically for accuracy benchmarks on semi-structured and unstructured documents from actual financial services deployments, not controlled demos.

2. AI-powered classification and validation

The system should classify incoming document types automatically and validate extracted data against business rules — for example, checking that a PAN number matches Aadhaar, or that an invoice amount reconciles with a PO. Look for built-in confidence scoring so low-confidence extractions are flagged for human review rather than passed through silently.

3. Compliance and security infrastructure

Financial services deployments require:

- SOC 2 Type II compliance (Cygnet.One achieved this in 2024, with additional ISO 27001:2022 and SOC 1 certifications)

- Encrypted storage and data handling at rest and in transit

- Role-based access controls

- Full audit logging of every extraction, decision, and model version used

- Regulatory recognition in your operating geographies (GSTN, ZATCA, FTA)

4. Integration depth

Ask vendors for certified integration lists and evidence from live deployments — not just a compatibility matrix. Cygnet.One's platform supports SAP, Oracle, Microsoft Dynamics, Tally, Finacle, and BANCS, with 100+ ERP integrations in production. Implementation risk drops significantly when your specific ERP combination has already been proven in the field.

5. Scalability and STP rates

Straight-through processing — the percentage of documents processed with zero human intervention — is your headline efficiency metric. According to Ardent Partners' 2024 AP benchmarking research, Best-in-Class AP teams achieve 69% STP adoption, 78% lower per-invoice costs, and 82% faster cycle times. Ask vendors for their STP rates on semi-structured documents, and verify that they can scale through quarter-end or tax-season volume spikes.

How to Evaluate and Select an IDP Vendor

Start With Your Document Universe

Before shortlisting vendors, catalogue what you actually process: document types, formats, volumes, languages, and downstream systems. Many vendors optimise for clean digital PDFs. Financial services firms deal with scanned paper, handwritten fields, and multi-language documents. Your vendor evaluation must test against your real document mix.

Use a Structured Scorecard

Evaluate every vendor across five dimensions:

| Dimension | What to Assess |

|---|---|

| Accuracy | Benchmarks on your specific document types |

| Compliance | SOC 2, regulatory recognition in your geographies |

| Integration | Certified ERP/core banking connections, live deployments |

| Scalability | Peak volume handling, documented STP rates |

| Track record | Verifiable financial services case studies |

Ask the Right Questions in Vendor Demos

Don't let vendors control the narrative with showcase documents. Bring your own and ask:

- "What is your STP rate on semi-structured documents?"

- "How do you handle documents in regional languages?"

- "Can you show audit logs from a live financial services deployment?"

- "What is your model retraining process when extraction accuracy drops?"

- "Do you have compliance recognition in our operating geographies?"

- "What happens when the system encounters a document format it hasn't seen before?"

Evaluate Total Cost of Ownership

Licensing fees are the visible part of the cost. What matters is TCO across:

- Implementation and integration labor

- Training data requirements

- Ongoing model maintenance

- Support SLAs and incident response

A lower license fee with high implementation complexity can exceed the cost of a higher-priced but proven solution. Vendors with established financial services deployments reduce this risk considerably. Cygnet.One clients, for instance, typically recover implementation costs within 3–6 months, with pilots starting in weeks using file drop and prebuilt templates before moving to full API integration.

Red Flags When Choosing an IDP Vendor

Template-Only Extraction with No AI Learning

If a vendor requires manual template configuration for every new document layout, it will fail in production. Real-world documents vary constantly:

- Suppliers update invoice formats without notice

- Handwritten fields appear in loan applications and forms

- Scanned documents arrive skewed, faded, or low-resolution

Modern IDP must adapt to documents it hasn't seen before — not pattern-match them against static templates.

No Compliance Audit Trail

In financial services, every extraction decision must be explainable to regulators and auditors. If a vendor cannot show complete logs — what was extracted, when, by which model version, and with what confidence score — that is a disqualifying gap. It is not a roadmap item.

No Verifiable Financial Services Deployments

Generic industry claims without specific case studies in banking, NBFC, insurance, or payments are a warning sign. Ask for references from organizations of comparable size, document volume, and regulatory complexity. A vendor's first financial services deployment should not be yours.

Frequently Asked Questions

Frequently Asked Questions

What does intelligent document processing do?

IDP uses AI and ML to automatically read, classify, extract data from, validate, and route financial documents, replacing manual data entry across loan processing, KYC, invoice handling, and compliance reporting. It handles both structured forms and unstructured correspondence with minimal human intervention.

What is an example of intelligent document processing?

A mortgage application package arrives containing a pay stub, bank statement, and ID proof. An IDP system automatically identifies each document type, extracts relevant fields, cross-validates them against credit rules, and routes the structured data to the loan origination system.

What's the difference between OCR and IDP?

OCR converts image-based text into machine-readable characters but has no understanding of what those characters mean. IDP layers AI, NLP, and ML on top of OCR to classify documents, understand context, validate extracted data, and make routing decisions, enabling it to handle the judgment-intensive steps that OCR alone cannot perform.

What is IDP in RPA?

RPA automates repetitive task execution but cannot interpret document content. IDP serves as the intelligence layer that reads and extracts structured data from documents, feeding it to RPA bots that then execute downstream tasks: updating a core banking system or posting an invoice to ERP, for example.

What types of financial documents can IDP process?

IDP handles a broad range of document types across financial operations:

- Invoices, bank statements, and loan application packets

- KYC and identity documents, insurance policies, and tax filings

- Compliance reports, contracts, and trade finance documents

This covers both structured forms and unstructured correspondence, across multiple formats and languages.

How do I evaluate an IDP vendor for financial services?

Assess accuracy on your specific document types, compliance certifications (SOC 2 Type II, relevant regulatory recognition), integration depth with your existing systems, scalability under peak loads, straight-through processing rates, and verified financial services deployments. Ask for proof from live deployments, not just curated demos.