The result is a growing application backlog. Product teams queue features for months. Compliance officers wait for developer bandwidth to update reporting workflows. Meanwhile, digitally native fintechs ship faster and capture more customers.

Low-code and no-code (LCNC) platforms have emerged as a practical answer to this problem — not as a replacement for engineering, but as a governed delivery layer that lets banks, NBFCs, and fintechs build and update digital applications significantly faster. This article covers what LCNC means in a BFSI context, why adoption is accelerating, where the highest-impact use cases are, and what risks to evaluate before committing.

Key Takeaways

- Low-code platforms use visual development with optional custom code, suited for complex financial workflows.

- No-code platforms require zero coding, suited for dashboards, forms, and simple automations.

- BFSI organisations adopt LCNC to close the gap between IT capacity and the pace of regulatory change and product launches.

- Highest-impact use cases: KYC/onboarding, loan origination, MSME invoice financing, compliance reporting, and fraud monitoring.

- Key risks (vendor lock-in, security gaps, shadow IT) are manageable with the right governance framework and platform criteria.

What Are Low-Code and No-Code Platforms?

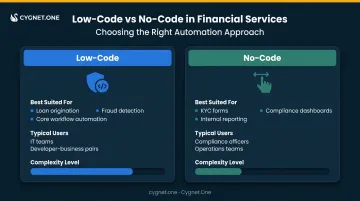

Low-code and no-code platforms are application development tools that reduce or eliminate the need to write traditional code. The distinction is practical: low-code platforms require some technical knowledge and customization, making them suited for developer-business pairs. No-code platforms are designed for domain experts — compliance officers, product managers, operations leads — with no coding ability at all. Gartner classifies these under enterprise low-code application platforms (LCAPs), while IBM emphasizes that the two serve fundamentally different users.

For financial services specifically, the distinction matters:

| Platform Type | Best Suited For | Typical Users |

|---|---|---|

| Low-code | Loan origination, fraud detection, core workflow automation | IT teams, developer-business pairs |

| No-code | KYC forms, compliance dashboards, internal reporting | Compliance officers, operations teams |

Neither replaces your core banking system or enterprise ERP. Both sit on top of existing infrastructure, connecting through APIs to extend capabilities faster than traditional development allows. Understanding this boundary — what these platforms can and can't do — is the starting point for evaluating where they fit in a financial services environment.

Why Financial Services Are Adopting LCNC at Scale Now

The IT Backlog Problem

Traditional development cycles take months. Regulatory changes arrive in weeks. The gap between the two is where digital products stall and compliance risk accumulates.

Forrester estimates the combined low-code and digital process automation market reached USD 13.2 billion by end-2023, with potential to approach USD 50 billion by 2028. That growth reflects a structural change: enterprises are treating LCNC as a core IT delivery capability, not an experiment.

The Talent Constraint

India's technology sector faces a structural skills gap. Deloitte-NASSCOM projects that demand for AI-skilled talent will grow from 600,000–650,000 to more than 1.25 million between 2022 and 2027. For NBFCs and mid-size fintechs with lean engineering teams, this gap is already a daily constraint.

LCNC allows scarce developers to focus on architecture, security, and complex integrations while product and compliance teams configure workflows directly.

Regulatory Acceleration

India's compliance environment is unusually dynamic. Key requirements update on short notice, including:

- GST e-invoicing mandates tied to NIC/GSTN portal changes

- RBI digital lending guidelines with defined implementation deadlines

- KYC/AML rules that vary by borrower segment and transaction type

Each change that requires a full development sprint creates risk: either a compliance delay or a rushed deployment that bypasses quality controls.

LCNC platforms let compliance teams modify reporting workflows and audit trails without waiting for IT queues. Cygnet.One, which processes 15–19% of India's e-invoices as an IRP and GST Suvidha Provider, maintains automatic updates aligned with NIC/GST changes — reducing the compliance lag that many BFSI clients face.

Competitive Pressure from Fintechs

Speed, not product quality, is where traditional banks and NBFCs lose ground to digital-native competitors. A fintech can push a new loan product feature in days; a bank running on legacy development cycles often cannot.

LCNC narrows that gap directly. Institutions can configure new workflows, update onboarding journeys, and adjust eligibility logic without touching the core stack — or waiting six months for an IT sprint to clear.

High-Impact Use Cases of LCNC in BFSI

Customer Onboarding and KYC

India's digital public infrastructure has transformed onboarding economics. The World Bank documented that e-KYC costs in India dropped from USD 12 to USD 0.06, making identity verification a solved problem. The remaining challenge is orchestration: connecting consent flows, CKYC records, account opening, sanctions checks, document exceptions, and audit evidence into a single governed workflow.

LCNC platforms handle this orchestration well. Compliance teams can reconfigure document requirements or add new verification steps when RBI KYC directions are updated, without rebuilding the entire onboarding application. Cygnet.One's BridgeFlow platform provides automated digital onboarding with real-time validations specifically designed for banks and NBFCs.

Loan Origination and Credit Assessment

Arab National Bank, using OutSystems, moved loan processing from 3+ days to under 24 hours and cut mortgage approval from 14 days to 5 days. A full digital SME loan origination system was delivered in under three months — a concrete benchmark for what LCNC makes possible in lending.

For Indian NBFCs, Cygnet.One's lending solutions have delivered comparable results. A leading NBFC client achieved a 95%+ reduction in report processing time through a centralised platform covering loan applications, due diligence, credit proposals, sanctions, documentation, disbursements, and utilisation tracking. Reports that previously took hours now generate in seconds.

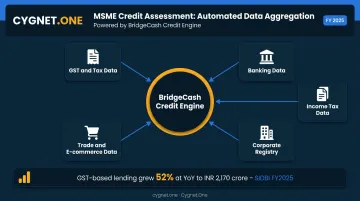

MSME and Invoice-Based Financing

India's MSME credit gap is estimated at INR 20–25 trillion by the RBI MSME Expert Committee. Closing that gap requires lenders to assess creditworthiness using alternative data — not just credit bureau scores. LCNC platforms make this practical by consolidating multiple data sources into automated decision workflows.

Cygnet.One's BridgeCash platform, launched in partnership with Ratnaafin (an NBFC), demonstrates this directly. The platform aggregates:

- GST and tax data: e-invoices, e-way bills, GST returns from GSTN

- Banking data: current accounts, savings accounts, UPI and merchant transaction data

- Income tax data: CBDT ITR summaries

- Corporate registry data: MCA filings, charges, director information

- Trade and e-commerce data: FSSAI registration, Amazon/Flipkart sales history

SIDBI's FY2025 results show that GST Sahay and TReDS digital lending outstanding grew 52% year-on-year to INR 2,170 crore — evidence that invoice and GST-data-based lending is moving from concept to operating scale. BridgeCash uses this data layer for auto-approval and auto-financing workflows that reduce manual intervention at every stage.

Compliance and Regulatory Reporting

Cygnet.One's work with BFSI clients shows what's possible in compliance automation:

- A leading private bank reduced GSTN vendor reconciliation efforts by 80%

- A banking client saved up to 350 man-hours through automated indirect tax return filing

- Another BFSI client achieved automated GSTR filing, reconciliation, and ITC management

For compliance teams managing multi-jurisdiction requirements — GST in India, VAT in the UAE, e-invoicing mandates across markets — the ability to modify reporting dashboards and audit trails without raising IT tickets is a genuine operational advantage.

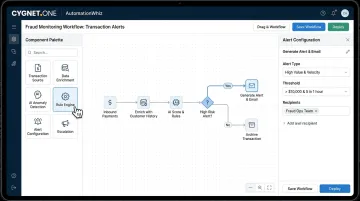

Fraud Detection and Monitoring

Fraud losses in India's banking sector continue to grow despite falling case counts, according to RBI Annual Report data — meaning individual fraud events are becoming more costly. LCNC-based monitoring tools let operations teams configure transaction anomaly detection rules and update alert thresholds as fraud patterns shift — without waiting for IT queue time or sprint cycles.

Cygnet.One's AutomationWhiz platform supports this with:

- 250+ built-in commands for transaction monitoring and alert configuration

- Drag-and-drop workflow builder for non-technical fraud and ops teams

- 50% faster deployment compared to traditional development — new detection logic goes live in weeks, not quarters

This speed matters when fraud tactics evolve faster than fixed rule sets can respond.

Core Benefits for Banks, NBFCs, and Fintechs

Speed to market is the headline benefit. Forrester's 2024 Total Economic Impact study of Microsoft Power Platform found 35% faster development for the composite organization. The same study documented 224% ROI, USD 81.7 million net present value, and payback in under six months.

Speed is just the entry point. The operational and financial advantages extend across cost, compliance, and scale:

- Cost efficiency: Cygnet.One's cloud-native modernisation work with a UK-based BNPL fintech delivered 30% lower AWS spend and 40% faster feature delivery. A digital lending platform client achieved 30% cost savings and 40% faster go-lives through container-first architecture and CI/CD automation.

- Regulatory responsiveness: Business users — not just developers — can update workflows when compliance requirements change. For institutions managing RBI mandates, GST updates, and global AML requirements simultaneously, this is operationally significant.

- Scalability without linear cost growth: Kubernetes-based auto-scaling and microservices architecture allow BFSI clients to handle transaction volume spikes without proportional headcount increases. One asset management client achieved a 3–5× improvement in platform scalability through independent service scaling.

Challenges and Key Considerations

Security and Data Governance

Not all LCNC platforms meet BFSI security requirements. Before adoption, verify:

- SOC 2 Type II certification (Cygnet.One achieved this in 2024)

- ISO 27001 information security management compliance

- Encrypted storage and data handling at rest and in transit

- Audit logging with minimum 5-year data retention

- Alignment with RBI's 2023 IT outsourcing directions and SEBI's 2024 Cybersecurity and Cyber Resilience Framework (CSCRF)

Treat security certification as a selection filter — not something to verify after contracts are signed.

Vendor Lock-In and Customisation Limits

Security is only part of the equation. Some no-code platforms also restrict how deeply workflows can be customised — a critical gap when regulatory requirements demand specific audit trails or decision logic. Evaluate platforms on:

- Open API support and connector libraries

- ERP integration capability (core banking, SAP, Oracle, Finacle, BANCS)

- Workflow export and data model portability

- Exit assistance terms in contracts

Cygnet.One supports integration with SAP, Oracle, Microsoft Dynamics, Tally, and core banking systems including Oracle, Finacle, and BANCS — with both API-based and file-drop connector options.

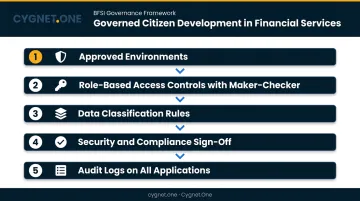

Shadow IT and Citizen Development Governance

Vendor flexibility addresses what platforms can do — but who builds on them matters just as much. When non-technical staff can deploy applications, ungoverned "shadow IT" spreads quickly. In BFSI, the stakes are high: a compliance officer building a reporting tool without IT oversight may expose sensitive data or create an unaudited workflow.

The solution is governance, not restriction. Establish:

- Approved environments for citizen development

- Role-based access controls with maker-checker workflows

- Data classification rules that define what data types non-technical builders can access

- Mandatory security and compliance sign-off before production deployment

- Audit logs on all citizen-built applications

Structured guardrails — not blanket prohibitions — are what allow financial institutions to move quickly without compromising compliance.

Frequently Asked Questions

What are low-code no-code platforms?

LCNC platforms use visual interfaces, drag-and-drop builders, and pre-built components to create applications with minimal or no hand-coding. Both IT teams and business users can build and deploy solutions significantly faster than with traditional development methods.

What is low-code no-code in banking?

In banking, LCNC refers to using visual development platforms to build, customise, and update applications — such as onboarding flows, loan origination systems, and compliance tools — without lengthy traditional development cycles. This allows banks and NBFCs to respond to regulatory changes and competitive pressures more rapidly.

What is the difference between low-code and no-code for financial institutions?

Low-code requires some coding knowledge and suits complex applications like loan origination, fraud detection, and RBI-mandated compliance workflows. No-code is fully visual and works best for simpler processes — internal dashboards, customer-facing forms, and approval flows. Both reduce IT dependency but serve different complexity levels.

Is no-code secure enough for handling financial data?

Security depends entirely on the platform chosen. Before adopting any no-code platform for sensitive financial data, institutions should verify SOC 2 Type II certification, ISO 27001 compliance, encryption standards, role-based access controls, and alignment with RBI IT governance directions.

Can low-code platforms integrate with existing core banking or ERP systems?

Most enterprise-grade low-code platforms support API-based integration with core banking systems, ERPs, and third-party services. Depth of integration varies. Evaluate connector libraries, API documentation quality, and support for systems like Finacle, BANCS, SAP, or Oracle before committing.