Introduction

Insurance operations are drowning in paperwork. Claims queues overflow. Underwriting decisions take days when customers expect hours. Policy renewals slip through the cracks, and compliance teams manually stitch together audit reports across disconnected systems.

The industry has long relied on processes built for a slower era: manual data entry, siloed approvals, spreadsheet-based tracking. That approach no longer holds up against rising customer expectations, tightening regulatory requirements, and insurtech challengers who deliver instant decisions and frictionless onboarding.

No-code business process automation gives insurance teams a way out. Underwriters, claims managers, and compliance officers can build and modify workflows through drag-and-drop interfaces, without writing code or waiting on IT. That removes the bottleneck between identifying a process problem and actually fixing it.

This article covers what no-code automation means in an insurance context, which processes it transforms most effectively, what to look for in a platform, and the measurable business outcomes insurers are achieving.

Key Takeaways

- No-code automation lets insurance teams design and deploy workflows independently, without developer involvement.

- Claims processing, underwriting, policy administration, customer onboarding, and compliance back-office functions are the highest-impact automation targets.

- Prioritize platforms with insurance-ready templates, legacy system connectors, built-in audit trails, and AI-powered document extraction.

- Measurable outcomes include shorter cycle times, lower operational costs, reduced compliance gaps, and stronger customer retention.

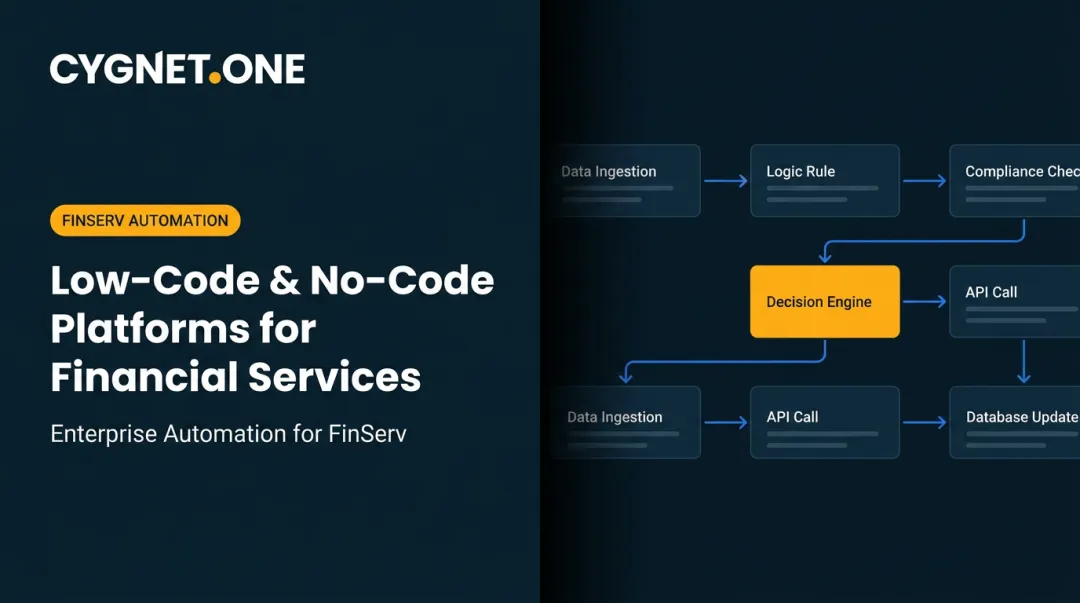

What No-Code Business Process Automation Is — and Why Insurance Needs It Now

No-code business process automation (BPA) is a software approach that lets non-technical users — claims managers, underwriters, compliance officers — design, automate, and modify workflows through visual drag-and-drop interfaces. No configuration scripts, no developer dependencies.

The distinction matters:

| Approach | Who Builds It | Deployment Speed | Flexibility |

|---|---|---|---|

| Traditional development | Developers only | Months | High but slow |

| RPA | IT/automation teams | Weeks | Good for repetitive tasks |

| Low-code | Developers + technical users | Weeks | Moderate |

| No-code BPA | Business users | Days | High for end-to-end processes |

RPA works well for isolated, repetitive tasks — data entry, screen scraping — but breaks down across multi-step processes requiring conditional logic and cross-system coordination. No-code BPA covers the full process lifecycle, and business teams can build and modify those workflows themselves.

Why Insurance Specifically Needs This Now

Several pressures are converging simultaneously:

- Customer expectations have shifted sharply toward instant, digital-first service delivery — driven by consumer experiences in banking and e-commerce

- Regulatory complexity keeps increasing, with IRDAI requirements around data maintenance, cyber security, and policyholder protection adding compliance overhead

- IT team bottlenecks mean that process improvement requests queue behind product development priorities for months

- Insurtech competition from digital-native players who run on modern, automated stacks

Underlying all four pressures is a shift in who builds process solutions. Business users — often called citizen developers — increasingly want to own their workflows rather than wait months for IT. According to IDC forecasts, the global low-code/no-code market is projected to exceed $65 billion by 2027, a signal of how deeply BFSI enterprises are committing to this model.

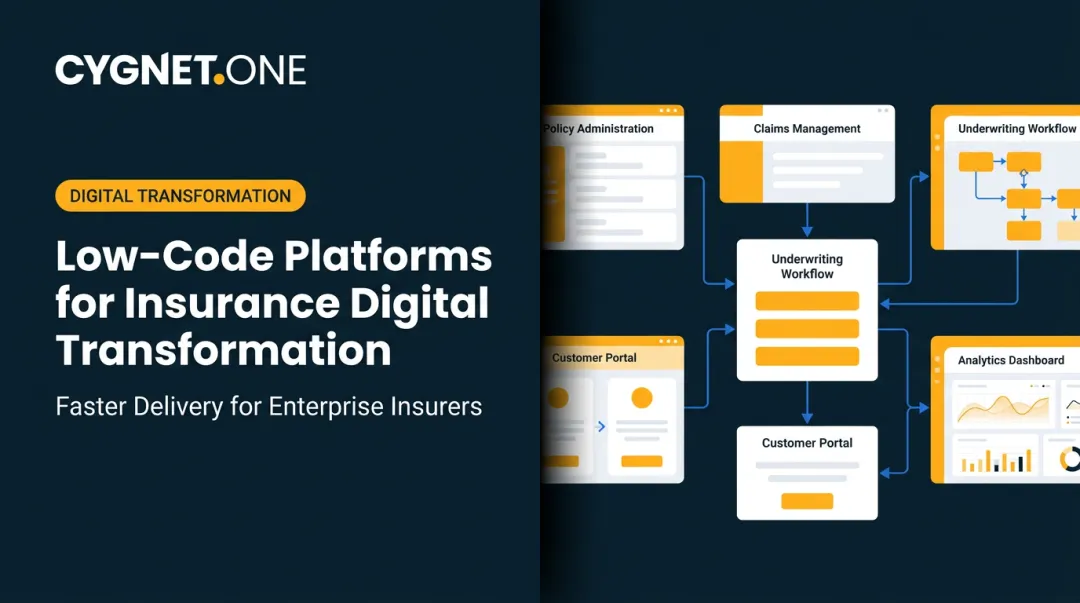

Key Insurance Processes Transformed by No-Code Automation

Insurance operations are full of high-volume, document-heavy, rule-driven workflows — exactly the conditions where no-code automation delivers the clearest value. The processes below share a common profile: long cycle times, high error rates, and heavy manual coordination. Each one is a strong candidate for automation.

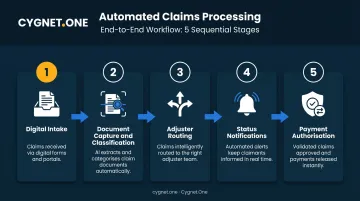

Claims Processing and Document Management

The claims lifecycle involves multiple handoffs: intake, document collection, adjuster assignment, status updates, and payment authorisation. Each handoff is a potential delay or error point when handled manually.

No-code platforms automate the full sequence:

- Digital intake — structured claim submission forms replace email and paper

- Document capture and classification — AI-powered extraction reads claim forms, medical reports, and proof-of-loss documents without manual data entry

- Adjuster routing — conditional logic automatically assigns claims based on type, value, or complexity

- Status notifications — automated triggers keep claimants informed at each stage

- Payment authorisation — rule-based approvals trigger disbursement once all conditions are met

The result is a process that moves in hours, not days, with a complete digital record at every stage.

Underwriting and Risk Assessment

Traditional underwriting requires analysts to manually pull data from multiple sources — credit reports, historical claims records, IoT feeds — then compile it for review. That's slow and inconsistent.

No-code workflows can:

- Pull data from multiple sources via API connectors automatically

- Apply pre-configured risk scoring logic across data points

- Route applications to appropriate approval queues based on risk tier

- Flag exceptions for senior review without manual intervention

Turnaround times compress significantly, and risk decisions become more consistent because the same logic applies every time.

Policy Administration and Renewal Management

Policy admin — issuance, endorsements, cancellations, renewal reminders — generates enormous administrative volume. Most of it is predictable and rule-driven, making it well-suited for automation.

No-code platforms handle:

- Automated renewal notices at configurable intervals before expiry

- Endorsement processing triggered by customer requests through self-service portals

- Cancellation workflows with appropriate regulatory notification steps

- Agent notifications for high-value policies requiring personal outreach

Automated renewal workflows reduce lapse rates while freeing agents to focus on advisory conversations rather than administrative follow-ups.

Customer Onboarding and KYC Verification

Manual onboarding creates friction that directly affects conversion rates. Coordinating form submission, document verification, KYC checks, and welcome communications across multiple teams is slow — and slow KYC causes measurable sign-up drop-off.

No-code automation simplifies the journey:

- Digital form submission with real-time validation

- Identity document upload and automated verification

- KYC and AML checks triggered automatically upon submission

- E-signature workflows integrated into the onboarding sequence

- Welcome communications sent immediately upon approval

Faster onboarding improves satisfaction scores and conversion — two metrics that compound over a customer's lifetime.

Compliance Reporting and Finance Back-Office Automation

Back-office compliance is often the last area insurers automate — but it carries significant risk when left manual. Premium reconciliation, GST filing, invoice processing, and audit reporting all fit the same profile as claims: high volume, rule-driven, and error-prone under manual handling.

Key use cases include:

- Automated reconciliation of premium collections against policy records

- GST compliance workflows for insurance premiums with automated filing triggers

- Invoice automation for claims payouts reducing processing delays

- Real-time audit trail generation across all financial transactions

Cygnet.One brings specific depth here. The company holds GSTN-approved GST Suvidha Provider status, has implemented GST reconciliation and vendor payment automation for BFSI clients, and processes a significant share of India's e-invoice volumes — capabilities that translate directly to insurers managing complex indirect tax compliance alongside operational workflows.

Must-Have Features in a No-Code Insurance Automation Platform

Evaluating no-code platforms requires knowing what to demand, not just what's available. Five capabilities consistently separate platforms that work for insurance from those that don't.

Insurance-Ready Templates and Pre-Built Modules

Generic no-code platforms require extensive configuration before they're useful for insurance. Purpose-built or insurance-ready platforms come with templates for claims workflows, underwriting queues, policy administration, and customer portals — reducing implementation timelines from months to weeks.

Ask vendors specifically: what's available out of the box for insurance, and what requires custom build?

Visual Workflow Builder with Conditional Logic

The drag-and-drop interface must support real decision logic — not just linear sequences. Insurance workflows are conditional: "if claim value exceeds ₹5 lakh, route to senior adjuster; if medical documents are incomplete, trigger request to claimant."

Business users need to build these decision trees themselves, test them in a sandbox environment, and iterate without IT involvement. Platforms that require scripting for conditional logic defeat the purpose.

API Connectors and Legacy System Integration

Most insurers run on legacy core systems — policy management platforms, CRMs, billing systems — that aren't going away anytime soon. A no-code platform that can't connect to these systems is only useful at the edges.

This is frequently the make-or-break factor for enterprise insurers. Look for:

- Pre-built connectors to common insurance and BFSI core systems

- Open REST API support for custom integrations

- Middleware capability to bridge legacy and modern systems

- Documented integration with ERP platforms (SAP, Oracle, Dynamics)

Built-In Compliance Controls and Audit Trails

Insurance is a regulated industry. Automation tools must include granular role-based access controls, version-controlled workflow history, and automatically generated audit logs.

For IRDAI compliance specifically, audit trails must demonstrate:

- Processes executed according to defined rules

- Access to policyholder data appropriately restricted by role

- Workflow changes tracked and authorized with timestamps

Platforms that treat audit trails as an afterthought create compliance exposure rather than reducing it.

AI-Enabled Document Processing

No-code platforms without AI document capabilities still require manual document handling — which limits their value in insurance. Look for:

- Reads scanned claim forms, identity documents, and medical reports via OCR

- Classifies document type automatically without manual routing

- Extracts structured fields from unstructured text using NLP

Cygnet.One's Intelligent Document Processing uses Vision Language Model (VLM) technology to extract line-level financial data from both structured and unstructured documents, and validates it against business and compliance rules automatically.

Business Benefits and ROI of No-Code Automation in Insurance

Speed: Faster Processes and Faster Deployment

No-code automation compresses two timelines simultaneously. Internally, process cycle times shrink as manual steps are eliminated. Externally, new workflows can be designed, tested, and deployed in days rather than months.

Gartner forecasts that the low-code development technologies market will continue growing at approximately 20% annually, and speed is the primary driver. Insurers who can respond to regulatory changes or market opportunities by updating workflows in days hold a structural advantage over competitors locked into multi-month IT delivery cycles.

Cost Reduction and Resource Reallocation

Automation reduces costs in two ways: directly, by eliminating manual labour hours in claims processing, policy admin, and reconciliation; and indirectly, by reducing IT dependency for process changes.

The result is a meaningful shift in how skilled staff spend their time:

- Claims adjusters focus on complex case review rather than data entry

- Compliance officers shift from manual tracking to exception handling

- Policy administrators move from coordination tasks to customer advisory work

Accuracy, Compliance, and Scale

Manual processes introduce errors that compound at volume. A data entry mistake on a single claim is minor; the same error pattern across thousands of claims creates financial exposure and potential regulatory findings.

Automation enforces rules consistently across every transaction. Conditional logic applies the same thresholds, the same routing rules, and the same notification triggers regardless of volume or time pressure. For insurers with high transaction volumes — premium collections, claims payouts, reconciliation cycles — this accuracy improvement has material financial impact.

Cygnet.One's documented outcomes for BFSI and enterprise clients include 90% faster process cycles and 60% reduced invoice processing time.

Customer Experience and Competitive Positioning

Faster claims resolution, real-time policy self-service, and faster digital onboarding translate directly into customer satisfaction and retention. These aren't soft benefits — insurers with higher NPS scores and lower churn rates have measurably better unit economics.

No-code automation is increasingly a competitive differentiator, not just an operational efficiency tool. Digital-native insurtechs built their operations on automation from day one. Traditional insurers who adopt no-code BPA close that gap without requiring a full technology overhaul.

Common Challenges and How to Overcome Them

Cultural Resistance and Governance Gaps

The biggest barrier to no-code adoption is often internal. Teams accustomed to IT-driven development may resist taking ownership of workflows. Others may build automations without adequate oversight, creating security or compliance risks.

A phased approach works best:

- Identify one high-friction process with clear metrics

- Automate it with IT supervision and cross-functional input

- Measure results against baseline

- Expand scope based on demonstrated outcomes

Governance policies are non-negotiable: define who can build, test, publish, and modify automations. Establish data access standards and security review requirements before scaling citizen development broadly.

Platform Selection Checklist

Once governance is in place, the next question is which platform can actually handle insurance workflow complexity. Before committing, confirm these criteria:

- Insurance-specific templates available out of the box

- Pre-built or open API connectors to your existing core systems

- Built-in compliance controls with automatically generated audit trails

- Role-based access with granular permissions per user or team

- Vendor security certifications relevant to insurance procurement (such as SOC 2 Type II)

- Enterprise SLAs, implementation support, and managed services on offer

Cygnet.One holds SOC 2 Type II certification — a security posture that satisfies enterprise insurance procurement requirements.

Frequently Asked Questions

What are no-code automations?

No-code automations are software systems that let users design and run automated workflows through visual, drag-and-drop interfaces — without writing programming code. Business teams handle repetitive processes independently of IT, reducing both delay and cost.

What are the 4 stages of process automation?

The four stages are:

- Process discovery and mapping — identifying what to automate

- Design and configuration — building the workflow logic

- Deployment and testing — going live and validating outcomes

- Continuous monitoring and optimisation — measuring performance and refining over time

Will RPA be replaced by AI?

RPA and AI are complementary, not competing. AI adds decision-making and document understanding to RPA's rule-based strengths, and no-code BPA platforms are incorporating both. Standalone RPA remains useful, but increasingly as one component within broader intelligent workflows.

Which insurance processes benefit most from no-code automation?

Claims processing, underwriting workflows, policy administration, customer onboarding, KYC verification, and compliance/finance back-office processes deliver the highest impact. All of these share the same profile: high transaction volumes, rule-driven logic, and heavy document handling — the conditions where no-code automation consistently delivers results.

How does no-code automation help with regulatory compliance in insurance?

No-code platforms enforce rule-based logic consistently across all transactions, generate automatic audit trails, and support role-based access controls. This makes it far easier for insurers to demonstrate compliance with IRDAI and equivalent regulatory requirements during audits, without relying on manually assembled documentation.