Introduction

Banking operations don't fail gradually — they collapse fast. A core banking outage, a payment rail failure, or a ransomware attack can lock customers out of accounts within hours, trigger regulatory investigations, and cost millions in compensation. Cyberattacks against financial firms have nearly doubled since before COVID-19, the sector accounts for nearly one-fifth of all reported cyber incidents globally, and financial firms have absorbed almost $12 billion in direct cyber losses since 2004.

Regulators have responded. Each of the major frameworks now demands documented plans, evidence of testing, and audit trails:

- DORA (effective January 2025) — mandates ICT business continuity policies and annual testing for EU financial entities

- RBI guidelines — operational resilience requirements for Indian banks and NBFCs

- FFIEC handbooks — business continuity standards for US financial institutions

- ISO 22301 / Basel III — internationally recognized continuity and operational risk frameworks

Yet many banks still manage continuity through static PDFs and disconnected spreadsheets. That gap creates direct regulatory exposure — and closes fast when an incident hits.

This guide compares the top BCM platforms built for banking environments in 2026, evaluated on regulatory alignment, core functionality, integration capability, and real-world incident response.

Key Takeaways

- BCM software automates recovery planning, crisis communication, BIA, and regulatory compliance in one platform

- Generic risk tools lack banking-specific workflows: no FFIEC-aligned BIA templates, no payment outage scenarios

- Top platforms covered: Riskonnect, Fusion Risk Management, Ncontracts (Ncontinuity), Everbridge, and MetricStream

- Key selection criteria: regulatory alignment (FFIEC/DORA/ISO 22301), RTO/RPO tracking, mass notification, audit-ready documentation

- Choosing the right BCM tool means building active resilience, not just storing recovery documents

What Is BCM in Banking — and Why Does It Matter?

Business Continuity Management (BCM) in banking is the structured process of identifying critical operations (payments, lending, customer access, regulatory reporting), assessing threats to those operations, and maintaining pre-tested plans to restore them within defined timeframes. Those timeframes are formalized as Recovery Time Objectives (RTOs) and Recovery Point Objectives (RPOs).

BCM differs from disaster recovery (DR). Where DR focuses on restoring IT systems after failure, BCM covers the full lifecycle: threat identification, business impact analysis, crisis response, stakeholder communication, and post-incident review. Both are necessary — but DR without BCM leaves business units without coordinated recovery procedures.

The Regulatory Imperative

Banks cannot treat BCM as optional. Key frameworks include:

- FFIEC BCM Handbook (US): Examiner guidance covering BIA, risk assessment, risk management, and risk monitoring/testing for US financial institutions

- RBI IT Master Direction 2023 (India): Covers IT governance, BCP/DR requirements, and includes annual BCP/DR review provisions for regulated entities

- ISO 22301:2019: International standard requiring a documented BCMS with ongoing monitoring, review, maintenance, and improvement

- DORA (EU, from January 2025): Mandates ICT business continuity policy, BIA, response and recovery plans, and at least yearly testing for critical functions

- Basel III / BCBS Operational Resilience: Requires banks to identify critical operations, map dependencies, maintain BCPs, and conduct regular exercises under severe-but-plausible scenarios

The UK Treasury Committee found 803 hours of unplanned tech outages across nine major banks between January 2023 and February 2025. One Barclays outage in early 2025 caused 56% of online payments to fail, with expected customer compensation of £5M–£7.5M.

Regulators across these frameworks require documented testing evidence, timestamped audit trails, and demonstrable exercise histories — none of which spreadsheet-based BCM can reliably produce at examination time.

Top BCM Software for Banks in 2026

These five platforms were evaluated on banking-sector regulatory alignment, depth of core BCM functionality (BIA, plan management, incident activation, testing), integration with banking infrastructure, and verified presence in financial services.

Riskonnect

Riskonnect is an integrated risk management platform that unified business continuity and enterprise GRC capabilities following its acquisition of Castellan Solutions in July 2022. It targets mid-to-large financial institutions with complex, multi-site risk programs.

Key differentiators for banks:

- Pre-built templates aligned with major compliance frameworks, with real-time dashboards showing plan readiness, testing status, and recovery gaps

- Configurable architecture lets banks model resilience across branches, data centers, and third-party providers without custom development

- BIA-derived strategies link automatically into recovery plans, reducing manual maintenance overhead

| Feature Area | Details |

|---|---|

| Key Banking Features | Automated BIA workflows, multi-site continuity planning, version-controlled plan management, crisis management activation, mass notification |

| Regulatory Alignment | ISO 22301, DORA, Basel III, FFIEC, CPS 232 — pre-built compliance reporting for audit trails |

| Best For | Mid-to-large banks, multinational financial institutions, banks with mature GRC programs |

Note: Riskonnect's Castellan acquisition is verified (July 2022). Specific regulatory framework certifications should be confirmed directly with the vendor before finalizing procurement.

Fusion Risk Management

Fusion is an enterprise operational resilience platform built around process-dependency modeling — mapping how disruptions cascade across business units, technology stacks, and vendor relationships. It has documented adoption by large financial services organizations.

Fusion's process-centric dependency mapping lets risk teams visualize how a core banking failure or payment processor outage propagates across the institution. Scenario-based stress testing is well suited to banks with complex, multi-vendor technology stacks and numerous third-party dependencies.

An official case study documents a financial services firm with 15,000–20,000 employees using Fusion to unify business continuity and disaster recovery.

| Feature Area | Details |

|---|---|

| Key Banking Features | Operational dependency mapping, automated BIA, scenario-based stress testing, recovery strategy documentation, incident management workflows |

| Regulatory Alignment | References financial sector regulatory expectations; specific framework certifications should be confirmed with the vendor |

| Best For | Large banks and global financial institutions needing granular visibility into process and technology dependencies |

Ncontracts (Ncontinuity)

Ncontinuity is the most purpose-built BCM platform for US-regulated financial institutions. Ncontracts acquired Quantivate in December 2023, integrating BCM with vendor management, compliance, audit, and IT risk in a unified GRC environment.

Ncontinuity is explicitly designed around FFIEC Business Continuity Management guidelines. Its BIA workflows, customizable plan templates, and multi-channel mass notification — SMS, email, voice, and mobile app with geofencing — are built around banking operational realities.

Named adopters include Montecito Bank and Trust, Guadalupe Credit Union, and First Dakota National Bank.

| Feature Area | Details |

|---|---|

| Key Banking Features | FFIEC-aligned BIA workflows, customizable BCP templates, multi-channel mass notification with geofencing, vendor risk integration, compliance and audit modules |

| Regulatory Alignment | Purpose-built for FFIEC; integrates with broader US financial institution compliance frameworks |

| Best For | Community banks, credit unions, and mid-market financial institutions seeking a banking-native BCM platform |

Everbridge (including BC in the Cloud)

Everbridge combines two complementary capabilities: its Critical Event Management (CEM) platform for enterprise mass notification, and BC in the Cloud — acquired via the Infinite Blue purchase in July 2024 — for end-to-end continuity program management.

When speed of communication is paramount — cyberattacks, ATM network failures, branch incidents — Everbridge's multi-channel alerting (SMS, voice, email, mobile, desktop) delivers targeted notifications simultaneously. BC in the Cloud adds BIA, dependency mapping, and plan activation.

CIBC Mellon is a documented financial services adopter using Everbridge for business continuity and critical communication planning.

| Feature Area | Details |

|---|---|

| Key Banking Features | Geolocation-based mass notification, multi-channel emergency alerting, BIA, dependency mapping, plan activation, recovery workflow automation |

| Regulatory Alignment | Supports sector-specific regulatory alignment and audit-ready documentation; specific ISO/FFIEC certification claims should be confirmed with the vendor |

| Best For | Large, globally distributed banks prioritizing rapid crisis communication alongside BCM planning |

MetricStream

MetricStream is an enterprise GRC platform with a dedicated business continuity module, widely used by large, highly regulated financial institutions. It integrates BCM with operational risk management, internal audit, and compliance.

MetricStream suits banks that need BCM tightly woven into their broader operational risk framework — linking continuity plans directly to risk registers, internal controls, and audit findings.

Named financial-sector clients include Standard Chartered Bank and LSEG, with an anonymized global bank case study also on record. The platform supports Basel standards alongside regulatory requirements from FFIEC, OCC, and the Bank of England, per official MetricStream content.

| Feature Area | Details |

|---|---|

| Key Banking Features | Integrated BCM and operational risk management, scenario analysis, dependency mapping, crisis workflow automation, internal audit integration |

| Regulatory Alignment | Basel standards, FFIEC, OCC, FRB, and Bank of England frameworks referenced in official content; ISO 22301 BCM certification should be confirmed directly |

| Best For | Large banks and financial holding companies seeking deep BCM-to-GRC integration on a single enterprise platform |

How We Chose the Best BCM Software for Banks

Evaluation Approach

Banks frequently select generic enterprise risk tools that lack banking-specific workflows — no FFIEC-aligned BIA templates, no payment outage scenarios, no integration with core banking monitoring systems. The platforms above were evaluated specifically against banking-sector requirements:

- Covers major regulatory frameworks: FFIEC, DORA, RBI, ISO 22301, and Basel III

- Delivers core BCM functionality — BIA, plan management, incident activation, exercise management, and audit trails

- Connects with core banking systems, IT monitoring, HR platforms, and third-party vendor risk tools

- Has verified financial services adoption, with named or documented banking clients and use cases

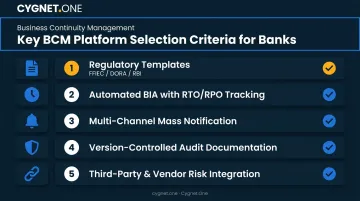

Key Selection Factors

The criteria above reflect platform-level capabilities. When narrowing down options for your specific institution, these decision factors matter most:

- Pre-built templates aligned to your regulatory jurisdiction (FFIEC for US, DORA for EU, RBI for India)

- Automated BIA workflows that capture RTO/RPO for critical processes — payments, digital services, core banking

- Mass notification across multiple channels for rapid stakeholder alerting

- Version-controlled plan management that produces audit-ready documentation

- Third-party and vendor risk integration, since most banking disruptions now involve supply chain failures

Scalability and Integration as Non-Negotiables

A BCM tool that cannot connect to core banking infrastructure, IT monitoring systems, or HR platforms creates dangerous silos during a crisis. Before selecting a platform, confirm three things:

- API availability and how it connects to your existing tech stack

- Native integrations with core banking and IT monitoring tools you already run

- Financial-services implementation support — not just generic onboarding

Conclusion

Choosing BCM software for a bank is not a standard enterprise software decision. It requires a platform that understands the risk topology of financial institutions: regulatory scrutiny, real-time payment dependencies, customer trust implications, and multi-jurisdiction compliance requirements.

Before finalizing a platform, conduct a structured pilot with a single business unit, validate the vendor's regulatory compliance claims against your jurisdiction's specific requirements, and assess whether the tool will drive adoption across both IT and business continuity teams. The strongest BCM platform is only as effective as the teams trained to use it under pressure.

While BCM software handles crisis planning and operational resilience, banks also need financial compliance infrastructure that holds up during disruptions. Cygnet.One's tax and finance transformation platform ensures GST compliance, e-invoicing, and regulatory filings remain audit-ready even when operations are under stress.

For Indian banks managing GSTN-regulated compliance workflows, Cygnet.One's dual status as a GSTN-approved IRP and GSP adds a layer of regulatory assurance that complements your broader BCM strategy.

Frequently Asked Questions

What is BCM in banking?

BCM in banking is the structured process of identifying critical operations — payments, lending, customer access, regulatory reporting — assessing potential disruptions, and maintaining tested plans to restore those operations within defined RTOs and RPOs. Regulators across most jurisdictions, including the RBI, FFIEC, and EU under DORA, now require formal BCM programs for financial institutions.

What is a BCP in banking?

A Business Continuity Plan (BCP) is a documented set of procedures defining how a bank will maintain or quickly restore essential operations during a disruption. It covers crisis response, communication protocols, recovery steps, and roles and responsibilities for each critical function.

What are the four pillars of a BCP in banking?

The four recognized pillars, aligned with FFIEC and BCBS frameworks, are:

- Business Impact Analysis — identifies critical processes and recovery requirements

- Risk Assessment — evaluates threats and vulnerabilities

- Recovery Strategies — defines how operations will be restored

- Plan Testing and Maintenance — keeps plans current through regular drills and reviews

Which BCM platform is most reliable for banks?

Reliability depends on bank size and regulatory jurisdiction. Ncontracts (Ncontinuity) is the strongest purpose-built option for US-regulated community banks and credit unions. Riskonnect and Fusion are better suited to large, globally distributed institutions. MetricStream suits banks needing deep GRC integration.

How often should banks test their business continuity plans?

DORA mandates at least annual testing for ICT systems supporting critical functions. BCBS operational resilience principles require regular exercises under severe-but-plausible scenarios. Most modern BCM platforms automate exercise scheduling and capture audit-ready results automatically.

What regulations require banks to have a formal BCM programme?

Key frameworks include: RBI IT Master Direction 2023 (India), FFIEC Business Continuity Management handbook (US), ISO 22301:2019 (international), DORA effective January 2025 (EU), and Basel III operational risk requirements. Specific obligations vary by geography and institution type — requirements differ materially between, for example, a US community bank and an EU systemic institution.