The stakes in vendor selection are real. The wrong platform locks you into poor extraction accuracy, broken integrations, and compliance gaps that take years to unwind. The right one compresses processing timelines and directly improves revenue cycles and audit outcomes.

The market signals urgency here: according to Grand View Research, the global intelligent document processing market was valued at USD 2.30 billion in 2024 and is projected to reach USD 12.35 billion by 2030 at a 33.1% CAGR — with BFSI holding the largest revenue share in 2024. This isn't a nascent technology. It's becoming standard infrastructure for financial operations.

This guide covers what document automation actually does in financial services, what to evaluate when selecting a vendor, and how platforms like Cygnet.One address multi-jurisdiction compliance at enterprise scale.

Key Takeaways

- Document automation uses AI, OCR, and NLP to capture, extract, validate, and route financial document data — reducing manual intervention across invoicing, lending, and compliance workflows

- Core use cases: loan origination, KYC/AML compliance, invoice processing, mortgage approvals, and audit management

- When evaluating vendors, prioritize regulatory credentials, extraction accuracy, ERP integration depth, scalability, and security certifications

- The right vendor reduces processing time significantly while maintaining audit-ready compliance trails

- Cygnet.One holds government-backed compliance credentials across six jurisdictions and processes over 412 million e-invoices through its platform

What Is Document Automation for Financial Services?

Document automation in financial services uses AI, machine learning, NLP, and OCR to capture, classify, extract, validate, and route data from financial documents with minimal human intervention. It applies across structured forms and unstructured documents alike: scanned PDFs, handwritten notes, multi-format bank statements, and complex multi-page loan files.

Common document types include:

- Invoices and purchase orders

- Bank statements and financial reports

- Loan applications and mortgage files

- KYC/identity documents

- Tax filings and GST/VAT returns

- Insurance claims and audit reports

- Regulatory filings and compliance submissions

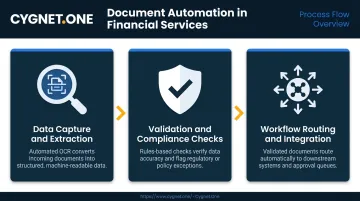

Core Components of Document Automation

Data Capture and Extraction

AI-powered OCR combined with NLP reads both structured forms and unstructured documents, pulling specific fields (account numbers, transaction amounts, entity names, tax identifiers) even when document layouts vary. For financial workflows, extraction accuracy is non-negotiable. A small error rate on loan amounts or tax fields triggers downstream reconciliation failures.

Cygnet.One's platform uses Vision Language Model (VLM)-based Intelligent Document Processing through its GLIB.ai engine, processing bank statements in any format — digital, scanned, AA JSON, or direct core banking integration — while minimizing the need for manual verification.

Validation and Compliance Checks

Automated validation layers cross-check extracted data against predefined rules, regulatory schemas, and internal policy logic before documents move downstream. This is where compliance risk gets caught — flagging anomalies in KYC submissions, AML screening matches, or GST/VAT discrepancies at the point of extraction rather than after filing.

Workflow Routing and Integration

Validated data routes directly into ERP systems, core banking platforms, or CRMs based on document type and approval hierarchy. This eliminates manual handoffs and accelerates approval cycles, cutting loan decision timelines from days to minutes.

Together, these three components address the most costly friction points in financial document workflows.

Why Financial Services Relies on Document Automation

Key operational benefits:

- Faster loan and mortgage turnaround

- Reduced manual errors in invoicing and reconciliation

- Improved KYC/AML accuracy and audit-readiness

- Lower cost-per-document at scale

- Faster customer onboarding through automated data collection

What to Consider When Choosing a Document Automation Vendor

Vendor selection in financial services is not a commodity decision. The wrong choice creates regulatory exposure, integration failure, or accuracy gaps that compound over time. The following criteria help procurement teams map vendor capabilities directly to operational and compliance outcomes.

These factors apply whether you're a bank, NBFC, insurance company, or fintech — but the weighting shifts depending on document volume, regulatory jurisdiction, and existing technology stack.

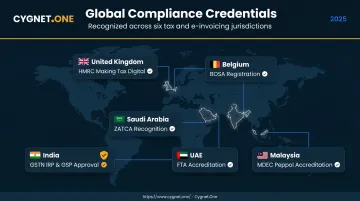

Regulatory Compliance and Certification Coverage

This is the foundational criterion. A vendor operating in financial services must hold verifiable approvals from the regulators governing your markets — not just generic SOC 2 certification, but jurisdiction-specific recognitions.

| Jurisdiction | What to Look For |

|---|---|

| India | GSTN IRP and GSP approval |

| Saudi Arabia | ZATCA recognised e-invoicing provider |

| United Kingdom | HMRC Making Tax Digital compatible software |

| UAE | Ministry of Finance accredited e-invoice service provider |

| Belgium | BOSA registered e-invoice compliant software |

| Malaysia | MDEC accredited Peppol service provider |

Compliance credentials directly affect audit pass rates, penalty risk exposure, and cross-border processing speed for multi-market institutions. A vendor without jurisdiction-specific recognition cannot be relied upon for regulatory submissions in that market, regardless of their general technology capability.

Cygnet.One holds credentials across all six jurisdictions listed above — IRP and GSP approval in India, ZATCA recognition in Saudi Arabia, HMRC compatibility in the UK, FTA accreditation in the UAE, BOSA registration in Belgium, and MDEC accreditation in Malaysia — enabling regulatory submissions across each market without relying on third-party intermediaries.

AI Extraction Accuracy and Document Variability Handling

In financial services, extraction errors in loan amounts, tax fields, or account identifiers can trigger reconciliation failures, reporting inaccuracies, or fraud exposure. Accuracy must be evaluated across:

- Variable document formats and layouts

- Multi-page financial documents with mixed-format tables

- Low-quality or scanned inputs

- Regional languages if operating in multilingual markets

Peer-reviewed benchmarking from the DocILE dataset — which used 6,680 annotated business documents — reported F1 scores well below perfect extraction even for leading models. This matters: don't accept generic accuracy claims. Request benchmark testing on your own document samples.

Cygnet.One's GLIB.ai OCR engine has been trained on document samples across invoice types, GST filings, and bank statement formats — prioritise vendors who can demonstrate extraction performance on the specific document types your institution processes, not just generic benchmarks.

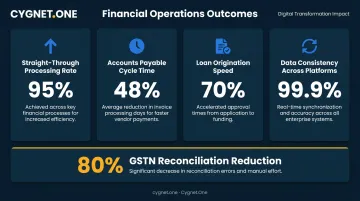

ERP and Core Banking System Integration

Document automation delivers maximum ROI only when extracted data flows directly into existing systems — ERP platforms, core banking software, accounting tools, or CRM systems — without manual re-entry. Integration depth determines whether automation eliminates handoff bottlenecks or simply relocates them.

Metrics this affects:

- Straight-through processing rates

- Accounts payable cycle times

- Loan origination speed

- Data consistency across platforms

Cygnet.One's platform supports APIs and file-drop connectors for integration with core banking systems, ERPs including Oracle, Finacle, and BANCS, and has completed 250+ successful ERP integrations. In one documented case, a leading private bank reduced GSTN vendor reconciliation effort by 80% through integration with Oracle Payment Apps.

Request integration case studies specific to your stack, and prioritise live reference calls over published benchmarks — public STP-rate data for core banking integrations is scarce, making direct customer references the more reliable evaluation signal.

Scalability and Transaction Volume Capacity

Financial institutions processing millions of invoices, loan files, or compliance documents monthly need infrastructure that scales without performance degradation. Cloud-based platforms with elastic capacity are preferred over on-premise solutions that require manual capacity planning at peak periods.

Scalability also applies to document type diversity: as business grows, the automation layer must handle new document categories without full retraining cycles.

AIIM's 2025 enterprise survey found that 61% of IDP processes still involve paper and 48% of enterprises expect paper volumes to increase — meaning scalability requirements are not shrinking.

Cygnet.One's AWS-native infrastructure uses container-based deployment with Kubernetes-enabled horizontal auto-scaling and CloudWatch monitoring, achieving 99% platform uptime. The platform processes over 55 million transactions monthly, with infrastructure capable of 5-minute scale-up times during demand spikes.

Data Security and Privacy Architecture

Financial documents contain highly sensitive PII, transaction data, and proprietary business information. Security requirements are non-negotiable.

Baseline certifications to require:

- SOC 2 Type II compliance (covers security, availability, confidentiality, processing integrity, and privacy trust service criteria)

- ISO 27001:2022 certification

- Documented incident response policies and penetration testing history

- Data residency options for regulated markets

Beyond certifications, verify that the vendor's framework aligns with the data protection regulations in each market you operate in.

Regulatory frameworks to assess by market:

- GDPR for EU-based operations — requires lawful processing, data minimisation, processor contracts, and breach notification under documented controller-processor agreements

- India's DPDP Act 2023 — requires lawful purpose, consent, safeguards, and data erasure when purpose ends

- Equivalent jurisdictional standards for UAE, UK, and other operating markets

Cygnet.One holds SOC 2 Type II compliance, SOC 1 Type I certification, and ISO 27001:2022 certification. Their security framework includes encrypted storage, endpoint and identity security, and GRC services aligned with SOC 2 and ISO 27001 standards.

Implementation Model and Post-Go-Live Support

Even technically superior platforms fail when implementation is poorly managed. Vendors should offer structured onboarding, dedicated integration support, and training for finance and operations teams accustomed to manual workflows.

Key questions to ask:

- What does the phased deployment model look like?

- Is there a pilot option using file drop and pre-built templates before full API rollout?

- What are SLA commitments post-go-live?

- Does the vendor have experience implementing for institutions of comparable size and document volume?

Cygnet.One's approach includes discovery phases to map end-to-end workflows, co-existence migration options that avoid disruption, and 24/7 infrastructure monitoring with automated escalation workflows and real-time incident dashboards.

How Cygnet.One Can Help

Cygnet.One is a finance and tax transformation platform with 25 years of enterprise deployment experience, purpose-built for the compliance and scale demands of banks, NBFCs, insurers, and large enterprises.

Platform scale:

- 412 million+ e-invoices generated through the platform

- 55 million+ transactions processed monthly

- 15–19% of India's e-invoice volumes processed through Cygnet's IRP

Compliance credentials across six jurisdictions:

- IRP and GSP approval from GSTN (India)

- ZATCA recognition (Saudi Arabia)

- HMRC recognition (UK)

- FTA approval and Muwafaq recognition (UAE)

- BOSA registration (Belgium)

- MDEC accreditation (Malaysia)

Measurable outcomes for financial services clients:

- 95% reduction in report processing time — an India-based microfinance NBFC reduced report creation from 4–5 days to seconds

- 60% reduction in invoice processing time — a global FMCG group in the GCC achieved full e-invoice compliance with enhanced reconciliation accuracy

- 80% reduction in loan processing turnaround time through automated bank statement analysis

- 250+ successful ERP integrations across Oracle, Finacle, BANCS, and other platforms

- SOC 2 Type II compliance and 99% platform uptime

Beyond technology infrastructure, Cygnet.One operates as both a technology solution provider and a loan solution provider. Its BridgeCash platform automates credit assessment using GST, banking, and financial statement data, combining ITC insight dashboards, CFO-level reporting tools, and AI-driven IDP analysis for creditworthiness evaluation. This makes it well-suited for NBFCs and lenders requiring end-to-end document-to-decision workflows.

The 2025 partnership with Ratnaafin for MSME invoice financing demonstrates this dual capability in practice. Cygnet's e-invoice infrastructure surfaces eligible invoices from its 1B+ monthly transaction pipeline. BridgeCash validates and processes them, and lenders receive automated credit decisions with full audit trails — all on a single platform, from document to disbursement.

Conclusion

Choosing a document automation vendor for financial services is a compliance and operational infrastructure decision — not a software purchase. The vendor must match your regulatory geography, document volume, integration complexity, and accuracy requirements before any feature comparison matters.

The most capable vendor on paper may not be the right fit without proven deployment at scale, jurisdiction-specific compliance credentials, and structured post-implementation support. Reference checks with institutions of comparable size and complexity are worth the time investment.

Vendor selection is also the start of an ongoing relationship, not a one-time deployment. Build evaluation cycles into your roadmap for:

- Extraction accuracy benchmarks as document types and formats evolve

- Emerging capabilities in agentic document workflows and real-time decisioning

- Regulatory changes across every jurisdiction you operate in

The right vendor grows alongside these demands — not just at go-live, but through every compliance update and operational shift that follows.

Frequently Asked Questions

What is document automation in financial services?

Document automation uses AI, OCR, and NLP to automatically capture, extract, validate, and route data from financial documents — reducing manual intervention across processes like loan origination, invoicing, and KYC. It applies to both structured forms and unstructured documents like scanned PDFs or handwritten inputs.

What types of financial documents can be automated?

Modern AI-based systems handle invoices, bank statements, loan applications, KYC/identity documents, mortgage files, tax returns, insurance claims, audit reports, and regulatory filings. Both structured and unstructured formats are supported, including scanned, digital, and mixed-layout documents.

How does document automation improve regulatory compliance?

Automated validation layers enforce compliance rules at the point of extraction, generate audit-ready trails, and reduce human error in regulatory filings. Systems can be configured to meet jurisdiction-specific requirements across KYC, AML, GST, VAT, and e-invoicing mandates.

What is the difference between OCR and intelligent document processing?

OCR converts text from images into machine-readable format but cannot interpret meaning or handle layout variability. IDP adds AI and NLP layers to classify content, extract specific fields accurately, and improve with use — making it far more capable for complex financial documents.

How long does it take to implement a document automation solution?

Full enterprise deployment typically ranges from a few weeks to several months, depending on document complexity, integration scope, and workflow requirements. A phased approach — starting with pre-built templates for high-volume documents before moving to full API integration — delivers faster time-to-value.

What security certifications should a financial services document automation vendor hold?

SOC 2 Type II compliance is the baseline. Beyond that, look for:

- ISO 27001 certification and documented encryption standards

- Role-based access controls and data residency options

- Jurisdiction-specific recognition — such as GDPR alignment for EU operations or DPDP Act compliance for India