Introduction: Why Predictive Analytics Is Now a Core Banking Imperative

Mobile banking is near-universal. According to McKinsey, 73% of global banking interactions now occur through digital channels , making digital access table stakes rather than a differentiator. Meanwhile, fintech revenues are projected to grow at 15% annually through 2028, roughly three times the 6% growth rate forecast for traditional banking.

That gap puts pressure on banks and NBFCs from both sides: customers expect personalized, proactive service, while regulators demand tighter controls. Reacting after a default, a fraud event, or a compliance breach is no longer a viable strategy.

Predictive analytics addresses this directly. Leading institutions are using it to anticipate fraud before it occurs, flag loan defaults before they materialize, and identify at-risk customers before they churn.

The global predictive analytics in banking market was valued at USD 3.63 billion in 2024 and is projected to reach USD 19.61 billion by 2033 — a 20.6% CAGR. For banks and NBFCs still evaluating adoption, that trajectory signals urgency, not optionality.

This guide covers the key use cases, measurable business benefits, common implementation pitfalls, and a practical vendor evaluation framework for banking and NBFC leaders moving from exploration to deployment.

Key Takeaways

- Predictive analytics lets banks act on early signals — catching fraud, credit defaults, churn, and compliance gaps before they become costly problems

- Top use cases: fraud detection, credit risk, churn prevention, AML monitoring, liquidity forecasting, and cross-selling

- NBFCs can extend credit to previously unscoreable borrowers using alternative data (GST, UPI, utility, e-commerce)

- Main implementation barriers: data silos, legacy system integration, and explainability requirements for regulators

- When evaluating vendors, prioritize domain expertise, real-time processing capability, model transparency, and integration depth

What Is Predictive Analytics in Banking?

Predictive analytics uses statistical algorithms, machine learning, and AI to analyse historical and real-time data. That includes transaction histories, credit records, customer behaviour, and market signals — processed together to forecast future outcomes and support more accurate credit, risk, and customer decisions.

The clearest way to understand it is by contrast. Descriptive analytics tells you what happened: loan defaults rose 12% last quarter. Diagnostic analytics explains why: borrowers in a specific income band were most affected. Predictive analytics forecasts what will happen next: which borrowers are likely to default in the next 90 days. Prescriptive analytics goes one step further — recommending what to do about it.

Understanding these distinctions matters because each type shapes a different kind of decision. Predictive and prescriptive analytics are where banks move from reporting the past to acting on the future.

How It Works in Practice

The process follows three steps:

- Data collection — pulling from core banking systems, credit bureaus, GST records, payment histories, mobile behaviour, and third-party sources

- Model training — algorithms identify patterns in historical data (for example, what transaction sequences preceded past fraud events)

- Prediction output — the model flags a likely loan default, scores a transaction as high-risk, or identifies a customer showing early churn signals

Banks use all four analytics types. But predictive and prescriptive analytics are where institutions gain genuine foresight — moving from reactive reporting to decisions made before problems materialise.

Top Use Cases of Predictive Analytics in Banking

Predictive analytics is being embedded across virtually every banking function. The following use cases represent areas where institutions are already seeing measurable returns.

Fraud Detection and Prevention

ML models assign real-time risk scores to every transaction by analysing location, device, time, transaction amount, and historical behaviour. When a pattern deviates from a customer's established baseline — a large withdrawal from an unusual location, for instance — the model flags or blocks it instantly.

The critical advantage over traditional rule-based systems is false positive reduction. Rules block anything that matches a threshold; ML distinguishes between a genuine anomaly and a customer who simply travelled abroad. Global payment card fraud losses reached USD 33.83 billion in 2023 — and the gap between rule-based and ML-powered detection directly determines how much of that exposure a bank absorbs. At Krungsri Consumer, SAS-powered ML models reduced alert volume by 40%, improved fraud detection by 35%, and cut false positives by 18% — a combination that protects revenue without degrading customer experience.

Credit Risk Assessment and Loan Processing

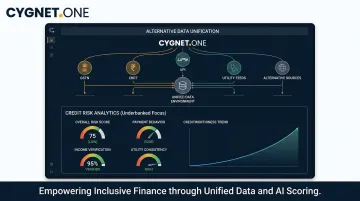

Traditional FICO scoring captures credit history. Predictive models go further — incorporating transaction behaviour, income patterns, GST filing history, UPI payment records, and utility payments to build a fuller picture of creditworthiness.

For thin-file borrowers, this is where the model earns its keep. A World Bank study found that alternative data — telco billing, utility payments, rental history — can improve credit model predictive power by 5% to 20%. Rental data alone made 9% of previously credit-invisible US consumers scorable.

In India, where more than 160 million consumers were credit underserved as of 2021, these capabilities have direct commercial implications for NBFCs looking to expand their lending portfolio responsibly.

Automated credit assessment also dramatically accelerates turnaround time. In one documented engagement, a Fincorp using Cygnet.One's Cygnet Finalyze platform reduced loan processing turnaround time by 80% — ageing reports that previously took 4–5 days were generated in seconds, with automated internal credit scoring across financial health, organisational structure, and operational parameters.

Customer Churn Prevention and Personalisation

Banks can detect churn signals weeks before a customer leaves: reduced app engagement, declining deposit balances, a shift in spending toward a competitor's card. Predictive models surface these patterns and trigger personalised retention interventions — a timely rate offer, a fee waiver, a relevant product recommendation.

According to Harvard Business Review, acquiring a new customer costs 5 to 25 times more than retaining an existing one. Despite this, McKinsey found that only 8% of banks can apply predictive insights from ML models to live campaigns — suggesting significant headroom for most institutions.

Regulatory Compliance and AML Monitoring

Threshold-based AML systems generate high volumes of alerts, most of which are false positives requiring expensive manual review. Predictive models — using clustering, neural networks, and logistic regression — scan millions of transactions and surface patterns consistent with structuring, layering, or other suspicious behaviour that rule-based systems routinely miss.

The scale justifies the investment:

- Financial crime compliance costs USD 61 billion annually for US and Canadian institutions alone

- 85% of FATF survey respondents identified AML/CFT effectiveness as the primary benefit of new detection technologies

- Predictive monitoring shifts compliance from reactive auditing to proactive risk identification

Liquidity, Cash Flow, and Cross-Selling

Two additional use cases demonstrate how predictive analytics extends beyond risk management into revenue generation.

Liquidity Forecasting

Predictive models stress-test cash flow across multiple macroeconomic scenarios — incorporating seasonal patterns, corporate payment cycles, and interest rate movements. Institutions can optimise capital reserves proactively rather than reacting to shortfalls. The same models also support advisory services for corporate clients managing working capital cycles.

Precision Cross-Selling

Cross-selling improves significantly when driven by life-event signals: a new payroll deposit suggesting a job change, increased savings activity, or category shifts in spending. McKinsey reports that experience-led growth in banking delivers 15% to 20% higher sales conversion rates, and personalisation drives revenue lifts of 10% to 15% on average. Generic campaign targeting rarely approaches these numbers.

Key Business Benefits for Banks and NBFCs

For banks and NBFCs, predictive analytics creates measurable impact — not just in risk management, but across revenue, operations, and long-term decision-making.

Financial benefits:

- Fraud loss reduction through better detection and fewer false positives

- Improved loan portfolio quality via more accurate credit decisioning

- Lower customer acquisition costs from proactive retention

- Higher revenue per customer through better-timed, more relevant cross-selling

Operational benefits for NBFCs and mid-size lenders:

- Faster credit decisions with less manual underwriting effort

- Ability to assess creditworthiness for underbanked borrowers using GST, UPI, utility, and e-commerce data

- Improved collections prioritisation based on default probability scoring

- Reduced data discrepancies through centralised, automated data processing

Cygnet.One's analytics platform connects to GSTN, CBDT (ITR), MCA, digital payment, and utility data sources to enable risk-optimised decisions for borrowers who lack conventional credit trails — addressing a gap that standard bureau-based models cannot fill.

Beyond daily operations, the strategic value lies in timing. Predictive analytics replaces lagging indicators — last quarter's NPAs, last month's fraud losses — with leading indicators that give leadership time to act before problems compound. That shift opens up better options in product development, risk calibration, and competitive positioning.

Implementation Challenges Banks Face

Data Quality and Silos

Most banks store customer data across disconnected systems — credit cards in one platform, mortgages in another, savings in a third. Predictive models trained on fragmented data produce fragmented predictions. Deloitte's 2024 Banking Data and Analytics Survey found that more than 90% of bank data users reported a data-related challenge, with data quality issues consistently ranked among the top obstacles.

The foundational requirement is a unified, clean data layer before deploying advanced models. This isn't a technology problem — it's an organizational one that requires deliberate data governance.

Legacy Integration and Regulatory Explainability

Plugging modern AI into decades-old core banking infrastructure requires modular APIs and phased integration strategies. That's a solvable engineering problem. The harder challenge is explainability.

The CFPB has confirmed that creditors using AI for credit decisions must provide specific reasons for adverse outcomes — there is no regulatory exemption for algorithmic decisions. The EBA has similarly highlighted regulatory treatment of ML in credit risk models. This creates direct tension with complex ensemble models or neural networks that can't be easily interpreted.

When evaluating vendors, banks should look for:

- Transparent model architectures that explain decision logic

- Complete audit trails for every model action

- Documentation written to satisfy regulatory review

- Clear adverse-action reason codes for credit decisions

Customer Trust and Data Ethics

Predictive personalization cuts both ways. A timely mortgage offer feels helpful; one that signals the bank knows about a life event the customer hasn't shared feels invasive. Successful institutions pair predictive capabilities with transparent data use policies and give customers meaningful control over how their information is used.

That risk extends beyond the individual customer. The World Bank flags this directly in the context of alternative credit data: borrower information can reveal details about third parties who never consented to share their data, creating "silent party" risks that institutions need to actively manage.

How to Evaluate Predictive Analytics Vendors: A Practical Guide

For banking and NBFC leaders moving from exploration to vendor selection, these five criteria separate platforms built for financial services from generic analytics tools.

Data Integration Depth

The vendor must connect to your existing core banking systems, ERP platforms, and third-party data sources without requiring a full infrastructure overhaul. Ask specifically about:

- Pre-built connectors for your core system (SAP, Oracle, Dynamics, or proprietary)

- API flexibility for custom data sources

- Experience with banking-grade data environments, including regulatory data feeds

Cygnet.One's platform supports integrations across SAP, Oracle, Microsoft Dynamics, and Tally, with documented connections to GSTN, CBDT, MCA, UPI, and utility data sources — reducing integration risk for institutions that need alternative data ingestion at the outset.

Real-Time Processing and Scalability

Fraud detection and AML monitoring require transaction-level scoring in milliseconds, not end-of-day batch processing. Confirm:

- Whether the platform analyses transactions in real time or in batch cycles

- What uptime SLAs are guaranteed during transaction volume spikes

- Infrastructure specifications for high-load scenarios

Cygnet.One's infrastructure has demonstrated 99.99% uptime in deployment and provides visibility into a transaction pipeline exceeding 1 billion transactions worth INR 5,000+ crore monthly through its e-invoice and financial data platforms.

Model Transparency and Regulatory Compliance

For credit decisions and AML monitoring, model explainability is not optional — it's a regulatory requirement in multiple jurisdictions. Evaluate:

- Whether the vendor provides model documentation regulators can review

- Availability of audit trails for every decision

- Compliance with SOC 2 Type II, ISO 27001, and applicable data privacy standards

Cygnet.One holds SOC 2 Type II and CMMI Level 5 certifications — a relevant credential set for institutions operating across India, the UK, UAE, and the Middle East.

Domain Specialisation and Implementation Track Record

A generic analytics platform is not the same as one built with banking and NBFC workflows in mind. Ask vendors for:

- Evidence of measurable outcomes from comparable deployments (loan TAT reduction, fraud loss rates, NPA improvement)

- Depth of coverage across credit assessment, collections prioritisation, and compliance use cases

- Named or anonymised case studies from institutions of comparable size and complexity

Support, Customisation, and Total Cost of Ownership

Licensing fees are rarely the full story. Evaluate:

- Whether the vendor provides ongoing model tuning as data patterns shift

- Availability of 24×7 support for production environments

- Ability to customise models for your specific lending or compliance workflows

- Total cost including integration, training, and maintenance — not just the annual license

Cygnet.One offers 24×7 support with model customisation capabilities tailored to lending and compliance workflows — and its deployment track record includes an 80% reduction in loan processing turnaround time for a leading Indian NBFC.

Frequently Asked Questions

What is predictive analytics in banking?

Predictive analytics in banking uses AI, machine learning, and statistical models to analyze historical and real-time data (transactions, credit histories, customer behavior) to forecast future outcomes like loan defaults, fraud events, or customer churn. It enables banks to act before problems materialize rather than responding after the fact.

What are the 4 types of analytics?

The four types are descriptive (what happened), diagnostic (why it happened), predictive (what will happen), and prescriptive (what should be done about it). Banks use all four, but predictive and prescriptive analytics drive the most strategic value in risk management and customer experience.

What are the main use cases of predictive analytics in banking?

The primary use cases are fraud detection, credit risk assessment, customer churn prevention, AML and compliance monitoring, liquidity forecasting, and cross-selling. Most banks start with fraud or credit risk before expanding into personalization and revenue use cases.

How does predictive analytics improve credit risk management?

Predictive models go beyond traditional credit scores by incorporating transaction behavior, income patterns, GST data, and alternative data sources. This enables faster, more accurate lending decisions, lower default rates, and credit access for borrowers who lack conventional credit histories.

What challenges do banks face when implementing predictive analytics?

The three primary challenges are fragmented data across legacy systems (which makes model training incomplete), integrating modern AI with existing core banking infrastructure, and maintaining model explainability. That last point is especially critical for satisfying regulatory requirements around adverse action notices and AML audit trails.

What should banks look for when choosing a predictive analytics vendor?

Key criteria to evaluate:

- Depth of banking domain expertise

- Real-time processing capability

- Model transparency and regulatory compliance support

- Integration track record with core banking and ERP systems

- Documented outcomes from comparable deployments, not just feature lists