Enterprise tax has a data problem. The information tax teams need (transaction records, entity data, intercompany flows, jurisdiction-specific rates) sits across ERP systems, billing platforms, and spreadsheets that do not communicate.

The result is a tax function that is always catching up, with planning and risk monitoring relegated to whatever capacity remains after the period close. The pressure on the function is also climbing. Real-time reporting mandates, e-invoicing rollouts, and tax authorities deploying machine learning to flag audit targets are reshaping what good looks like for enterprise tax.

The teams that get ahead are the ones turning their tax data into a queryable, monitored asset rather than a quarterly assembly project. The ones that wait keep paying the catch-up tax in audit risk and missed planning opportunities.

The 2025 Deloitte Tax Transformation Trends Report found that 86% of tax leaders outsourced or automated at least part of the tax function, which means the analytics maturity bar against which every enterprise tax function gets benchmarked has already moved. Tax data analytics is the discipline that makes the shift possible, turning fragmented systems into a queryable, monitored asset.

This guide explains what tax data analytics covers, why it matters for enterprise tax now, how it works inside the tax function, what visibility it produces, and how the discipline matures from spreadsheets to AI-enabled tax.

What Is Tax Data Analytics?

Tax data analytics is the practice of collecting, unifying, and analysing tax-relevant data across an enterprise to improve compliance accuracy, surface risk, and support strategic tax decisions. The discipline combines transaction-level data from ERP, billing, HR, and treasury systems with external reference data on jurisdiction rates and regulatory rules, then applies tax logic to surface position, risk, and planning insights.

Outputs serve compliance teams preparing filings, planning teams modelling deals, and tax leadership reporting to the CFO and audit committee. Mature tax data analytics is continuous rather than periodic, embedded into business decisions at the point they are made, and audited against the same data that the tax authority can query.

Tax Data Analytics Vs Regular Tax Reporting

Regular tax reporting answers a narrow set of questions about what is owed and when. The work is backwards-looking, periodic, and produces outputs for external consumption like returns, filings, and statutory disclosures. The reporting cycle ends at submission.

Tax data analytics covers a broader brief, examining patterns across transactions, entities, and periods to answer questions like where exposure is growing, which jurisdictions carry the most risk, and what the effective rate looks like if a particular deal closes. The output supports both compliance and decision-making across the year rather than only at filing time.

Data Sources That Feed Tax Data Analytics

Tax data analytics draws from multiple systems across the enterprise:

- ERP platforms like SAP, Oracle, and Microsoft Dynamics for transaction-level data

- Billing and order-management systems for invoice-level detail

- HR and payroll systems for employment-tax data

- Treasury systems for transfer-pricing flows

- External reference data, such as jurisdiction rate tables and regulatory feeds

The breadth of sources is what makes the unification layer the central engineering challenge, since each source has its own schema, refresh cadence, and ownership question.

Why Does Tax Data Analytics Matter For Enterprise Tax Now?

Three forces have shifted tax data analytics from a multinational nice-to-have to an enterprise-grade priority:

- Tax authorities are digitising filing and audit at speed

- Compliance windows are shrinking from quarterly to near real-time

- Analytics tools available to tax teams are catching up with what authorities themselves are deploying

The pressure shows up at scale, particularly because manual tax determination fails at high-volume, multi-country transactions where spreadsheet-based logic cannot keep pace with the change cadence.

Real-Time Reporting Mandates

Tax authorities in an increasing number of jurisdictions, including the EU, Latin America, and parts of Asia-Pacific, now require transaction-level data to be reported in near real-time. SAF-T, MTD in the UK, and similar regimes mean tax data must be clean, structured, and accessible on demand. Organisations without analytics infrastructure are exposed every reporting cycle, with little room to reconstruct evidence after submission.

AI-Readiness Of Tax Authorities

Tax authorities are deploying machine learning to detect anomalies, flag inconsistencies, and identify audit targets. The OECD’s Forum on Tax Administration has documented this shift across member countries. When the authority analysing the filing is running AI, the enterprise tax team needs equivalent visibility into its own data to anticipate what the model will surface.

E-Invoicing Rollout

Mandatory e-invoicing, now live or in rollout across the EU, India, Saudi Arabia, and other markets, means transaction data flows directly to tax authorities at the point of invoice. There is no opportunity to correct errors after the fact. Analytics capability is what lets tax teams monitor data quality before it leaves the business, with reconciliation and exception logic running on the same dataset that the authority will receive.

Audit Risk And The Analytics Case

Audit selection is increasingly data-driven. Authorities cross-reference VAT reclaims against supplier filings, compare effective rates against industry benchmarks, and flag outliers automatically. Tax data analytics gives enterprise teams the ability to run the same checks internally, finding discrepancies before they become audit triggers.

The 2024 IBM Cost of a Data Breach Report found that the global average cost of a breach reached USD 4.88 million in 2024, with regulatory penalties and remediation work amplifying the total figure, which is the order-of-magnitude exposure analytics is built to compress.

How Does Tax Data Analytics Work Inside The Tax Function?

Tax data analytics operates as a pipeline that runs in three layers:

- Data sources (raw data flowing in from across the enterprise)

- Data unification (cleaning and reconciling sources into a single dataset)

- Analytics (applying tax logic to surface position, risk, and planning insights)

Each layer has its own tooling, its own ownership questions, and its own failure modes. The output, the consumers, and the cadence depend on how mature the operating model behind the pipeline is, which is where tax governance frameworks for enterprises shape the work as much as the platform does.

Data Sources

The process starts with raw data from across the enterprise: transactional data from ERP and billing systems, entity and structural data from legal and finance, payroll data for employment tax, and external reference data like jurisdiction rate tables.

Volume is high, and formats are inconsistent across these sources. Refresh cadence varies from real-time billing flows to monthly HR snapshots to annual regulatory feeds, and the pipeline has to absorb all three without losing reconciliation.

Data Unification Layer

Before any analysis can happen, data must be extracted, cleaned, and normalised. This is typically handled through ETL pipelines, a tax data warehouse, or a purpose-built tax data platform. The goal is a single reconciled dataset where transactions map correctly to entities, jurisdictions, and tax types, and where discrepancies are surfaced rather than buried.

The 2026 Gartner Forecast on Embedded AI in Cloud ERP found that 62% of cloud ERP spending will be on AI-enabled solutions by 2027, up from 14% in 2024, which signals how quickly the unification layer will absorb AI-assisted reconciliation, anomaly tagging, and automated lineage tracking.

Analytics Layer

With clean, unified data in place, analytics tools apply tax logic to surface insights across four common output types:

- Dashboards for tax position monitoring

- Exception reporting to flag anomalies

- Scenario modelling for planning

- Reconciliation tooling for compliance

Platforms like Alteryx, Power BI, Tableau, and purpose-built tax analytics tools operate at this layer, sitting on top of the unified dataset rather than re-extracting from source systems for every analysis.

Output Consumers and Use Patterns

The outputs serve different users in different ways:

- Tax compliance teams use exception reports and reconciliation outputs to prepare accurate filings

- Tax planning teams use scenario models and effective-rate analysis to support decisions

- Tax leadership uses dashboards to report position and risk to CFOs and audit committees

The same underlying dataset serves all three. The layer that changes is how the data is sliced, aggregated, and presented for the consumer’s question.

What Does Tax Data Analytics Give You Visibility Into?

Once the analytics pipeline is running, the visibility it produces splits into three categories that drive different decisions across the tax function: position, risk, and planning. Each one shifts how tax interacts with finance, the business, and the board.

For jurisdictions where indirect tax sits at the centre of the operating model (such as GST in India), the visibility also extends into broader GST business intelligence that turns granular tax data into actionable insights for finance, lending, and operational leaders.

Visibility Into Tax Position

Analytics gives tax leaders a current, consolidated view of the organisation’s tax position: effective rates by jurisdiction, outstanding liabilities, deferred tax balances, and filing status across entities. Instead of assembling the view manually at quarter-end, it is available on demand.

This changes how tax leaders communicate with finance and the board, since the conversation moves from explaining the lag to defending the position.

Early Visibility Into Tax Risk

Analytics surfaces the signals that precede risk: unusually high reclaim rates, transaction patterns that deviate from historical norms, and jurisdictions where the effective rate is drifting. These are the same signals that drive audit selection. Seeing them internally, before a filing goes out or a notice arrives, gives the tax team time to investigate and correct rather than respond.

Visibility Into Planning Opportunities

Tax data analytics also creates the foundation for proactive planning. When the team can see the effective rate at the entity level, model the impact of a restructure, or identify where withholding-tax exposure is building, planning becomes data-driven rather than assumption-driven.

Tax planning judgment remains central, with analytics changing the inputs that judgment runs on rather than replacing the judgment itself.

How Does Enterprise Tax Data Analytics Mature?

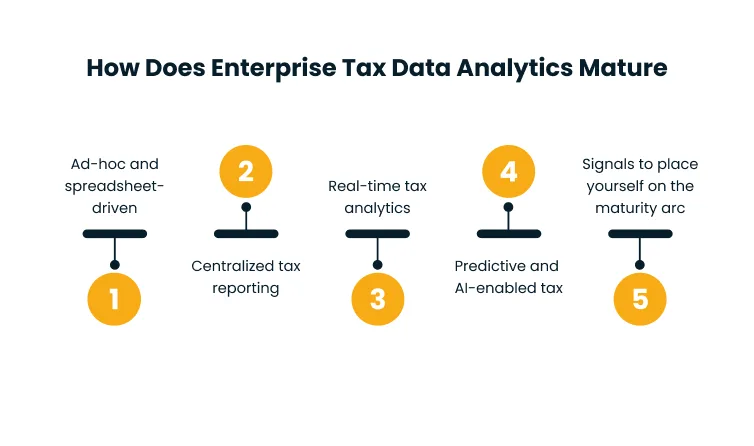

Most enterprise tax functions sit somewhere on a four-stage maturity arc, with the stage being a function of both the underlying data architecture and how the team uses the outputs. Knowing where you sit on the arc is the prerequisite for deciding what to invest in next, since the right next step is usually one stage forward rather than a leap to the top.

Stage 1: Ad-Hoc And Spreadsheet-Driven

Most organisations start at this stage, with tax data living in spreadsheets, assembled manually for each filing cycle, and not systematically reused or analysed. Insight is limited to what an individual analyst can produce in a given week. Risk monitoring is reactive, and planning depends on rebuilding the dataset every time the question changes.

Stage 2: Centralised Tax Reporting

The organisation moves data into a shared environment, such as a tax data warehouse or a centralised reporting tool. Reporting becomes more consistent and repeatable, with the tax team no longer rebuilding the same dataset from scratch each period. Analysis is still largely backwards-looking and periodic, though the foundation for higher-stage maturity is in place.

Stage 3: Real-Time Tax Analytics

At this stage, data pipelines feed tax dashboards continuously rather than periodically. Tax teams can monitor positions between filing cycles, run exception reports on demand, and flag data quality issues before they reach a filing.

Integration with ERP and billing systems is tight, often anchored on a Unified Tax Data Lake that consolidates ERP, billing, HR, and treasury feeds into a single queryable dataset. This is where most enterprise tax functions are currently trying to get to, and where real-time reporting and e-invoicing mandates push the architecture without ambiguity.

Stage 4: Predictive And AI-Enabled Tax

The leading edge of tax analytics applies machine learning to forecast liabilities, predict audit risk, and model the tax impact of business decisions before they are made. Analytics is embedded into business processes, with tax input available at the point of a contract decision, a supply-chain change, or an M&A transaction.

The 2025 Deloitte AI-Enabled Tax Transformation Report found that 84% of respondents used AI heavily in the tax function, up from 47% the prior year, with 87% of CFOs expecting AI to be extremely or very important to finance operations in 2026. Few organisations are fully at Stage 4, with the trajectory of that adoption curve making it the planning horizon rather than the destination.

Signals To Place Yourself On The Maturity Arc

Three signals usually fix the stage with little ambiguity:

- Where the tax dataset lives, ranging from spreadsheets at Stage 1, to a shared reporting tool at Stage 2, to a continuous pipeline at Stage 3, to a model-integrated platform at Stage 4

- The cadence of refresh, from monthly or quarterly assembly at Stages 1-2, to continuous refresh at Stage 3, to predictive model output at Stage 4

- Who consumes the output, from the tax team only at Stages 1-2, to tax plus finance at Stage 3, to tax plus business decision-makers at the point of action at Stage 4

The stage with the most signals is the one to plan from.

Conclusion

Tax data analytics is no longer a capability reserved for the largest multinationals with dedicated data teams. Regulatory pressure, authority sophistication, and the availability of modern tooling have made it a practical priority for any enterprise tax function that wants to reduce risk and operate proactively.

The teams that move first treat the analytics layer as an operating capability rather than a one-off project. They name an owner, define the data sources and unification pattern, set the cadence for refresh and review, and pressure-test the outputs against the same questions a tax authority would ask. The teams that wait are the ones still assembling each filing from scratch when the next real-time reporting mandate lands in their jurisdiction.

The maturity arc is short for organisations that start now, with the catch-up project growing larger the longer the wait. Book a demo with Cygnet.One to walk through where your tax data analytics maturity sits today and what the next stage looks like for your team in operational terms.

FAQs

Tax data analytics focuses on collecting, unifying, and analysing tax-relevant data to surface position, risk, and planning insights. Tax automation executes tax processes like calculation, filing, and e-invoicing submission using rule-based engines. Mature enterprise tax functions usually need both: automation runs the workflow, and analytics monitors it.

Tax data analytics typically combines ETL pipelines and tax data warehouses for the unification layer with BI tools like Power BI, Tableau, and Alteryx for analytics. ERP-native tax modules from SAP, Oracle, and Microsoft Dynamics supply transactional data, with Snowflake or Databricks added for high-volume cross-jurisdictional stacks.

ROI typically shows up in three places: reduced audit risk and penalty exposure from earlier anomaly detection, faster compliance cycles under real-time and e-invoicing mandates, and improved planning quality from data-driven scenario modelling. Most enterprise teams see the case land within twelve to eighteen months.

Three challenges dominate: data fragmentation across ERP, billing, HR, and treasury systems, cross-functional governance to align finance, IT, and tax on definitions and ownership, and the skills gap between tax professionals and data engineering depth. Tooling is the easiest part, with the operating model where most programmes stall.

A capable team blends tax-domain expertise across compliance, planning, transfer pricing, and indirect tax with data engineering for the unification layer and BI skills for surfacing insights. Some teams add machine learning for predictive use cases. Most enterprises hire across the mix rather than expecting one person to cover all three.

Tax authorities increasingly run machine learning across e-invoicing feeds, real-time reporting submissions, and historical filings to flag anomalies, cross-reference VAT reclaims, compare effective rates against benchmarks, and prioritise audit targets. Authorities that analyse filings with AI expect the enterprise to have equivalent visibility into its own data.

Author

Abhishek Nandan

AVP, Marketing

Abhishek Nandan is the AVP of Services Marketing at Cygnet.One, where he drives global marketing strategy and execution. With nearly a decade of experience across growth hacking, digital, and performance marketing, he has built high-impact teams, delivered measurable pipeline growth, and strengthened partner ecosystems. Abhishek is known for his data-driven approach, deep expertise in marketing automation, and passion for mentoring the next generation of marketers.