Tax errors rarely begin with the tax return. They begin earlier, in the quiet distance between a sales invoice, a ledger posting, a tax engine rule, a credit note, and the final compliance file. By the time the tax team sees the number, the damage may have already travelled through three systems.

That is why Tax data reconciliation has moved from a back-office task into a tax control through tax assurance services. Tax teams now defend numbers that pass through ERP, billing tools, procurement systems, tax engines, warehouses, spreadsheets, and statutory portals. One mismatch can distort input credit, output tax, withholding, jurisdictional reporting, and audit responses.

The older model was simple: finance closes the books, tax adjusts the data, compliance gets filed. That model is weak for 2026. Regulators receive faster, system-generated data. Enterprises need Tax data management built into the data path itself to improve tax compliance data accuracy.

Why Tax Reconciliation Is Now a Control Issue

Reconciliation is often treated as clean-up. In practice, it is evidence. It proves whether the tax number in the return can be traced back to the commercial event that created it.

A tax leader should be able to answer four questions without asking five teams for screenshots:

- Which source created this tax value?

- Was it changed after posting?

- Which rule or master data field drove the treatment?

- Why does the filing differ from the ERP report?

If these answers are slow, risk is already present.

Tax data reconciliation gives the tax team a repeatable way to compare records, find timing gaps, explain exceptions, and retain the trail. For enterprises, this is no longer about matching totals. It is about proving that each transaction moved correctly through its compliance path.

This is where financial reconciliation tax work differs from standard finance reconciliation. Finance may accept a timing difference if the books remain correct. Tax teams need a sharper view because timing, jurisdiction, place of supply, tax code, exemption status, and document validity can change the compliance outcome.

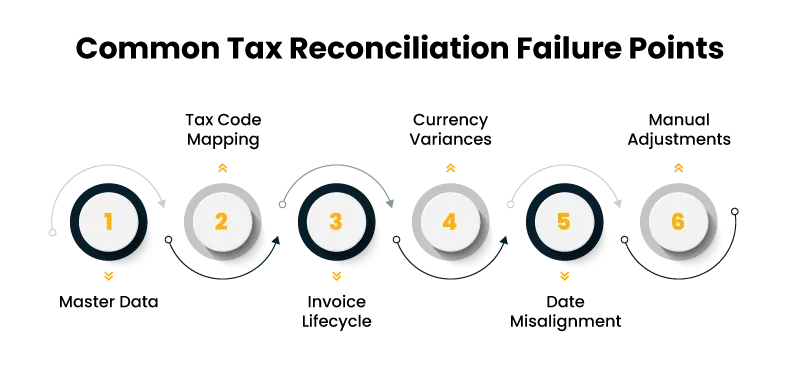

Where Tax Data Breaks Between ERP, Tax Engines, and Portals

The most common failure is not a system crash. It is a small difference that looks harmless until it repeats.

| Mismatch area | What usually happens | Tax risk created |

| Master data | Tax ID, legal name, or address differs across systems | Wrong tax treatment or credit denial |

| Tax code mapping | ERP code does not match tax engine logic | Incorrect rate, exemption, or place of supply |

| Invoice lifecycle | Invoice, amendment, credit note, and cancellation move at different times | Duplicate reporting or missing adjustment |

| Currency conversion and precision variances | ERP, tax engine, and portal apply different conversion or decimal precision rules | Return values differ from books |

| Transaction date misalignment | Transaction date, tax point, and accounting date do not align | Period mismatch |

| Uncontrolled tax adjustments | Users modify tax values without documented justification | Weak audit trail |

The hard part is not finding one mismatch. It is deciding which mismatch matters, who owns it, how it gets corrected, and whether the same issue is recurring.

ERP vs tax system mismatch reconciliation should start with business rules, not spreadsheets. If the ERP is the book of record and the tax engine is the tax decision layer, the organization needs a defined rule for which system wins under each scenario. Without that rule, teams debate exceptions instead of resolving them.

The Reconciliation Need Across Modern Tax Operations

A mature tax team does not wait for filing week to test data. It checks the data as it moves.

For indirect tax, the reconciliation need often sits between sales register, purchase register, e-invoice data, e-way bill data, GST or VAT returns, and input credit statements. For direct tax, it may sit between ledger balances, fixed asset systems, payroll, withholding records, intercompany charges, and tax provision workpapers.

In both cases, financial reconciliation tax controls should confirm three things:

- Source records are complete.

- Tax values are calculated and posted correctly.

- Filed values can be traced to approved records.

This is where tax compliance data accuracy becomes measurable. It can be tested through match rates, unresolved exceptions, recurring root causes, late adjustments, manual override frequency, and reopened filings.

A useful metric is the first-pass tax match rate. It shows how many transactions clear reconciliation without human correction. If that number stays low, the tax team should not celebrate heroic filing effort. It should fix the upstream design.

Tax Data Reconciliation Techniques That Enterprise Teams Can Defend

Good reconciliation is layered. It should not rely on one grand report.

Tax data reconciliation techniques enterprise teams can adopt usually fall into five practical groups:

| Technique | Best use | What to watch |

| Field-level matching | Invoice number, tax ID, date, amount, tax code | Formatting differences can create false breaks |

| Rule-based tolerance checks | Decimal precision, currency conversion, and minor timing gaps | Tolerance must be approved by tax |

| Three-way matching | ERP, tax engine, statutory portal | Needs consistent document identifiers |

| Exception aging analysis | Unresolved breaks by days and value | Old low-value breaks may signal process failure |

| Root-cause tagging | Master data, rule logic, timing, user override | Tags must lead to ownership |

A practical approach is to classify exceptions before assigning work. Not every mismatch deserves the same urgency. A missing tax ID on a high-value vendor invoice needs different treatment from a minor precision variance on a low-value sale.

A simple hierarchy works well:

- Blocker: Filing or credit claim cannot proceed.

- High-risk: Filing can proceed only with tax approval.

- Operational: Correction needed, no immediate filing impact.

- Informational: Accepted difference with policy backing.

This structure prevents reconciliation from becoming an endless queue. It also helps tax, finance, IT, and shared services work from the same risk view.

Designing for Tax Compliance Data Accuracy Across Systems

Ensuring tax data accuracy multi systems requires design discipline. The tax team cannot inspect quality into data after the fact. It has to define controls before data reaches the return.

The first control is master data governance. Customer tax registrations, vendor classifications, item tax categories, exemption certificates, jurisdiction fields, and withholding indicators need clear ownership. If no one owns a field, the field will decay.

The second control is tax rule governance. Tax engines and ERP tax procedures often contain logic that only one specialist understands. Rules should have named owners, effective dates, change notes, test cases, and approval logs.

The third control is cross-system transaction traceability. Each invoice, credit note, debit note, journal, and adjustment needs a stable identifier across systems. If identifiers change between ERP, middleware, tax engine, and filing portal, reconciliation becomes guesswork.

The fourth control is exception feedback. When tax data reconciliation finds a recurring break, the fix should move upstream. Repeating the same correction every month is disguised rework.

This is the point where tax compliance data accuracy becomes an operating habit. It depends on how people create, move, correct, and approve data before the tax team files anything.

Reconciliation Tools for Tax: What Actually Matters

Many teams ask for automation before they define the process. That sequence creates expensive disappointment.

Reconciliation tools for tax can help only when supported by data engineering services that define source ownership, matching logic, exception categories, and close responsibilities.

The right tool should support six capabilities:

| Capability | Why it matters |

| Multi-source ingestion | Pulls data from ERP, tax engine, warehouse, portals, and files |

| Configurable matching logic | Allows tax-specific rules, not only accounting matches |

| Workflow routing | Sends exceptions to the right owner with status tracking |

| Audit trail | Records changes, approvals, comments, and evidence |

| Dashboards | Shows match rate, aging, value at risk, and root causes |

| Period controls | Prevents silent changes after closing or filing |

Reconciliation tools for tax should also handle partial matches. Tax data is rarely clean enough for exact matching across all fields. A good system can identify likely matches, show confidence, and keep human approval where judgment is needed.

The trap is buying a tool to hide process weakness. If master data is poor, tax rules are unclear, and ownership is scattered, software will only make the mess easier to view. The tool should reduce manual matching and expose the defects that create mismatches.

Governance That Stops Repeat Errors

Governance decides whether reconciliation improves the tax process or becomes another report nobody trusts.

The operating model should define:

- Data owners for each critical tax field.

- Rule owners for tax logic and rate changes.

- Exception owners for correction and approval.

- Close calendars for reconciliation checkpoints.

- Materiality thresholds approved by tax leadership.

- Evidence standards for audit and regulator review.

Financial reconciliation tax governance also needs independence. The person who creates or changes a tax-sensitive field should not be the only person approving the exception. For high-risk items, tax must retain final sign-off.

A monthly governance review should focus less on how many breaks were cleared and more on why they happened. If 40 percent of exceptions come from vendor master data, the answer is better vendor onboarding, validation, and periodic clean-up.

What Strong Outcomes Look Like

The strongest outcome is fewer late-stage surprises.

When tax data reconciliation works well, the tax team spends less time defending numbers and more time reviewing judgment areas. Finance gets fewer late tax adjustments. IT gets clearer change requests. Auditors get cleaner evidence. Business teams face fewer filing disruptions.

| Outcome | Business impact |

| Higher first-pass match rate | Less manual effort before filing |

| Lower unresolved exceptions | Faster close and fewer unresolved risks |

| Fewer post-filing adjustments | Cleaner statutory reporting |

| Stronger audit trail | Faster response to notices and reviews |

| Better root-cause visibility | Permanent fixes instead of repeated manual effort |

Tax compliance data accuracy also supports better forecasting. If the tax team trusts the data earlier, it can identify cash flow impact, credit risk, and provision issues before the reporting deadline. This matters because tax affects working capital, earnings quality, and management confidence.

Final thoughts: Accuracy Is Built Before the Return

Tax filings are only as reliable as the data path behind them. Once numbers reach the return, the tax team has limited room to fix the real issue. It can adjust, explain, or rework. It cannot rewrite weak upstream controls during filing week.

That is why tax data reconciliation deserves more attention from CFOs, tax heads, controllers, and technology leaders. It sits at the point where tax risk, data quality, system design, and governance meet.

For 2026, the serious question is no longer whether the organization can file on time. The sharper question is whether it can prove, transaction by transaction, that the filed number is complete, correct, and explainable. That proof starts with tax compliance data accuracy, disciplined financial reconciliation tax controls, and a reconciliation model built for the systems where tax data actually lives.

Author

Yogita Jain

Content Lead

Yogita Jain leads with storytelling and Insightful content that connects with the audiences. She’s the voice behind the brand’s digital presence, translating complex tech like cloud modernization and enterprise AI into narratives that spark interest and drive action. With a diverse of experience across IT and digital transformation, Yogita blends strategic thinking with editorial craft, shaping content that’s sharp, relevant, and grounded in real business outcomes. At Cygnet, she’s not just building content pipelines; she’s building conversations that matter to clients, partners, and decision-makers alike.