Tax risk now forms inside ordinary transactions: invoices, tax codes, vendor masters, customer exemptions, intercompany charges, payroll settings, and manual journals. By the time a quarterly review finds the error, the business may have already filed, reported, or repeated it across hundreds of records.

That is the case for continuous tax monitoring through tax assurance services. It moves tax control closer to the point where risk is created. Instead of waiting for a periodic audit to uncover patterns, tax teams watch live transaction behavior, route exceptions, and retain evidence while the issue is still fixable.

This shift is not theoretical. Tax administrations are digitizing. OECD work on digital tax administration points to tax processes being embedded into the systems taxpayers already use. E-invoicing and continuous transaction control programs are also pushing companies toward faster, cleaner reporting. For enterprise tax teams, the question is no longer whether more tax data will be inspected. The question is whether the company can inspect it first.

This blog explains what is continuous tax monitoring enterprise leaders should understand, why periodic audits are losing ground, how real time tax compliance works, where an automated tax audit fits, and what outcomes finance leaders can reasonably expect.

Why Periodic Tax Audits Find Problems Too Late

Traditional audits were built around review cycles. Close the books, pull samples, test controls, document gaps, assign remediation, and prepare for the next cycle. That model still has value, but it is too slow for tax risks created inside high-volume systems.

| Common audit finding | Why it appears late | Business impact |

| Incorrect tax code | Detected after invoice posting | Rework, credit notes, filing corrections |

| Missing exemption proof | Found during document sampling | Weak defense during assessment |

| Vendor classification error | Identified after procurement activity | Wrong withholding or indirect tax treatment |

| Manual override | Reviewed after close | Limited control evidence |

The weakness is timing. A sample-based review can confirm that a problem exists. It cannot stop the same error from spreading through similar transactions.

This is where an automated tax audit adds value. It tests full transaction populations against defined rules using data analytics consulting services. It does not replace tax judgment. It gives tax professionals earlier evidence, broader coverage, and a cleaner view of repeat issues.

A periodic audit asks, “What went wrong?” An automated tax audit asks, “What is going wrong now, where is it repeating, and who can correct it?”

What Real-Time Tax Compliance Means in Practice

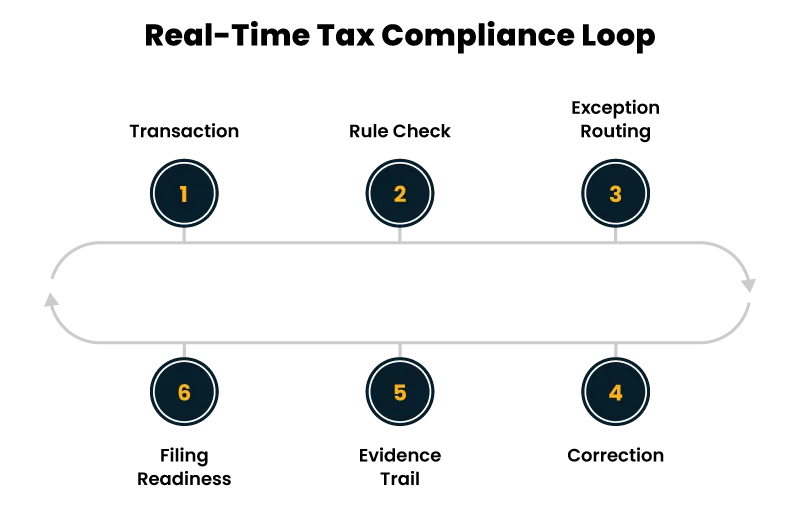

Real-time tax compliance is often described as faster reporting. That is too narrow. The better definition is transaction-level tax control with timely detection, assigned ownership, and audit-ready evidence.

In practical terms, real time tax compliance means:

- Tax-sensitive data is checked before posting or soon after posting.

- Exceptions are routed to the team that can fix the source issue.

- Decisions are recorded with timestamps, comments, and supporting documents.

- Tax teams can see risk by entity, process, rule, and filing period.

The important point is that many tax issues are operational. A wrong VAT, GST, sales tax, or withholding treatment may start with a missing field, outdated exemption certificate, incorrect ship-to location, or product category mapped to the wrong tax rule. If tax sees the issue only at filing time, the correction effort expands.

With monitoring, tax does not need to approve every transaction manually. Rules, thresholds, workflows, and evidence trails do much of the first-line work.

What Continuous Monitoring Should Watch

Good monitoring is specific. It focuses on risk signals that can be tested repeatedly.

| Monitoring area | Example control test |

| Tax code accuracy | Compare tax code with entity, product, place of supply, and customer type |

| Exemption handling | Flag expired, missing, or mismatched certificates |

| Vendor setup | Check tax registration, residency, withholding category, and duplicates |

| Intercompany flows | Identify missing agreements, incorrect rates, or unsupported charges |

| Manual postings | Detect tax-impacting journals outside approved workflow |

| Filing readiness | Reconcile transaction data with return preparation logic |

This is where real time compliance tools tax teams use must go beyond dashboards. A chart that turns red after closing is only a delayed warning. A useful tool detects the issue, explains the reason, assigns the owner, tracks closure, and stores evidence.

That closed loop is the difference between reporting and control.

Automated Audit Systems Need Rules Before Dashboards

An automated tax audit works best when rules are tied to real exposure. Starting with visualization is tempting, but it often creates noise. Start with the risks that already hurt the business: audit adjustments, filing corrections, notices, late reconciliations, and manual review bottlenecks.

| Risk | Rule | Owner | Action |

| Wrong tax code on domestic sale | Tax code must match customer location and product category | Tax operations | Correct before filing |

| Expired exemption certificate | Certificate date must be valid on invoice date | Billing or credit team | Request updated proof |

| Manual tax journal | Tax-impacting journal above threshold needs approval | Controller | Review and document |

| Vendor residency gap | Residency field must be complete before payment | Procurement | Update master data |

For enterprise programs, automated audit systems enterprise tax teams deploy should act as control infrastructure. They should connect ERP data, tax engines, workflow tools, and evidence repositories.

The second use of automated audit systems enterprise tax is pattern detection. One exception may be a mistake. A cluster from one country, business unit, product line, or vendor group may show a broken process. That is where tax becomes more useful to finance leadership.

Technology Tools That Support Continuous Tax Monitoring

The toolset does not need to be complex. It needs to be connected, explainable, and governed.

| Layer | Purpose | What to check |

| ERP and source systems | Capture transaction data | Can tax fields be extracted cleanly? |

| Tax engine | Apply tax logic | Are rules maintained centrally? |

| Data quality layer | Validate completeness and consistency | Are exceptions traceable to source records? |

| Workflow system | Route and close issues | Is ownership clear? |

| Evidence repository | Store proof | Can users retrieve decisions by period, entity, and rule? |

| Analytics layer | Show patterns | Does it explain the reason behind each exception? |

For organizations evaluating what is continuous tax monitoring enterprise programs, the more important question is not which dashboard looks better. It is whether the system helps reduce tax risk at the source or merely documents it more efficiently.

A tool cannot repair unclear ownership. If procurement owns vendor tax data, procurement must close vendor exceptions. If billing owns exemption data, billing must fix certificate gaps. Tax defines risk and reviews’ impact, but it should not become the cleanup desk for every upstream defect.

Benefits Finance Leaders Can Defend

The strongest case for continuous tax monitoring is fewer late surprises. The tax compliance automation benefits usually appear in four areas.

First, teams reduce rework because errors caught before filing cost less to correct. Second, controls become easier to prove because each exception has a timestamp, owner, decision, and closure trail. Third, tax teams spend less time collecting evidence. Fourth, leaders get a clearer view of where risk starts.

The tax compliance automation benefits should be measured against a baseline. Track current audit adjustments, return corrections, tax notice themes, close delays, and manual review hours before implementation. After go-live, compare the same metrics.

| KPI | What it tells leadership |

| Exception volume by rule | Which control creates the most noise or risk |

| Repeat exceptions by source | Which process needs correction |

| Average closure time | Whether ownership is working |

| Filing adjustments avoided | Whether monitoring prevents late corrections |

| Manual review hours reduced | Whether capacity is moving to higher-value work |

Do not measure everything. Pick metrics that change decisions.

How to Implement Without Creating Alert Fatigue

The weakest projects try to monitor every tax field on day one. That creates fatigue. Users stop trusting alerts. Tax then returns to spreadsheets because the official system produces too much noise.

Start with five to ten rules tied to known exposure. Include one control linked to statutory filing, one linked to master data, one linked to manual postings, and one linked to past audit pain.

A practical sequence:

- Identify recurring exceptions from the last four to six reporting cycles.

- Rank them by financial exposure, frequency, and correction effort.

- Define rule logic in plain language before tool configuration.

- Test each rule against historical data to check false positives.

- Assign business ownership, not only tax ownership.

- Review alert quality every month until noise drops.

This is how real-time tax compliance becomes operational. It starts with fewer rules, better ownership, and cleaner evidence.

Making It Work Across Multiple Entities

Multi-entity businesses need consistency without forcing one rule onto every jurisdiction. A tax code pattern that is normal in one country may be wrong in another. A certificate requirement may exist in one region and have no relevance in another.

A workable model uses a global control spine with local rule variants.

| Control element | Global standard | Local variant |

| Tax code validation | Tax code must match transaction facts | Country-specific rates and reporting codes |

| Master data completeness | Required tax fields must be populated | Local registration and documentation rules |

| Manual override review | Override must be approved and documented | Thresholds based on local risk |

| Evidence retention | Decision trail must be stored | Retention period and format by jurisdiction |

This structure keeps governance consistent while preserving local accuracy. It also makes real time compliance tools tax programs easier to maintain because teams know which rules are global and which are local.

What Better Outcomes Look Like

A mature continuous tax monitoring model changes the tax conversation.

Instead of defending late corrections, tax can show prevented errors. Instead of explaining audit findings after damage is done, it can show recurring defects and remediation. Instead of asking for more people during closing, it can show where automation has reduced manual review.

An automated tax audit also helps internal audit and external reviewers. They can see full-population testing, rule history, exception closure, and evidence quality. Sampling still has a role, but it starts from a stronger base.

For leadership, the outcome is practical: quieter close cycles, fewer preventable notices, cleaner evidence, earlier visibility into process weakness, and better real time tax compliance maturity across entities.

Final thoughts: Audit Should Become a Safety Net

Periodic audits still have a place in modern tax governance. They help verify controls and identify systemic weaknesses. The limitation is timing. When an issue is identified months after the underlying transaction occurred, the organization often faces a larger correction effort and a longer evidence-gathering exercise.

Continuous tax monitoring gives tax teams a timing advantage. Real-time tax compliance makes that advantage visible in daily operations. An automated tax audit makes the control model repeatable.

The value is not speed alone. It is confidence before filing, evidence before review, and correction before exposure hardens into liability.

Companies that treat monitoring as another reporting layer will get limited value. Companies that connect rules, ownership, workflow, and evidence will build a tax control model suited to digital tax administration and enterprise complexity. That is where real time tax compliance and an automated tax audit start to feel less like technology projects and more like tax discipline finally catching up with the business.

Author

Yogita Jain

Content Lead

Yogita Jain leads with storytelling and Insightful content that connects with the audiences. She’s the voice behind the brand’s digital presence, translating complex tech like cloud modernization and enterprise AI into narratives that spark interest and drive action. With a diverse of experience across IT and digital transformation, Yogita blends strategic thinking with editorial craft, shaping content that’s sharp, relevant, and grounded in real business outcomes. At Cygnet, she’s not just building content pipelines; she’s building conversations that matter to clients, partners, and decision-makers alike.