Introduction

E-invoicing in Nigeria is described as the computerized creation, authentication, and submission of invoice information to tax agencies, mainly instigated by the Federal Inland Revenue Service (FIRS).

In contrast to PEPPOL-based markets, like Australia and New Zealand, Nigeria is progressing towards a Continuous Transaction Controls (CTC) model, in which invoice data is validated or reported to the tax authority in almost real-time. E-invoicing in Nigeria is not only related to sending invoices, but also to reporting them to the tax authority to comply.

Businesses can simplify compliance using a CTC-ready e-invoicing platform that integrates directly with ERP systems

What Makes Nigeria Different from Other Countries

| Actor | Role | Action | Key Detail |

| Seller | Invoice creator | Creates invoice in ERP or accounting system and submits to FIRS | Both buyers and sellers carry risk if FIRS validation step is skipped |

| FIRS Validation | Central validator | Checks data, assigns an IRN, returns stamped invoice | IRN = Invoice Reference Number. An invoice without one cannot be used to claim input VAT |

| Buyer | Invoice recipient | Receives IRN-stamped invoice and uses it to claim VAT credit | Invoice must carry valid IRN to be eligible for VAT credit claim |

| TaxPro-Max | FIRS central portal | Stores all invoice data; cross-matched against VAT returns | All invoice data stored here for audit and reconciliation purposes |

PEPPOL, a network in which invoices pass between business systems, is used by most countries, such as Australia or Singapore. Nigeria works differently. In this case, all invoices will have to pass through FIRS.

FIRS verifies the information, signs it with an Invoice Reference Number (IRN) and only the invoice may be sent to the buyer. Imagine it as a toll gate: the invoice will not be cleared until it is cleared by FIRS.

This matters because:

1. Invoices without an IRN are not eligible for the buyers to claim VAT credits.

2. Sellers that do not validate are penalized.

3. Mismatches can be automatically identified by FIRS between the invoices submitted and VAT returns.

E-Invoicing and Why it is Important to Businesses

The motivation behind the e-invoicing model in Nigeria is compliance but it has more than regulation effects. It directly enhances the day-to-day operations of the finance teams. On the simplest level, invoices are approved and then they are accepted. This helps minimize errors at an early stage and avoid future problems towards the end of the process like rejections, arguments, or delayed payments.

It enhances visibility as well. Finance departments can monitor invoice status real time, thus, it is easier to control accounts payable and accounts receivable (AP and AR).

What businesses gain

- Reduced mistakes and reworking.

- Manual corrections are minimized using validated data.

- Faster invoice processing

- Reduced back-and-forth between suppliers and buyers.

- Improved visibility of cash flow, invoices and payments are closely monitored.

- Stronger VAT compliance Less risk of misalignments and audit problems.

What begins as compliance soon turns into operational efficiency.

Who is in scope?

| Business Category | Status (May 2026) | Scope / Threshold | Key Detail |

| Large Taxpayers | In Scope Now | Annual turnover ≥ ₦5 billion | Mandatory since 1 Nov 2025 (extended from 1 Aug 2025); must integrate with FIRS Electronic Fiscal System / Merchant-Buyer Solution |

| Medium Taxpayers | Upcoming — Prepare Now | Annual turnover ₦1 billion to ₦5 billion | Pilot from April 2026; mandatory go-live 1 July 2026, with a 6-month soft-landing on penalties (full enforcement in 2027) |

| Emerging / Small Taxpayers | Future Phase | Annual turnover below ₦1 billion | Pilot from April 2027; mandatory July 2027 |

| Foreign companies with a Nigerian subsidiary, branch, or PE | In Scope Now if they meet the ₦5B threshold | Treated as resident taxpayers — turnover ≥ ₦5B test applies | Same obligations as domestic large taxpayers |

| Non-Resident Companies (NRCs) without a Nigerian PE | Currently Out of Scope | Originally targeted for 1 Jan 2026; postponed | FIRS expected to revisit in 2026; specific guidance still pending |

An operational guideline: In case your Nigerian business is VAT-registered and you invoice other businesses; you should assume that you are in scope. There is no use taking a chance by waiting to receive a formal notice by FIRS.

Another significant detail as a multinational: When an external company in Nigeria invites you to provide services to a domestic company in Nigeria such as a software licence or management fee invoiced in the UK, you do not require an IRN. However, it is up to your Nigerian customer to self-account on that payment and record it accordingly.

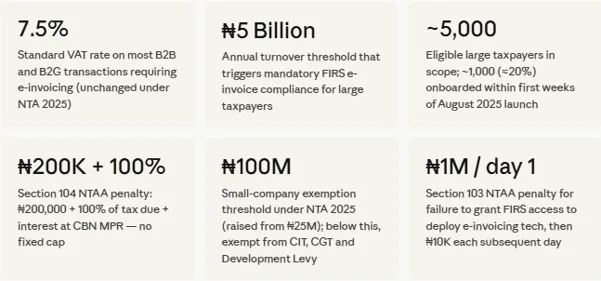

The Numbers That Matter

What Should be on a Compliant Invoice?

Having the IRN is half the battle. The information in the invoice sent to FIRS should also satisfy certain field requirements and the failure to submit a vague or incomplete description can often result in rejections. The following table divides what is always needed with that which is conditionally needed based on the type of transaction.

| Field | Required? | Plain-language note |

| Invoice Reference Number (IRN) | Always | Assigned by FIRS after validation; must appear on the invoice you send the buyer |

| Seller’s Tax Identification Number (TIN) | Always | Must match your TaxPro-Max registration exactly |

| Buyer’s TIN | For B2B | Without it, your buyer cannot claim input VAT, they will ask for it |

| Invoice date and time | Always | Use the actual transaction date, not your ERP posting date |

| Specific line-item descriptions | Always | “Goods supplied” or “services rendered” are rejected. Be specific |

| VAT amount per line and total | Always | Itemized per line; must match your VAT return submission |

| Exempt or zero-rated flag | If applicable | Reference the Finance Act provision that grants the exemption |

| Currency and CBN exchange rate | Foreign-currency invoices | Must use the Central Bank of Nigeria (CBN) official rate on the invoice date |

| QR code | POS/retail transactions | Required in FIRS fiscal device pilot zones |

How E-Invoicing Works in Nigeria (CTC Model)

Nigeria framework, as opposed to PEPPOL four-corner model, hosts the tax authority participation in the invoice lifecycle.

Simplified Flow:

Supplier System → Tax Authority (FIRS Validation/Reporting) → Buyer System

What this means operationally:

- Data on invoices is verified or reported to FIRS

- Special invoice number or confirmation can be created

- Downstream processing only involves compliant invoices

Key Components FIRS Platform

- Central validation/reporting system.

- ERP/Accounting Systems – source of invoice generation.

- Integration Layer / Middleware – interconnects systems to FIRS.

- Structured Data Format – Provides standardization.

Connection: System and ERP

Manual invoice filing in the TaxPro-Max portal is fine when the volumes are low, but with most businesses it requires an automated connection. FIRS releases an API to enable your ERP or accounting system to file invoices, get IRNs and follow-up status automatically.

In simple terms, you have the following alternatives:

- Your ERP is integrated with a local Nigerian one (as it is with Sage): the easiest route, simply set it up and start.

- Your ERP is supported partially (SAP, Microsoft Dynamics 365): you will need a middleware layer or a certified partner to support the routing of FIRS.

- Your ERP lacks in-built support (Oracle NetSuite, most legacy systems): hire an Application Service Provider (ASP) – a third party certified that will sit between your ERP and FIRS and will take care of the whole submission and IRN retrieval process.

Questions to ask when selecting an ASP include: Are they FIRS-certified? How do they deal with rejections? Are they capable of handling batch submissions in case your volumes are large? Do they give you an audit trail which traces to your VAT returns?

The VAT Reconciling Risk Most Businesses Overlook

This is where businesses are taken by surprise. Since FIRS keeps all validated invoice data in TaxPro-Max, it can cross-check: What you claimed on your monthly filing vs. what the invoices marked by IRN indicates. The difference between what your suppliers claimed and what IRN stamped invoices you raised with them.

This implies that a breach in your e-invoicing process not only poses a seller-side penalty risk but also introduces a buyer-side audit risk.

Big Nigerian companies and properly managed MNCs are refusing to pay supplier bills until they can establish a valid IRN. That makes FIRS compliance a business requirement, rather than a regulatory one.

In the case of AP teams: Integrate IRN checks into your invoice processing. Verify the IRN prior to payment of any invoice to a supplier.

How the Timeline Has Unfolded

| Period | Status | Key Milestone |

| June 2021 | Done | FIRS launched TaxPro-Max — the online tax filing & payment portal (not e-invoicing). Empowered by Finance Act 2020 |

| 2022–2023 | Done | Continued TaxPro-Max expansion; FIRS Digital Transformation Strategy (2023/24) drafted, laying groundwork for e-invoicing |

| Sep–Nov 2024 | Done | FIRS introduced legal framework for e-invoicing (Sept 2024); Merchant-Buyer Solution (MBS) pilot began November 2024 with selected large taxpayers in Oil & Gas, Manufacturing, Telecoms and Financial Services |

| April 2025 | Done | FIRS officially launched the FIRSMBS e-invoicing platform on 29 April 2025 |

| Aug–Nov 2025 | Done | Electronic Fiscal System / MBS went live 1 August 2025; mandatory compliance for large taxpayers (turnover ≥ ₦5 billion) from 1 November 2025 (extended from 1 Aug). MTN Nigeria was the first company to transmit a live e-invoice |

| Sep–Oct 2025 | Done | FIRS appointed as Nigeria’s Peppol Authority (19 Oct 2025); Nigeria Tax Act 2025 signed; FIRS reorganisation into Nigeria Revenue Service (NRS) commenced |

| January 2026 | Done | Nigeria Tax Act 2025 came into force; FIRS officially became the Nigeria Revenue Service (NRS) |

| Q1–Q2 2026 | In Progress | Medium taxpayer (₦1B–₦5B) engagement phase running through March 2026; pilot rollout in Q2 2026; large-taxpayer enforcement tightening |

| 1 July 2026 | Coming | Mandatory go-live for medium taxpayers; 6-month soft-landing on penalties (full enforcement 2027). Possible inclusion of non-resident suppliers under review |

| Apr–Jul 2027 | Future | Emerging / small taxpayers (<₦1B) pilot from April 2027; mandatory go-live July 2027 — completing the full B2B e-invoicing mandate |

Major Problems that Businesses encounter

In Nigeria, e-invoicing is not only a change in a system, but a change in processes and data. The biggest challenges are more about preparedness than regulation.

ERP integration is one of the greatest challenges. Most systems are not designed to report in real-time and this makes it hard to connect directly with FIRS.

The other problem is data quality. Lack of fields or vague descriptions can contribute to rejection of invoices.

Key challenges to prepare for

- ERP integration gaps: The legacy systems might require middleware or ASP.

- Data inconsistencies: Rejection is caused by incorrect or incomplete data.

- Real-time reporting pressure: Mistakes should not be corrected in the future but now.

- Handling rejections: In the absence of automation, resubmissions can delay operations.

Reality check: The greatest problems are based on systems and data, not the regulation itself.

The next step to take by businesses

To get ready for the e-invoicing compliance framework in Nigeria:

- Determine ERP preparedness to real-time reporting.

- Introduce connectivity with FIRS systems.

- Standardize invoice data format.

- Automate validation and reconciliation processes Keep track of regulatory changes.

Future perspective: What will become of E-Invoicing in Nigeria

The e-invoicing system in Nigeria is in its developmental stage. Whatever is being introduced today will probably be widened in its scope and application.

This will gradually bring more businesses into the fold and this includes mid-sized and small companies. There are also validation rules that are likely to be stricter.

Meanwhile, e-invoicing will be increasingly associated with VAT reporting. This implies that tax authorities will be able to see more of the transactions.

What to expect next

- Widening usage in all sizes of business.

- Tougher compliance and validation tests.

- More automation of audits and reconciliation.

- Greater integration with tax reporting.

Forward view: E-invoicing is not a short-term endeavour in the tax system in Nigeria, but a long-term obligation.

Conclusion

E-invoicing in Nigeria must not be viewed as a one-time need, but rather as one of the fundamental compliance capabilities. The e-invoicing system in Nigeria is an important move towards real-time tax transparency and compliance. This contrasts with PEPPOL-based markets in which the emphasis is not only on efficiency but also on regulatory control and transparency. With the growing framework, companies investing early in integrating, standardizing data and automation will be in a better position to handle compliance and enhance operational efficiency.

E-invoicing is no longer a choice in Nigeria, but rather a necessity to conduct business in a compliant manner.

FAQs

It is being applied in stages, beginning with big taxpayers, and will extend into all types of businesses.

The CTC model used in Nigeria, where the business invoice information is reported to the tax authority compared to PEPPOL, where businesses can exchange information directly.

Yes, integration is needed to report or validate invoice data as compliance.

Invoices can be rejected or flagged, which can affect the downstream processing and compliance.

It improves accuracy and ensures real-time reporting, reducing discrepancies and audit risks.

The main challenges are system integration, real time reporting capability and data standardization.

Yes, automation tools can facilitate reporting, validation and reconciliation.