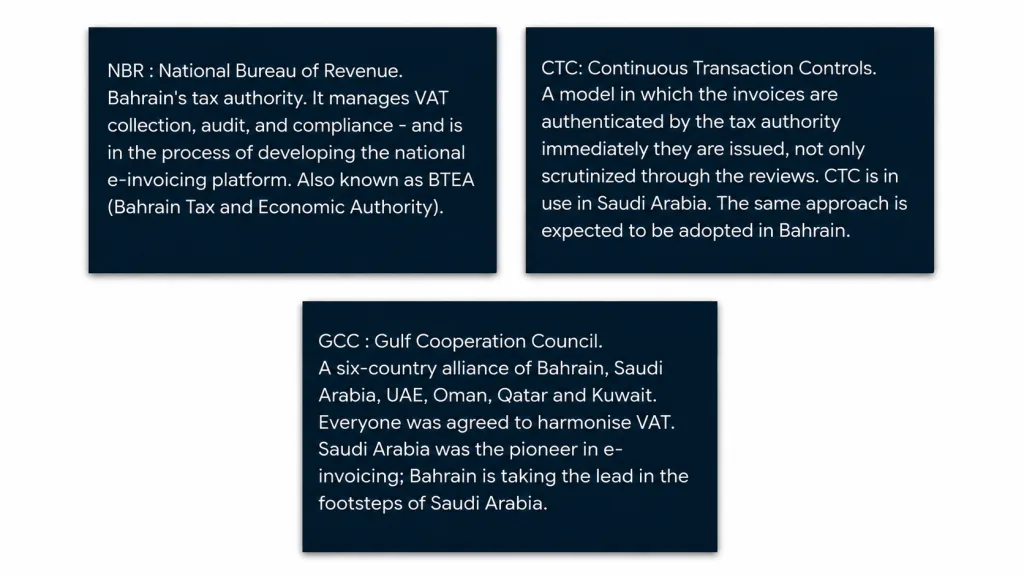

With the increasing pace of digital transformation in the sphere of taxation in the GCC, Bahrain is planning its next big move to modernize its tax environment by means of e-invoicing. Although a fully enforced e-invoicing system, such as that of Saudi Arabia, is not yet enforced in the country, the National Bureau for Revenue (NBR) demonstrates the imminent change.

For businesses operating in Bahrain, this is not a question of if but when. Planning ahead can bring the difference between a successful compliance and a disrupted operation.

To Begin with, the fundamentals: terminology you will continually come across

Unless you are a tax expert, the discussion of Bahrain e-invoicing can soon be dotted with acronyms. Here is a plain-language glossary of the terms that are most important.

Knowing the Present Situation

In 2019, Bahrain implemented VAT and since that time, it has been based on conventional invoicing with digital record-keeping conditions. Nonetheless, as the world continues to trend towards real-time tax reporting, Bahrain will probably follow the trend of regional leaders such as the United Arab Emirates and Saudi Arabia.

The NBR has already highlighted:

- Accurate invoice documentation

- Digital audit readiness Timely

- VAT reporting

The next step is e-invoicing.

What is e-invoicing and why is it not the same as sending a PDF?

There are already numerous businesses that send invoices via email as PDF files. That does not mean e-invoicing compliance-wise. A PDF is a readable document to a human being but cannot be automatically read, verified, and processed with a system of a tax authority.

Real electronic invoicing refers to creating an invoice in a structured, machine-readable format – most commonly XML or JSON and placing it into an approved channel, either to your customer directly or to a government-linked network that authenticates it first.

| Aspect | PDF Invoice (Old Way) | E-Invoice (Compliance Model) |

| Sender | Your business | Your business (ERP / billing system) |

| Transmission | PDF sent by email | Submitted directly to NBR Central Platform |

| Customer | Customer receives PDF | Customer receives validated invoice |

| Tax Authority Visibility | NBR sees data only at VAT return time | NBR sees transaction in real time |

| Invoice Status | Unverified | Validated · Traceable · Compliant |

Is Bahrain currently obliged to use e-invoicing?

No – as of April 2026, e-invoicing is not mandatory (officially) in either B2B, B2G or B2C transactions in Bahrain. The NBR has not published a formal date of mandate.

But Bahrain is not sitting back. The National Bureau for Revenue has been working hard to develop the infrastructure, consulting businesses, and providing signals that it is planning to do so. Tax experts and industry commentators agree that a gradual B2B requirement will commence in 2026, initially with big taxpayers who turnover more than a BHD 500,000 annually.

How the Bahrain e-invoicing system is Expected to work

NBR has not yet published final technical specifications however, grounded on the RFP, stakeholder consultations, and in comparison, with the Saudi Arabia ZATCA system, the framework that is likely to be used is emerging.

A Central Platform Model

Bahrain is developing what the RFP defines as an “E-invoicing central platform” a government-based system to which businesses submit invoice data, which is validated and stored. Imagine it to be an online clearing house. Your customer does not receive your invoice directly but goes through the NBR.

What businesses will be required to do

- Create invoices in structured format (XML or JSON) and not PDFs. The format should be machine-readable with all the required fields of VAT.

- Register and connect with the NBR central platform, your ERP or billing system should be connected to the system using API and send invoices safely without manipulation.

- Use digital signatures: cryptographic signing of invoices is anticipated, as in the case of Saudi Arabia. This provides that invoices cannot be changed once issued.

- Keep complete audit records: all transactions should be tracked. The system will automatically recognize and indicate non-compliant invoices.

- Send invoice information in real time and not only on VAT return time. Such is the Continuous Transaction Controls (CTC) model in action.

What a compliant tax invoice should already contain

In the present Bahrain VAT legislation (with or without e-invoicing) each tax invoice shall include the following elements: Tax Registration Number (TRN) of the supplier, supply date, a description of goods or services, amount of VAT billed, amount payable, and the buyer information in the case of B2B transactions. These fields will also have to be typed in structured XML/JSON format rather than typed on a document when the e-invoicing mandate arrives.

What will happen when you do not comply?

E-invoicing non-compliance falls under the general VAT enforcement regime by the NBR which includes penalties.

Companies not fulfilling EIS requirements face the risk of:

• Monetary fines on the issuing of invoices through the EIS portal or otherwise and in non-compliant format.

• Rejection of input VAT claims due to lack of proper clearance and stamping of incoming invoices.

• Automatic red flags in VAT returns where invoice information is mismatched with reported VAT values.

Bahrain vs Saudi Arabia: what the GCC comparison tells us

| Feature | Saudi Arabia (ZATCA) — Live | Bahrain (NBR) — Expected 2026 |

| Launch Approach | Phased by turnover threshold, starting with largest taxpayers | Expected phased, starting with BHD 500K+ turnover |

| Phase 1 | Generate & archive: businesses issue structured invoices | Likely generation mandate: issue XML/JSON invoices |

| Phase 2 | Integration & clearance: real-time submission to ZATCA | Central platform integration, real-time reporting |

| Invoice Format | UBL-based XML with QR code | XML or JSON (likely); QR code anticipated for B2C |

| Digital Signing | Mandatory cryptographic stamp from ZATCA | Anticipated; details not yet published |

| Archive Requirement | Invoices archived for minimum 6 years | Likely similar; current VAT law requires records kept |

| Governing Authority | ZATCA (Zakat, Tax and Customs Authority) | NBR / BTEA (National Bureau for Revenue) |

Preparing your business to be Bahrain VAT e-invoicing

The technical requirements are not published yet you cannot wait to prepare until you receive them. It is a lengthy process: ERP upgrades, negotiating with vendors, testing, employee training, process modifications do not occur overnight. The following is what you are supposed to do now.

| Step | Action | Detail |

| Confirm | Confirm your VAT registration and EIS scope | Check whether your business is registered for VAT with the NBR and verify whether your transaction types (B2B, B2C, B2G) fall within the current or upcoming EIS mandate. If you have not yet received a wave notification, monitor nbr.gov.bh closely. |

| Assess | Run a gap assessment on your invoicing systems | Review your existing invoicing setup against NBR EIS technical requirements. Key gaps to look for: XML output capability, NBR portal API integration, cryptographic stamp support, QR code generation for B2C invoices, and a 5-year audit log retention setup. |

| Integrate | Choose your integration path | You can integrate with the NBR EIS portal directly through your ERP system or through an NBR-approved service provider. Mid-market businesses typically work through an accredited service provider (ASP). Large enterprises may build direct ERP-to-NBR API integration. Assess both options against your technical readiness and go-live deadline. |

| Update | Update your AP and AR workflows | Build NBR clearance validation into your purchase approval and invoice issuance workflows. AP teams must check that incoming invoices carry a valid NBR digital stamp before processing payment or claiming input VAT. AR teams must ensure the EIS clearance step is completed before invoices are dispatched to buyers. |

| Train | Train your teams and update your controls | Finance, procurement, and shared services staff handling Bahrain transactions need updated training on what a compliant EIS invoice looks like, how to handle non-compliant incoming invoices, and how to apply the correct input VAT treatment. |

Readiness Checklist

| Sr No | Step | Action | Detail |

| 1 | Audit | Audit your invoicing setup | Can your ERP produce XML/JSON output? |

| 2 | Verify | Verify VAT invoice fields | TRN, dates, VAT amount: all correct? |

| 3 | Engage | Engage ERP/software vendors | Ask about NBR platform integration roadmap |

| 4 | Adopt | Issue e-invoices voluntarily now | No NBR approval needed since Nov 2023 |

| 5 | Monitor | Monitor NBR announcements | Set alerts for BTEA / NBR updates |

| 6 | Align | Brief finance & IT together | This touches both. Build a cross-functional team. |

Conclusion

It is not a matter of whether: Bahrain e-invoicing is a matter of when. Since 2022, the NBR has been developing towards a mandatory system, and the platform is currently being constructed. With VAT registered businesses, particularly those with high turnover, the issue is not whether to prepare, but whether to prepare now or to scramble later.

The companies that will do this most optimally are the ones that will approach it as a strategic initiative and not as a compliance issue. Begin by a sincere assessment of your invoicing capacity. Discuss with your ERP supplier. Align your finance and IT teams. And watch closely NBR announcements of the official technical specifications.

The better you prepare now, the easier it will be when the mandatory to use e-invoicing in Bahrain officially becomes a reality.

Automate. Integrate. Stay Ahead of the NBR Mandate with Cygnet.One.

FAQs

Currently, e-invoicing is not compulsory in Bahrain. Nevertheless, the National Bureau for Revenue is progressing towards the development of digital compliance structures, which means that regulations on e-invoicing might be implemented soon. Companies ought to start planning in advance to prevent last minute shocks.

The e-invoicing will be used in Bahrain on businesses registered to pay VAT. This encompasses businesses in all industries (especially high volume of transactions), complicated supply chains or those that involve cross-border reporting of their taxes that must be done correctly and promptly.

Although no formal specifications are published, it is expected that Bahrain will use structured invoice formats (XML or JSON). These formats facilitate system integration in real time, validation and standard data transmission between business and tax authorities.

Bahrain can either use a clearance model, in which invoices are checked and then issued, or a reporting model, in which invoice information is exchanged after the issuance. The same strategies have been used in Saudi Arabia and the United Arab Emirates and this provides one with an idea of what to expect.

The businesses can begin by evaluating their existing invoicing procedures, improving ERP systems, and data accuracy. The need to invest in automation and real-time reporting features will assist organizations to make a smooth transition once regulations are implemented.

Any failure to prepare in time may cause serious problems like incompatibility of the system, cancellation of invoices and fines. It can also interfere with the cycles of cash flow and cause more manual intervention, which affects the efficiency of operations, in general.

Yes, e-invoicing is going to make the process of AP and AR much easier, as it will allow to promptly validate invoice and minimize mismatch. The result of this is faster approvals, better reconciliation and more visibility of financial transactions.

Automation is an important aspect as it helps to check invoices in real time, minimize human error, and maintain a high level of adherence to regulatory terms. It also assists in keeping audit ready records and in integrating with government platforms.