Introduction

The input service distributor mechanism has been mandated by the GST department, effective from April 1, 2025, to ensure transparency, accuracy, and a standard process in the distribution of GST credit for third-party common services received.

Input service distributor Mechanism mandated for GST credit distribution by companies operating at multiple locations and have transactions of common expenses, including RCM, for such units/locations, and the billing is done centrally at the HO or central Unit.

Before mandating the ISD mechanism, businesses often faced inconsistency, incomplete documents, and records of ITC treatment. They interchangeably followed cross-charge or ISD practices to distribute ITC without understanding the correct compliance process.

In this blog, we shall explore the basic understanding of ISD and the compliance requirements.

What is an Input Service Distributor?

An input service distributor is an office of a supplier of goods or services that receives tax invoices for the input service, including invoices for the input service charged under RCM for or on behalf of a distinct person (person with a different GSTN registration but the same PAN) and distributes ITC among units/locations as per prescribed manner.

For instance, a company, D, registered in Mumbai, has its branches, E and F, in Ahmedabad and Jaipur, respectively, which receive common services for software maintenance from a company, J.

In this scenario, D can register as ISD and receive an input service invoice from J under the ISD GSTN. D alone cannot take ITC for the services received by all the branches. The ITC shall be distributed in the ratio of turnover among D (Normal registration), E, and F by ISD D.

Let’s take numbers to understand it in detail.

Suppose J issued an invoice of Rs 100,000 + 18%, i.e., Rs 18,000 GST, which is available for distribution.

Now the turnover of various units is as follows

D = 10 crore

E= 5 crore

F= 5 crore

Total =20 crore

The ITC shall be distributed as under

D (10/20*18000)= 9000, i.e., 4500 each of CGST and SGST, as ISD D and HO D are in the same state.

E (5/20*18000)= 4500 IGST (as Unit E and ISD D are in different states)

F (5/20*18000)= 4500 IGST (as Unit F and ISD D are in different states)

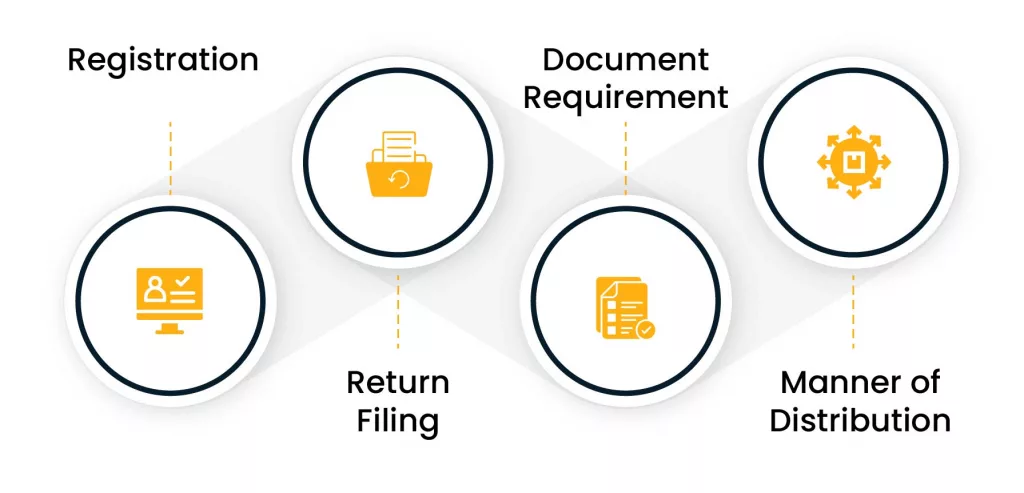

We will now examine the details of registration, return filing, documentation, distribution ratio, manner of distribution, reconciliations, and other related aspects in detail.

Compliance Requirement for Input Service Distributor

1. Registration

Requirement:

A separate ISD registration u/s 24(viii) of the CGST Act, 2017 is required irrespective of the turnover limit, for

- A business having units/branches at multiple locations under the same PAN and different GSTNs.

- Business receives a single invoice at the main unit/HO for common input services (including RCM) utilized among more than one unit.

- Business is liable to distribute ITC among all attributable units.

Overview of the registration process:

- Apply for ISD registration through FORM GST REG-01 on the GST portal

- Services > Registration > New Registration section, select “ISD” as the registration type.

- Provide business details (legal name, trade name, PAN, email, and mobile number) in Part A of the form and enter OTP for verification.

- Upon verification, a temporary TRN will be generated. Use TRN and log in to fill in additional business details in Part B.

- Submit registration form with e-verification and receive ARN (Application Reference Number)

- Upon application approval, an ISD GSTN will be generated.

Other requirements:

- A single ISD registration is allowed per state; multiple ISD registrations in the same state are not permitted.

- Applies to businesses receiving invoices for input services, including RCM services (not goods or capital goods), used by multiple branches.

2. Return Filing

- A return in FORM GSTR-6 shall be filed on the 13th of the succeeding month by ISD.

Details in GSTR-6:

- Invoices received from vendors/suppliers for input services.

- Separate distribution of eligible and ineligible ITC

- Credit or debit notes issued or received for adjustments.

- Amendments in the original information.

- Redistribution of wrongly distributed ITC.

- Other details like late fees, refund claims, ITC mismatches, and reclaims to be distributed, etc.

3. Document Requirement

The following documents shall be issued as per sub-rule (1) of rule 54 of the CGST Rules 2017:

- ISD must issue an ISD invoice to distribute ITC to their branches, clearly indicating in such invoice that it is issued only for GST credit distribution.

- The Input Service Distributor shall issue an ISD credit n ote for the reduction of credit in case the ITC already distributed gets reduced for any reason.

4. Manner of Distribution

The following points describe the manner of Distribution

- ITC shall be distributed among the common service recipient branches in proportion to the ratio of their turnover for the relevant period.

- The amount of credit distributed shall not exceed the total credit available.

- The ITC for common services attributable to the recipient shall be distributed to that particular recipient only.

- If ITC for common services is attributable to more than one branch/unit, it shall be distributed to all such recipient branches on a pro-rata basis as per their turnover to the aggregate of the total turnover of all such recipients.

- If ITC for common services is attributable to all branches/units, it shall be distributed to all such recipient branches on a pro-rata basis as per their turnover to the aggregate of the total turnover of all such recipients.

- Relevant Period for turnover considerations

- Turnover of preceding financial year, if the turnover for all recipients receiving common services is available.

- If the turnover of the preceding financial year is not available for all recipients receiving common services, then the turnover of the last quarter for which details of turnover are available.

- Relevant Period for turnover considerations

- The ITC available for distribution in a month shall be distributed in the same month, and the details shall be furnished in return.

- Distribution of IGST, CGST, SGST/UTGST

- When ISD and branches are in the same state

- IGST shall be distributed as IGST.

- CGST shall be distributed as CGST.

- SGST/UTGST shall be distributed as SGST/UTGST.

- When ISD and branches are in different states

- The total of IGST, CGST, SGST/UTGST attributable to the recipient shall be distributed as IGST.

- When ISD and branches are in the same state

5. Other practices vital for Input Service Distributor compliance

Vendor Coordination

- Identify all third-party common expenses received by branches/units.

- Inform the respective vendors/suppliers and provide them with the ISD GSTN, and communicate clearly with them to ensure they issue invoices with the ISD GSTN.

Reconciliations

- Before filing GSTR-6, reconciliation of GSTR-6A( an auto-populated statement reflecting ITC available as per vendor’s GSTR-1) with ISD invoices and ITC booked by ISD for distribution to ensure there is no mismatch or errors in ITC availment and distribution.

System and process upgrade to integrate ISD

- Update software to generate ISD invoices, track ITC distribution, perform reconciliations, calculate ratios, and ensure compliance with GSTR-6 filing requirements.

- Train finance and tax teams on ISD compliance, including correct ITC allocation and GSTR-6 filing

- Maintain proper documentation of invoices, ITC distribution, and services used by each branch for audit purposes.

Regular internal audit and compliance check

- Conduct an internal audit regularly to check the following compliance

- Ensure that third-party common services invoices received are issued under ISD.

- Ensure a valid ISD invoice, CN, or DN is issued for ITC distribution.

- Verify turnover ratio calculations for each transaction.

- Ensure compliance with RCM transactions.

- Conduct various reconciliations to ensure accuracy

- Verify details as per the return and ensure timely filing.

- Ensure there is no anomaly in the ISD software and process.

- Any discrepancies or errors found should be reported in the audit report and resolved by paying the applicable tax and interest.

- Intimation of payment shall be made to the department via the DRC-03 form.

- Ensure that documents are well-maintained, including those necessary to explain discrepancies or mismatches, as well as the subsequent actions taken.

Penalties for Non-compliance

Failure to Register: A penalty of ₹10,000 or the amount of ITC irregularly distributed, whichever is higher, may be imposed for failing to obtain mandatory ISD registration.

Excess Distribution: Excess ITC distributed in violation of GST provisions will be recovered from recipient units with 18% per annum interest under Sections 73 or 74 of the CGST Act. It can also attract a penalty of Rs 25,000.

Audit Risks: Non-compliance may lead to audits, show-cause notices, and denial of ITC claims, increasing tax liability and disrupting operations.

How Cygnet Helps in ISD Compliance

Cygnet GST compliance Input Service Distributor solution streamline ISD compliance by automating the end-to-end process of ITC distribution, reconciliation, and return filing.

Their platform ensures seamless management of ISD invoices, credit/debit notes, and GSTR-6 filings, enabling accurate and timely distribution of ITC to recipient units based on turnover ratios.

With AI-driven tools, Cygnet facilitates various reconciliations to minimize errors and ensure compliance with GST regulations.

By integrating with ERP systems and offering real-time analytics, Cygnet enhances efficiency, reduces manual efforts, and mitigates risks of penalties, helping businesses stay audit-ready and optimize ITC utilization.

Summary

The mandatory Input Service Distributor mechanism, effective from April 1, 2025, introduces a standardized approach to ITC distribution for businesses with multiple GSTINs under the same PAN, ensuring transparency and compliance with GST regulations.

By adhering to key compliance requirements, such as obtaining ISD registration, filing GSTR-6 returns, issuing proper ISD invoices, distributing ITC based on turnover ratios, and conducting regular reconciliations and audits, businesses can avoid penalties, optimize ITC utilization, and maintain audit readiness.

Author

Komal Vithalani

Content Writer

Komal Vithalani, a Chartered Accountant and Commerce graduate, is a dedicated professional committed to delivering value with years of expertise in navigating the complexities of indirect tax laws. Her practical excellence includes managing perplexed litigations, dispensing tactical tax advice, conducting thorough compliance checks, supervising audits, and crafting articulate and insightful content. At Cygnet, Komal seamlessly blends her profound understanding of tax regulations with cutting-edge tax technology. Leveraging her competence, she adeptly transforms complex tax tech jargon into concise, impactful, and engaging content. This not only aids readers in comprehending tax-related topics with enlightening clarity but also ensures the delivery of narratives that resonate broadly.